Case Law Details

Saket Promoters Limited Vs Principal Commissioner of Service Tax-I (CESTAT Kolkata)

The appeal challenged an Order-in-Original confirming a service tax demand of Rs. 7,70,381 along with interest and an equal penalty in respect of a real estate project at 39A, Jorapukur Square Lane, Kolkata. The adjudicating authority had confirmed the demand solely on the ground that the completion certificate dated 11.06.2010, issued by Shri Sanjib Datta, LBS.I/1165, Kolkata Municipal Corporation (KMC), was not a valid completion certificate, as it had not been issued by the competent authority under the Kolkata Municipal Corporation Building Rules, 2009. On this basis, the authority rejected the appellant’s claim that the project had been completed before the relevant date.

The appellant contended that Shri Sanjib Datta was an authorized technical person of the Kolkata Municipal Corporation who had inspected the project and certified its completion on 11.06.2010. It was further submitted that the competent municipal authority subsequently issued a formal completion certificate on the basis of the said technical certification. Accordingly, the appellant argued that the actual completion date of the project should be treated as 11.06.2010 and that no service tax demand could survive.

The Revenue maintained that the certificate issued by Shri Sanjib Datta could not be accepted as a valid completion certificate, as he was not the competent authority to issue such certificate, and therefore supported the adjudicating authority’s decision.

The CESTAT observed that the sole basis for confirming the demand was the rejection of the certificate dated 11.06.2010. It found that Shri Sanjib Datta was the technical person authorized by the Kolkata Municipal Corporation to certify completion of projects. The Tribunal further noted that the competent municipal authority had subsequently issued the formal completion certificate on 30.05.2011 on the basis of the technical certification. It held that the project had been completed in all respects on 11.06.2010 when the authorized technical person inspected the building and certified its completion, while the later certificate issued by the competent authority was only a formal certification. Accordingly, the Tribunal held that the certificate dated 11.06.2010 was a valid document for determining the completion date of the project.

Holding that the service tax demand had been confirmed solely due to non-acceptance of the valid completion certificate, the CESTAT set aside the demand. As the demand itself did not survive, the Tribunal also held that no interest or penalty was payable. The appeal was allowed with consequential relief, if any, as per law.

FULL TEXT OF THE CESTAT KOLKATA ORDER

The present appeal has been filed by M/s. Saket Promoters Limited, 46, Bepin Behary Ganguly Street, Bowbazar, Kolkata – 700 012, West Bengal [hereinafter referred to as the “appellant”] against the confirmation of the demand of Service Tax amounting to Rs.7,70,381/-, along with interest and a penalty of an equal amount thereon, vide the Order-in-Original No. 96/PR. COMMR/ST-I/KOL/2016-17 dated 31.10.2016.

2. During the course of hearing, the appellant submitted that the ld. adjudicating authority, vide the impugned order, has confirmed the demand on the ground that the completion certificate furnished by the appellant in respect of 1 (one) project located at 39A, Jorapukur Square Lane, Kolkata – 700 006 cannot be considered as a proper certificate evidencing completion. Accordingly, the ld. adjudicating authority has confirmed the demand of Service Tax of Rs.7,70,381/-, pertaining to this project, and dropped the remaining demands of Service Tax raised in the Notice.

2.1. It is the appellant’s contention that the completion certificate had been issued to them by one Shri Sanjib Datta, LBS.I/1165, K.M.C., who is the authorized person from the Kolkata Municipal Corporation; it is further pointed out that later on, on the basis of the said certificate issued by Shri Sanjib Datta, LBS.I/1165, the competent authority has also issued a formal completion certificate. Thus, it is the case of the appellant that the date of completion of the project should be treated as11.06.2010, as the documentary evidence available on record clearly indicate that the proper authority for verification has verified the project and certified that the said project has been completed as on 11.06.2010 itself. It is his submission that if the said completion certificate is accepted then no further demand sustains in the impugned order. Accordingly, the appellant prayed for setting aside the demand of Service Tax confirmed in the impugned order along with interest and penalty.

3. The Revenue’s stand is that Shri Sanjib Datta, the person who has issued the certificate in question, is not the proper officer for issuing the completion certificate; it is their contention that the ld. adjudicating authority has rightly rejected the letter issued by Shri Sanjib Datta on 11.06.2010 as the same cannot be admitted as evidence of completion. Accordingly, he prayed for rejecting the appeal filed by the appellant.

4. Heard both sides and perused the records of the case.

5. We find that the ld. adjudicating authority has confirmed the demand of Service Tax of Rs.7,70,381/-pertaining to one project located at 39A, Jorapukur Square Lane, Kolkata – 700 006, on the ground that the completion certificate submitted by the appellant cannot be considered as a proper certificate evidencing completion. The reasoning given by the Ld. Adjudicating authority for rejection of the Certificate is that the completion certificate was not issued to the appellant by the competent authority. For ease of reference, the relevant observation made by the ld. adjudicating authority to this effect in the impugned order is extracted below: –

“5.9 I find that the said assessee has submitted documents regarding completion certificate against two projects namely “Girish Park” at 39A Jorapukur Square Lane, Kolkata 700006 and Saket Nagar situated at 127 B. T Road, Kolkata 108 claiming completion prior to 1.7.2010. I find the completion certificate in respect of the construction at 127, B. T Road was issued on 16.06.2010 by the Baranagar Municipality as per section 34(2) of The West Bengal Municipal (Building) Rules 2007 as amended. Therefore the contention of the said assessee in respect of the said premises is acceptable. On the other hand the said assessee has produced a letter from Sanjib Datta LBS.I/1165 dated 11.6.2010 in support of completion certificate. However I do not admit this as certificate of completion. The completion certificate in respect of the premises at 39A Jorapukur Lane, Kolkata – 700006 being under jurisdiction of Kolkata Municipal Corporation ought to be issued under the section 28(2) of the Kolkata Municipal Corporation Building Rules 2009 by the competent authority. The Municipal Commissioner is the competent authority to issue such certificate of completion in schedule XIII. Therefore I do not consider this as the completion certificate and deny the plea of the said assessee.”

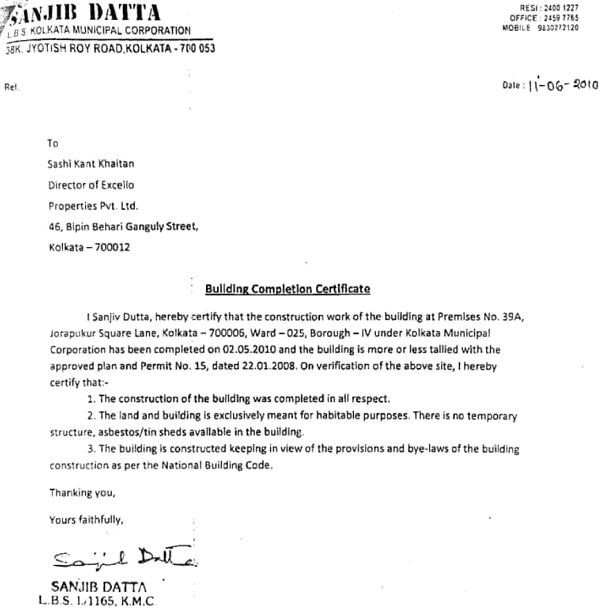

5.1. From the above, it is clear that the sole ground for confirming the impugned demand is due to nonacceptance of the certificate/letter dated 11.06.2010 issued by Shri Sanjib Datta indicating completion of the project. For better appreciation of the facts, the said letter/certificate dated 11.06.2010 issued by Shri Sanjib Datta, LBS.I/1165 is reproduced below: –

6. We find that Shri Sanjib Datta, LBS.I/1165, K.M.C., is in fact the technical person authorized by the Kolkata Municipal Corporation for certifying the completion of the Projects. Significantly, it is observed that subsequently, on the basis of the said certificate issued by Shri Sanjib Datta, the Kolkata Municipal Authorities have also issued a formal completion certificate to that effect. Thus, we agree with the submission of the appellant that as on 11.06.2010, when the technical person of the Kolkata Municipal Corporation examined the buildings in the project and issued a letter to the effect that the building is complete in all respects, the said date has to be considered as the date of completion of the project. Subsequent issuance of the certificate of completion by the appropriate authority on 30.05.2011 was a formal certification, which was required to be fulfilled by the competent authority. Thus, we observe the project in question has been completed in all respects on 11.06.2010 when the technical person authorized by the Kolkata Municipal Corporation, namely, Shri Sanjib Datta, LBS.I/1165 examined the project and issued the certificate as to the status of completion of the said project. Therefore, we consider that the completion certificate for the said project was issued on 11.06.2010 and formally approved by the competent authority later, on 30.05.2011. Hence, we hold that the said certificate dated 11.06.2010 is eligible to be considered towards completion of the said project located at 39A, Jorapukur Square Lane, Kolkata – 700 006.

7. In view of the above, we hold that the demand confirmed in the impugned order on the ground that the certificate issued by Shri Sanjib Datta is not a valid document, deserves to be set aside. Accordingly, the said demand of service tax confirmed in the impugned order stands set aside. Since the impugned demand itself does not survive, the question of demanding interest or imposing penalty thereon does not arise.

8. In these terms, the appeal filed is allowed, with consequential relief, if any, as per law.

(Order pronounced in the open court on 25.06.2026)

Author Bio