Case Law Details

Preethi Engineering Enterprises Vs DCIT (ITAT Raipur)

The appeal arose from the order of the CIT(A)/NFAC dated 26.02.2026 for AY 2014-15. The principal issue before the ITAT Raipur was whether the notice issued under Sections 147/148 of the Income-tax Act was valid when it had been issued by an Assistant Commissioner of Income Tax (ACIT), although the assessee contended that jurisdiction vested with the Income Tax Officer (ITO) under CBDT Instruction No. 1/2011 dated 31.01.2011.

The assessee submitted that, in the return of income filed under Section 139(1) for AY 2014-15, the gross total income declared was ₹1,38,829. According to CBDT Instruction No. 1/2011, jurisdiction over non-corporate assessees having returned income up to ₹15,00,000 vested with the ITO. The assessee argued that the notice dated 31.03.2021 issued under Section 148 for reassessment proceedings had been issued by the ACIT, Circle-1(1), Bilaspur instead of the ITO. It was therefore contended that the ACIT lacked the inherent jurisdiction prescribed under the CBDT Instruction to issue the notice and that the reassessment proceedings initiated on the basis of such notice were invalid.

The Tribunal examined the issue in light of judicial precedents. It referred to the decision of the ITAT Delhi in Vikas Jhuntra and Sons HUF v. ACIT, where, on identical facts, it was held that the authority competent to issue a notice under Section 148 must be determined in accordance with the monetary limits prescribed in CBDT Instruction No. 1/2011. In that case, the Tribunal had held that where the assessee’s returned income was below the prescribed monetary limit, the notice under Section 148 ought to have been issued by the ITO. Since the notice had instead been issued by the ACIT, it was held to be without jurisdiction, void ab initio, and the consequential reassessment proceedings were quashed. The ITAT Delhi had also relied on its earlier decision in Aashiyana Infrastructure Development Pvt. Ltd., where a notice under Section 148 issued by an officer lacking jurisdiction was similarly held to be defective and void ab initio.

The Tribunal also referred to the judgment of the Bombay High Court in Ashok Devichand Jain v. Union of India, where the High Court held that a notice under Section 148 is a jurisdictional notice and any inherent defect relating to the authority issuing such notice is not curable. In that case, the High Court held that a notice issued by an officer who lacked jurisdiction under CBDT Instruction No. 1/2011 was invalid and without authority in law, notwithstanding administrative difficulties in transferring the PAN to the competent jurisdiction.

Following the above judicial precedents and applying the ratio of the Supreme Court decision in Union of India v. Rajeev Bansal, the Tribunal held that the ACIT, Circle-1(1), Bilaspur did not possess the valid inherent jurisdiction under CBDT Instruction No. 1/2011 to issue the notice under Section 148 to the assessee. Accordingly, the notice issued under Section 148 was held to be void ab initio.

The Tribunal further held that once the jurisdictional notice under Section 148 was void ab initio, it could not provide the foundation for a valid reassessment order. Consequently, the reassessment order framed pursuant to the defective notice was quashed, and all subsequent proceedings were held to be non est in law. In view of the finding on jurisdiction, the remaining grounds raised by the assessee became academic and required no adjudication.

Accordingly, the Tribunal allowed the appeal and quashed the reassessment proceedings initiated under Sections 147/148 of the Income-tax Act.

FULL TEXT OF THE ORDER OF ITAT RAIPUR

The present appeal preferred by the assessee emanates from the order of the Ld. CIT(Appeals)/NFAC, dated 26.02.2026 for the assessment year 2014-15 as per the grounds of appeal on record.

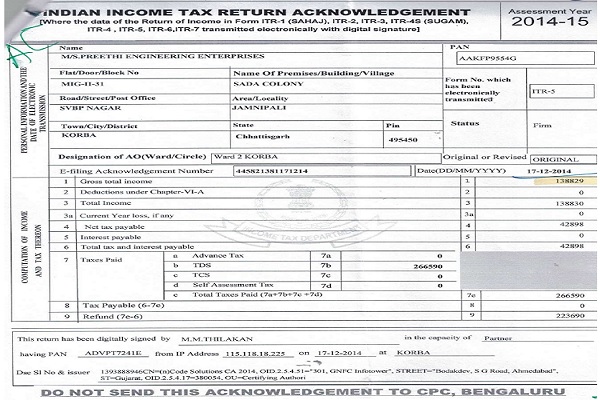

2. The contention in law assailed by the Ld. Counsel for the assessee is that as per the return filed under section 139(1) of the Act for A.Y. 2014-15 the assessee had shown gross total income of Rs. 1,38,829/-. The said copy of the return is extracted as follows:

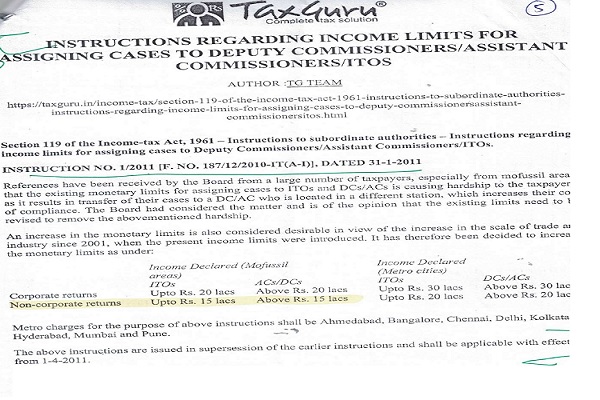

3. The Ld. Counsel further submitted that as per CBDT Instruction No. 1/2011 [F. No. 187/12/2010-IT(A-I)], Dated 31-01-2011 for non-corporate return up to Rs. 15,00,000/- the assessment has to be done by the ITO. The said copy of the instruction as extracted as follows:

4. It is the grievance of the assessee that in such scenario the notice under section 148 of the Act for reassessment proceedings under section 147/148 of the Act dated 31.03.2021 for A.Y. 2014-15 had been issued to the assessee not by ITO but by the ACIT, Circle-1(1), Bilaspur who is, therefore, not having the valid jurisdiction to issue such notice. It was further contended by the Ld. Counsel that being a non-corporate assessee and as demonstrated as per the return filed was below Rs. 15,00,000/-, therefore, the valid jurisdiction as per CBDT instruction (supra), it was with the A.O. who had to issue notice under section 148 of the Act. The ACIT, Circle-1(1), Bilaspur issuing notice to the assessee suffers from invalid jurisdiction.

5. I find that in the identical facts and circumstances and issue the Coordinate Bench Delhi in the case of Vikas Jhuntra and Sons HUF vs. ACIT, Circle-49(1), Delhi 2026 (5) TMI 1251 – ITAT Delhi held that having regard to CBDT Instruction governing monetary limits for jurisdiction, the ACIT lacked authority to issue the notice under section 148 in the assessee’s case and therefore, the entire reassessment proceedings was void. The relevant observation are extracted as follows:

“5. Undisputedly, the assessee had filed return of income u/ s. 139(1) of the Act on 21.06.2019 declaring total income of Rs. 7,34,500/ -, i.e., less than the monetary limit of Rs. 20,00,000/ – specified under CBDT Instruction No. 1/2011 dated 31.01.2011 (supra). Even in the return of income filed by the assessee in response to notice u/ s. 148 of the Act, the assessee had declared total income of Rs. 7,34,500/ -. The said return of income is at page 95 of the paper book. Thus, in light of aforesaid CBDT Instruction, the notice u/ s. 148 of the Act ought to have been issued by the ITO. Since, in the present case the notice has been issued by the ACTT, the same is without jurisdiction, hence, void ab Initio. I find that the Division Bench of the Arbunal in the case of Aashiyana Infrastructure Development Pvt. Ltd. vs. DCIT in ITA No.8472/ Del/ 2019, decided on 04.07. 2025 in similar facts had held notice issued u/ s. 148 of the Act to 20 defective and void ab initio. Thus, in light of the above undisputed facts, I hold that the notice issued u/ s. 148 of the Act by the ACTT is without Jurisdiction. Consequently, the proceedings arising from such defective notice are vitiated and hence, quashed

6. In the result, appeal of the assessee is allowed.”

6. Further, the Hon’ble High Court of Mumbai in the case of Ashok Devichand Jain vs. Union of India & Ors. (2023) 452 ITR 00 43 (Born.) observed and held as follows:

“2. The primary ground that has been raised is that the Income Tax Officer who issued the notice under section 148 of the Act, had no jurisdiction to issue such notice. According to Petitioner as per instruction No. 1/2011 dated 31st January, 2011 issued by the Central Board of Direct Taxes, where income declared/ returned by any Non-Corporate assessee is up to Rs. 20 lakhs, then the jurisdiction will be of ITO and where the income declared returned by a Non Corporate assessee is above Rs. 20 lakhs, the jurisdiction will be of DC/ AG.

3. Petitioner has filed return of income of about Rs. 64,34,663/- and therefore, the jurisdiction will be that of DC/ AC and not ITO. Mr. Jain submitted that since notice under section 148 of the Act has been issued by ITO, and not by DC/ AC that is by a person who did not have any jurisdiction over Petitioner, such notice was bad on the count of having been issued by an officer who had no authority in law to issue such notice.

4. We have considered the affidavit in reply of one Mr. Suresh G. Kamble, ITO who had issued the notice under section 148 of the Act. Said Mr. Kamble, ITO, Ward 12(3)(1), Mumbai admits that such a defective notice has been issued but according to him, PAN of Petitioner was lying with ITO Ward (12)(3)(1), Mumbai and it was not feasible to migrate the PAN having returned of income exceeding Rs. 30 lakhs to the charge of DCIT, Circle 12(3)(1). Mumbai, as the time available with the ITO 12(3)(1) was too short to migrate the PAN after obtaining administrative approval from the higher authorities by 31st March, 2019.

5. The notice under section 148 of the Act is jurisdictional notice and any inherent defect therein is not curable. In the facts of the case, notice having been issued by an officer who had no jurisdiction over the Petitioner, such notice in our view, has not been issued validly and is issued without authority in law.”

7. Respectfully following the aforestated judicial pronouncements and even applying the ratio of Hon’ble Supreme Court in the case of Union of India & Ors. vs. Rajeev Bansal, in Civil Appeal No. 8629 of 2024, dated 03.10.2024 the ACIT, Circle1(1), Bilaspur did not posses valid inherent jurisdiction as per the CBDT instruction (supra) to issue notice under section 148 of the Act to the assessee. Therefore, the notice under section 148 of the Act is void-ab-initio. That once the very notice under section 148 is held void-ab-initio it cannot enable framing of valid reassessment order which is, therefore, quashed. Subsequent proceedings becomes non-est as per law. Rest other grounds stand academic only.

8. As per the above terms the appeal of the assessee is allowed.

Order pronounced in open court on 24th day of June, 2026.

Author Bio