Case Law Details

Econship Tech Pvt. Ltd. Vs Commissioner of Customs (CESTAT Chennai)

The Chennai Bench of the Customs, Excise and Service Tax Appellate Tribunal (CESTAT) allowed the appeal by way of remand, setting aside the orders confirming customs duty of ₹3,92,28,576, interest, confiscation, redemption fine and penalty for the alleged violation of Notification No. 104/94-Cus. dated 16.03.1994. The Tribunal held that the proceedings suffered from incomplete verification and inadequate examination of the evidence, making the impugned orders unsustainable.

The appellant, a steamer agent and main line operator at Chennai Port, had imported durable containers by availing exemption under Notification No. 104/94-Cus. after executing a continuity bond. The Department alleged that proof of re-export had not been furnished for 6,163 containers and issued a show cause notice proposing recovery of duty, confiscation and penalties. During adjudication, the disputed number of containers was successively reduced to 4,020 and thereafter to 3,886 after exclusion of duplicate entries and other discrepancies. In the de novo proceedings, duty of ₹3,92,28,576, along with interest, redemption fine of ₹1,37,00,000 and penalty of ₹40,00,000, was confirmed and subsequently upheld by the Commissioner (Appeals).

The appellant contended that the entire demand rested on the erroneous assumption that the containers appearing in the departmental compilation had not been re-exported. It submitted that Notification No. 104/94-Cus. grants exemption for temporarily imported durable containers subject to re-export and that the burden lay upon the Department to establish breach of the notification conditions. The appellant argued that vessel-wise records, import and export particulars, reconciliation statements and other supporting documents had been produced, but no comprehensive container-wise verification had been undertaken despite earlier remand directions. It also raised limitation and challenged the confiscation and penalties. During the Tribunal proceedings, the appellant produced a reconciliation statement covering all 3,886 disputed containers, claiming verifiable export records for 3,574 containers, export details for 40 containers shipped through ports other than Chennai, asserting that 22 containers did not belong to it, and seeking an opportunity to produce records for the remaining 250 containers.

The Tribunal observed that Notification No. 104/94-Cus. is a conditional exemption requiring re-export within the prescribed or extended period. While the appellant was responsible for accounting for the imported containers and furnishing proof of re-export, the Department was required to establish breach of the notification conditions before denying the exemption. It noted that the substantial reduction in the disputed number of containers during the adjudication process itself revealed inaccuracies in the departmental data. The Tribunal further found that neither the de novo order nor the appellate order contained a comprehensive container-wise analysis showing the date of import, expiry of the permissible period, extension, alleged default, non-re-export and corresponding duty liability. Instead, the proceedings substantially relied on aggregate figures derived from departmental compilations.

The Tribunal also considered the reconciliation statement produced before it and observed that the dispute essentially required verification and reconciliation of export records rather than confirmation of duty based on departmental compilations. It held that exemption under Notification No. 104/94-Cus. could not be denied merely on the basis that a container appeared as non-exported in a departmental compilation. The adjudicating authority was required to verify, for each container, whether it had been imported under the notification, whether it had not been re-exported within the prescribed or extended period, and whether the conditions of the notification had actually been violated. In the absence of such comprehensive verification, the Tribunal held that breach of the notification conditions had not been conclusively established.

On the second issue, the Tribunal found that the factual foundation of the demand remained incomplete. It observed that the earlier remand by the Commissioner (Appeals) had intended a comprehensive examination of the documentary evidence, but the de novo proceedings again culminated in confirmation of the demand without completing container-wise verification. The repeated revisions in the disputed quantity, duplicate entries and unresolved reconciliation issues indicated that the evidence had not been adequately examined.

Accordingly, the Tribunal set aside the impugned order and remanded the matter for fresh adjudication. It directed the adjudicating authority to examine vessel-wise export records, terminal-generated container lists, Shipping Bills, Export General Manifest (EGM) particulars, Let Export Order (LEO) details, ICEGATE data, reconciliation statements and all other documentary evidence produced by the appellant. The authority was further directed to independently verify the export particulars without rejecting them solely for want of any particular format of document, afford the appellant a reasonable opportunity of hearing, and pass a fresh speaking order. The Tribunal expressly refrained from recording any final finding on limitation, leaving that issue, along with confiscation, redemption fine and penalty, open for fresh consideration. The appeal was accordingly allowed by way of remand on the ground of incomplete verification and inadequate examination of evidence.

FULL TEXT OF THE CESTAT CHENNAI ORDER

This appeal is directed against Order-in-Appeal No. 962/2025 dated 24.09.2025 passed by the Commissioner of Customs (Appeals-II), Chennai (hereinafter referred to as the “impugned order”), upholding Order-in-Original No. 111540/2025 dated 12.02.2025 and confirming the demand of duty, interest, confiscation and penalty against M/s. Econship Tech Pvt. Ltd. (hereinafter referred to as the “appellant”) for alleged violation of Notification No. 104/94-Cus. dated 16.03.1994.

2. The facts, briefly stated, are that the appellant, a Steamer Agent/Main Line Operator at Chennai Port, imported durable containers availing exemption under Notification No.104/94-Cus. dated 16.03.1994 upon execution of a continuity bond of Rs.25 crores. On the allegation that proof of re-export had not been furnished in respect of 6163 containers, the Department issued the Show Cause Notice dated 27.07.2021 proposing recovery of duty, confiscation and penalties. The original adjudicating authority has reduced the disputed containers to 4020 and confirmed duty, interest, confiscation and penalty, whereupon the Commissioner (Appeals), vide Order-in-Appeal dated 24.10.2024, remanded the matter for fresh consideration. In the de novo proceedings, after noticing duplicate entries and other discrepancies, duty of Rs.3,92,28,576/- along with interest was confirmed in respect of 3886 containers (as against 6163 containers originally noted as not re-exported), redemption fine of Rs.1,37,00,000/- and penalty of Rs.40,00,000/- were imposed, which came to be upheld by the Commissioner (Appeals) vide the impugned Order-in-Appeal dated 24.09.2025, leading to the present appeal.

3. The Ld. Advocates Shri Stebin Mathew and Shri Rohit Singh appearing for the appellant submitted that the entire proceedings rest upon the erroneous assumption that the containers reflected in the departmental compilation had not been re-exported. It was argued that Notification No.104/94-Cus. grants exemption to durable containers imported temporarily subject to re-export and that the burden lies upon the Department to establish breach of the notification conditions before demanding duty. The learned Counsel pointed out that while the Show Cause Notice covered 6163 containers, the disputed quantity was successively reduced during the process of adjudication on account of furnishing details of re-exported containers, duplicate entries and other discrepancies, thereby demonstrating that the foundation of the demand itself was shaky and uncertain. It was further submitted that detailed import and export particulars, vessel-wise records, annual reconciliation statements and other supporting documents had been produced, but comprehensive container-wise verification was not undertaken despite specific remand directions. The appellant also pleaded limitation, contending that the relevant import and export data was always available with the Customs authorities, and argued that confiscation and penalties could not survive in the absence of conclusive proof of violation of the notification’s conditions.

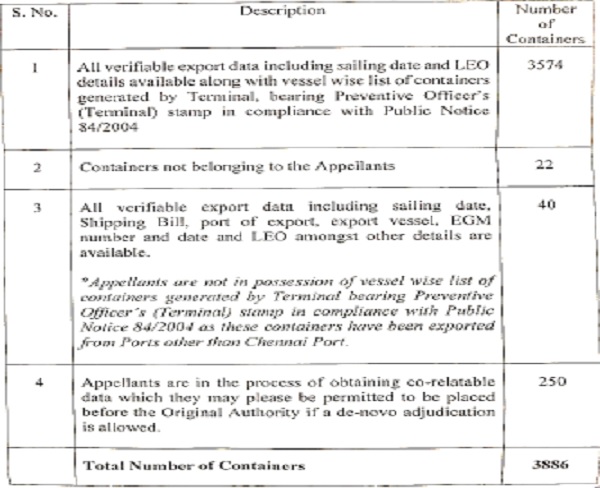

The Ld. Counsel additionally submitted that, pursuant to the directions of the Bench during hearing on 25.05.2026, a detailed reconciliation statement covering all 3886 containers under dispute was furnished before the Tribunal, indicating availability of verifiable export records for 3574 containers, export particulars for a further 40 containers exported through ports other than Chennai and a specific contention that 22 containers did not belong to the appellant, while correlatable records for the remaining 250 containers were being obtained. It was therefore contended that the dispute essentially required detailed verification and reconciliation of export records rather than confirmation of duty on the basis of departmental compilations.

4. The Ld. Authorized Representative Ms. O.M. Reena reiterated the findings contained in the Show Cause Notice, Orders-in-Original and Orders-in-Appeal and submitted that the appellant, having imported containers under Notification No.104/94-Cus. upon execution of a continuity bond, was required to re-export the containers within the stipulated period and furnish required proof thereof. It was contended that despite repeated opportunities and exclusion of containers in respect of which re-export was established, the appellant failed to satisfactorily prove compliance with the conditions of the Notification in respect of the remaining containers and, therefore, the adjudicating authority was justified in confirming the demand and in imposing consequential liabilities.

5. We have carefully considered the submissions advanced on behalf of both sides and perused the appeal records, the Show Cause Notice, the Orders-in-Original, the impugned Order-in-Appeal, the vessel-wise container details, the judicial precedents relied upon by both sides and the other documents placed on record. Upon such consideration, the following questions arise for determination: –

i. Whether violation of Notification No.104/94-Cus. stands established?

ii. Whether the impugned demand, confiscation and penalties have been confirmed on the basis of adequate verification and examination of evidence?

6. We now proceed to examine the above issues sequentially.

Issue No. (i): Whether violation of Notification No.104/94-Cus. stands established?

7. We note that Notification No.104/94-Cus. grants exemption to durable containers imported temporarily subject to re-export within six months or such extended period as may be permitted by the proper officer. Being a conditional exemption, the burden lies upon the Department to establish breach of the notification conditions before denying the benefit. The appellant is equally responsible for accountal of containers imported by furnishing details as to their re-export within 6 months and for taking extension of time when the prescribed 6 months was not complied with.

8. In the present case, the allegation originally involved 6163 containers. However, the first adjudication itself revealed substantial inaccuracies in the departmental data, resulting in reduction of the disputed quantity to 4020 containers. Thereafter, the Commissioner (Appeals), while remanding the matter, observed that the documentary evidence required fresh examination. Even in the de novo proceedings, duplicate container numbers and other discrepancies were noticed, necessitating further verification and resulting in further reduction of the disputed quantity.

9. The appellant consistently sought reconciliation through import and export records, vessel-wise details, ICEGATE data and other supporting documents. Nevertheless, neither the de novo order nor the impugned appellate order contains a comprehensive container-wise analysis showing the date of import, expiry of the permissible period, availability of extension, alleged default, non-re-export and corresponding duty liability in respect of each container. Instead, the proceedings substantially rely upon aggregate figures derived from departmental compilations.

10. We also take note of the additional reconciliation statement placed before us pursuant to the directions issued during the course of hearing on 25.5.2026. The said statement categorizes all 3886 containers forming the subject matter of the impugned demand and indicates that verifiable export data along with vessel-wise records is available for 3574 containers, export particulars including Shipping Bill, EGM and LEO details are available for a further 40 containers exported through ports other than Chennai and that 22 containers are stated not to belong to the appellant. In respect of the remaining 250 containers, the appellant has sought an opportunity to place further correlatable records before the adjudicating authority. These figures themselves demonstrate that the controversy is essentially one of proper verification and comprehensive reconciliation rather than one involving established non-reexport.

11. We also note the appellant’s contention that certain containers were exported through ports other than Chennai and, therefore, terminal-generated vessel-wise records contemplated under Public Notice No.84/2004 may not be available in the same form. In such cases, the adjudicating authority shall examine alternative export evidence such as Shipping Bills, EGM particulars, vessel details and LEO records before arriving at any conclusion.

12. The Department cannot deny exemption under Notification No.104/94-Cus. merely because a container appears in a departmental compilation as non exported. It is required to establish, through proper verification, that the particular container was imported under the notification, was not re-exported within the prescribed or extended period and thereby violated the conditions of exemption. In the absence of a comprehensive container-wise verification of the evidence produced by the appellant, including the reconciliation materials discussed above, the allegation of violation of Notification No.104/94-Cus. cannot be said to have been conclusively established. Accordingly, we are unable to hold, on the basis of the present record, that breach of the conditions of the notification stands proved.

Issue No. (ii): Whether the impugned demand, confiscation and penalties have been confirmed on the basis of adequate verification and examination of evidence?

13. We also find merit in the appellant’s contention that the dispute relates to container movements spanning several years from 2011 onwards and that the relevant import and export data must be available with Customs authorities. The proceedings themselves reveal repeated verification exercises based on departmental records and do not prima facie indicate any deliberate concealment on the part of the appellant. More importantly, the very foundation of the demand underwent substantial modification during adjudication and de novo proceedings, with the number of disputed containers being repeatedly revised after verification, exclusion of re-exported containers and identification of duplicate entries.

14. We further note that the remand ordered by the Commissioner (Appeals) was intended to facilitate a comprehensive examination of the documentary evidence produced by the appellant. However, it appears that despite reconciliation statements, import-export details and other materials being placed on record, the de novo proceedings culminated in confirmation of the demand without completion of comprehensive container-wise verification. The repeated revisions in the disputed quantity, existence of duplicate entries and unresolved reconciliation issues indicate that the factual foundation of the proceedings remains incomplete.

15. The Ld. Counsel representing the appellant has filed the following details as to the containers allegedly not re-exported: –

Thus, the additional reconciliation statement filed before this Tribunal indicates that the appellant has produced verifiable export particulars in respect of a substantial majority of the containers forming the subject matter of the demand. Once such material is available, the adjudicating authority is required to undertake container-wise verification and record specific findings thereon. Confirmation of duty without such verification would defeat the very purpose of the earlier remand ordered by the Commissioner (Appeals).

16. In these circumstances, we are unable to hold that the impugned demand, confiscation and penalties have been confirmed on the basis of complete and satisfactory verification. Accordingly, without expressing any final opinion on the merits of the demand, confiscation, interest and penalties, we set aside the impugned order and remand the matter to the adjudicating authority for fresh adjudication. The adjudicating authority shall specifically examine the vessel-wise export records, terminal-generated container lists, Shipping Bills, EGM particulars, LEO details, ICEGATE data and all other documentary evidence produced by the appellant, including the reconciliation statement placed before this Tribunal. The adjudicating authority shall independently verify the export particulars without rejecting the same solely on the ground of non-production of any particular format of document and shall thereafter pass a fresh speaking order after affording reasonable opportunity to the appellant. Needless to state, the adjudicating authority shall consider all documentary evidence already produced as well as any further evidence that may be furnished by the appellant during the remand proceedings. As we are remanding the matter on the ground of incomplete verification, we refrain from recording any final finding on limitation and leave the issue open for consideration by the adjudicating authority. All issues are kept open.

17. In view of the foregoing findings, we find that the impugned proceedings suffer from incomplete verification and inadequate examination of the evidence produced by the appellant. Since the resolution of the dispute essentially depends upon reconciliation and verification of the records placed before the authorities, the orders of the Lower Adjudicating Authority are not sustainable and so ordered to be set aside. Consequently, the matter is remanded to the adjudicating authority for fresh adjudication in accordance with the law and on the basis of observations made herein above. The adjudicating authority shall examine the reconciliation statement and all supporting records, afford a reasonable opportunity of hearing and thereafter pass a fresh speaking order. All contentions of both the sides, including those relating to limitation, confiscation, redemption fine and penalty, are left open. Thus, the appeal is allowed by way of remand.

(Order pronounced in open court on 01.07.2026)

Author Bio