Month: March 2026

2,081 articlesGoods and Services Tax

Goods and Services Tax

Allahabad HC: Goods Release Ordered as Invoice Value Applies Under Sec. 129(1)(a)

Excise Duty

Excise Duty

CENVAT Credit Allowed as ISD Registration Requirement Was Only Procedural: CESTAT Bangalore

Service Tax

Service Tax

Service Tax Demand Set Aside as Overseas Branch Cannot Provide Service to Itself

Service Tax

Service Tax

Service Tax Demand Set Aside as Residential Construction Activity before 01.07.2010 Was Not Taxable

Income Tax

Income Tax

Bombay HC Quashed Assessment Order as No SCN Issued Under Section 69

Corporate Law

Corporate Law

Land Acquisition Challenge Rejected as Objections Were Filed Within Statutory Time Limit

CA, CS, CMA

CA, CS, CMA

Bank Audit Manual 2025-2026

Income Tax

Income Tax

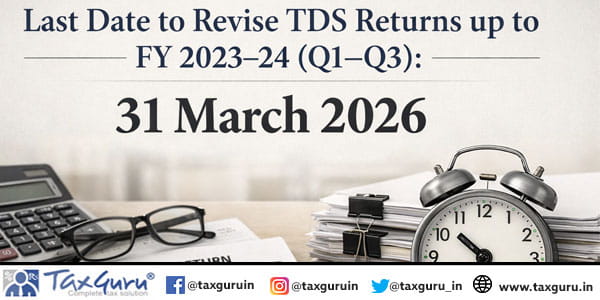

Last Date to Revise TDS Returns up to FY 2023–24 (Q1–Q3): 31 March 2026

Company Law

Company Law

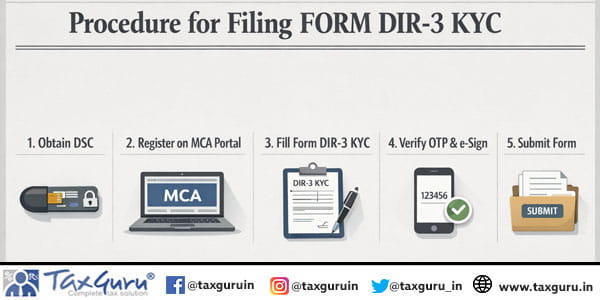

Procedure for filing FORM DIR-3 KYC

Income Tax

Income Tax