Month: March 2026

2,081 articlesIncome Tax

Income Tax

Karnataka HC Quashes TDS Refund on Land Acquisition Over Suppression; ₹5L Cost

Income Tax

Income Tax

Inflated Stock Statement to Bank Justifies Income Addition as Practice Held Commercial Immorality: J&K HC

Income Tax

Income Tax

Section 89(1) Relief Cannot Be Denied for Non-Filing of Form 10E Before ITR Due Date: ITAT Gauhati

Corporate Law

Corporate Law

P&H HC Denies Bail To YouTuber Jyoti Malhotra For Espionage

Company Law

Company Law

The Corporate Gudi – Opportunity to File Pending ROC Forms

Income Tax

Income Tax

Assessment Order Passed in Name of Deceased Assessee Held Void: Karnataka HC

Corporate Law

Corporate Law

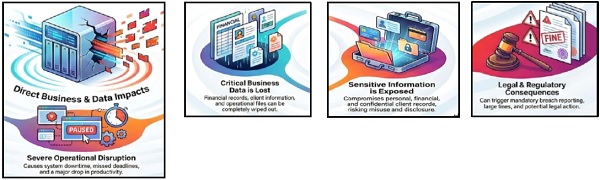

Advisory on Ransomware Groups Targeting NAS Devices used by CA & Consulting Firms

Corporate Law

Corporate Law

No Legal Basis to Ban Kambala Outside Coastal Karnataka, Rules High Court

Corporate Law

Corporate Law

Dismissal of public servant without departmental inquiry not justifiable

Corporate Law

Corporate Law