Month: January 2026

2,391 articlesIncome Tax

Income Tax

Section 69 Cannot Be Invoked for Recorded Share Investments Merely for Premium Mismatch

Income Tax

Income Tax

Survey Disclosure Accepted in Return Cannot Trigger Section 270A Penalty: ITAT Mumbai

Income Tax

Income Tax

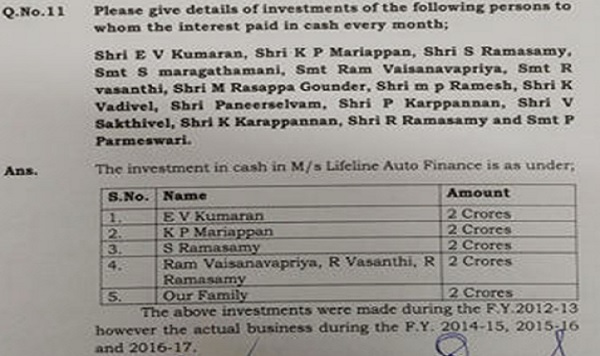

₹2 Crore Section 69 Addition Quashed Due to Uncorroborated Loose Sheets

Corporate Law

Corporate Law

Guidelines on Reinvestment of Returned and Pending Amounts into PRANs

Income Tax

Income Tax

Reassessment Addition Based Solely on Retracted Third-Party Statements Quashed: ITAT Mumbai

DGFT

DGFT

DGFT Announced Second Round of Gold TRQ Allocation for India–UAE CEPA

Income Tax

Income Tax

Reassessment Quashed for Failure to Record Reasons Under Section 148: ITAT Mumbai

Income Tax

Income Tax

ITAT Hyderabad Condoned 506-Day Delay; Ad Spend Allowed; Alleged Coerced Share Sale Ground Admitted

Finance

Finance

Registration of FME – Non-Retail in Gift City SEZ / IFSC

Income Tax

Income Tax