The Securities and Exchange Board of India (SEBI) has released a consultation paper proposing the introduction of a New Asset Class aimed at bridging the gap between Mutual Funds (MFs) and Portfolio Management Services (PMS). This New Asset Class is designed to offer higher risk-taking capabilities and a higher ticket size to regulated investment products, addressing the proliferation of unregistered and unauthorized investment schemes. The investment landscape in India has evolved with various products meeting the needs of retail, high net-worth, and institutional investors. The proposed asset class targets investors desiring flexibility in portfolio construction, positioning itself between MFs and PMS in terms of risk and investment size. The consultation paper suggests that the New Asset Class will operate under the MF structure with relaxed prudential norms and higher minimum investment requirements to attract appropriate investors while ensuring regulatory compliance. SEBI also outlines eligibility criteria for existing and new mutual funds to launch this asset class, emphasizing the importance of experienced fund management. Branding and regulatory distinctions are proposed to avoid confusion with traditional MFs. The paper invites public comments on various aspects, including nomenclature, eligibility criteria, registration requirements, permissible investments, and investment restrictions. It also explores the potential of the New Asset Class to engage in derivative transactions beyond hedging and rebalancing. The minimum investment threshold is set at INR 10 lakh to deter retail investors and attract those with substantial investible funds. SEBI aims to ensure investor protection and market integrity by introducing this structured and regulated investment product.

Securities and Exchange Board of India

CONSULTATION PAPER ON INTRODUCTION OF NEW ASSET CLASS/ PRODUCT CATEGORY

Jul 16, 2024 | Reports : Reports for Public Comments

Click here to provide your comments

1. Objective

1.1. The objective of this consultation paper is to solicit comments on the proposed introduction of new asset class/ product category (hereinafter referred to as ‘New Asset Class’) aimed at bridging the gap between Mutual Funds and Portfolio Management Services (hereinafter referred to as ‘PMS’) in terms of flexibility in portfolio construction. The proposed New Asset Class seeks to provide investors with a regulated investment product featuring higher risk-taking capabilities and a higher ticket size, aimed at curbing the proliferation of unregistered and unauthorized investment products.

2. Background

2.1. The landscape of investment management in India has significantly evolved over the years, marked by the introduction and development of various investment products. SEBI has adopted a segmented risk-based approach to regulation of these products depending on their complexity, sophistication of target investors, minimum investment size etc., with the over-arching objective of diversifying investment avenues while protecting the interest of investors.

2.2. The current range of investment products with varying risk-reward profiles, are intended to meet the investment needs of retail, high net-worth and institutional investors. These products include Mutual Fund schemes which are retail oriented with a low ticket size, portfolio management services with a ticket size of INR 50 lakhs and Alternative Investment Funds with a minimum investment value of INR 1 crores. The regulatory framework and prudential norms governing these investment vehicles become progressively more flexible from Mutual Funds (‘MFs’) to AIFs, in sync with the increasing minimum investment size along this spectrum.

2.3. Over the years, a notable opportunity of a New Asset Class has emerged between Mutual Funds and PMS in terms of flexibility in portfolio construction.

2.4. The absence of such an investment product appears to have inadvertently propelled the investors of this segment towards unregistered and unauthorized investment schemes/entities. Such schemes/entities, often promise unrealistically high returns and exploit the investors’ expectations for better yields, leading to potential financial risks. Therefore, a New Asset Class would provide a regulated and structured investment suited to the investors in this segment.

2.5. Considering that the New Asset Class is intended to have a risk-return profile between MFs and PMS, the proposed regulatory framework needs to accordingly enable higher risk-taking than Mutual Funds, while containing commensurate safeguards and risk mitigation measures. The New Asset Class is proposed to be introduced under the Mutual Fund structure, with relaxations in prudential norms for such New Asset Class to be adequately effective. While such relaxations may enhance the risks associated with the product, the same can be mitigated by putting a higher limit on minimum investment size.

2.6. Thus, the proposed New Asset Class intends to fill the gap between MFs and PMS by offering a regulated product featuring greater flexibility, higher risk-taking capability

and a higher ticket size, to meet the needs of the emerging category of investors.

2.7. It is also proposed to have a distinct nomenclature for the New Asset Class to distinguish it from traditional Mutual Funds and other investment products already available in the securities market such as PMS, AIF, REITs, INVITs etc.

Consultation Proposal 1:

Comments/suggestions for the nomenclature of the ‘New Asset Class’.

3. Eligibility Criteria

3.1. In order to facilitate existing as well as newly registered Mutual Funds/ Asset Management Companies (‘AMCs’) to offer products under the New Asset Class, the following two routes of eligibility criteria are proposed.

3.2. Route 1: Strong track record

All registered Mutual Funds fulfilling the below mentioned criteria shall be eligible to launch the New Asset Class:

3.2.1. Mutual Fund shall be in operation for minimum of 3 years and has average Asset Under Management (‘AUM’) of not less than INR 10,000 crores, in immediately preceding 3 years.

3.2.2. No action initiated or taken against the sponsor/AMC under section 11, 11B, and/or Section 24 of the SEBI Act, 1992 during the last 3 years.

3.3. Route 2: Alternate Route

All newly registered as well as existing Mutual Funds, not fulfilling the requirements under Route 1 above, shall also be eligible to launch the New Asset Class, subject to compliance with the following requirements:

3.3.1. AMC shall appoint:

- A Chief Investment Officer (‘CIO’) for the New Asset Class with an experience of fund management of at least 10 years and managing AUM of not less than 5,000 crores, AND

- An additional Fund Manager for the New Asset Class with experience of fund management of at least 7 years and managing AUM of not less than 3,000 cr. 3.3.2. No action initiated or taken against the sponsor/AMC under section 11, 11B, and/or Section 24 of the SEBI Act, 1992 during the last 3 years.

Consultation Proposal 2:

Whether the eligibility criteria mentioned under Strong Track Record route and Alternate route, as specified in para 3.2 & 3.3 above, are appropriate? Please provide comments/suggestions with appropriate rationale.

Consultation Proposal 3:

Comments/suggestions on any other criteria of eligibility for the New Asset Class that can be considered?

4. Registration and Approval Requirements

4.1. The Trustees/sponsor of a Mutual Fund shall file an application, along with nonrefundable application fees, with SEBI for providing services under the New Asset Class, along with the required undertakings and documentation.

4.2. SEBI, upon being satisfied that the applicant fulfils the necessary requirements, shall provide its approval to the applicant to commence operations under the New Asset Class.

4.3. The registration process for New Asset Class shall be a two-stage process, consisting of in-principle and final approvals, similar to the registration process currently followed for Mutual Funds.

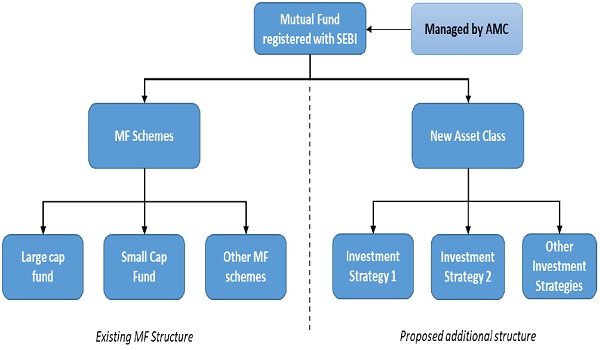

4.4. While the sponsor may not be required to maintain segregated net worth or infrastructure specifically for the New Asset Class, the New Asset Class shall represent a new arm/service offered under the broader umbrella of Mutual Funds. The illustration of the same is provided below:

4.5. All provisions of existing SEBI (Mutual Funds) Regulations, 1996, SEBI Master Circular for Mutual Funds and any other circular issued thereunder shall apply to the New Asset Class unless otherwise specified, ensuring a consistent regulatory approach and investor protection measures.

Consultation Proposal 4:

Whether the proposals mentioned under para 4 above are appropriate? Please

provide comments/suggestions with appropriate rationale.

5. Branding of the New Asset Class

5.1. As the products offered under the New Asset Class will be relatively riskier than the schemes offered by the traditional Mutual Funds, it is essential to maintain a clear distinction between the branding of products under the New Asset Class and those under the traditional Mutual Funds.

5.2. To achieve this, it is proposed that the New Asset Class is positioned as a product distinct from the traditional Mutual Funds, both from branding and advertisement perspectives, including the manner of usage, if any, of the sponsor/AMC’s brand or logo.

5.3. The distinction in branding may be made, for example, through the use of specific nomenclature and disclaimers in advertisements of products under the New Asset Class. This shall aid in ensuring that any potential misconduct/ failure in performance of the New Asset Class does not result in brand contamination or negatively impacting the confidence and trust in the traditional Mutual Funds.

Consultation Proposal 5:

Whether the proposals regarding branding of the New Asset Class mentioned under para 5 above are appropriate? Please provide comments/suggestions with appropriate rationale.

Consultation Proposal 6:

In addition to the proposals mentioned under para 5.3, what other branding or advertising guidelines or restrictions should be considered to ensure distinction between Mutual Funds and products under the New Asset Class?

6. Structure of the New Asset Class

6.1. Under the New Asset Class, the AMC can offer ‘Investment Strategies’ under pooled fund structure, akin to Mutual Funds schemes. This nomenclature (or any other appropriate nomenclature, received during consultation) is proposed in order to differentiate between the mutual fund schemes currently being managed by the AMCs and the schemes under the New Asset Class.

6.2. The redemption frequency of these ‘Investment Strategies’ can be tailored (i.e. daily/weekly/fortnightly/monthly/quarterly/annually/fixed maturity) based on the nature of investments to allow the investment manager to adequately manage liquidity without imposing undue constrains on investors.

6.3. AMCs may implement appropriate notice or settlement periods for redemption from these funds to protect the interest of investors.

6.4. The units of the investment strategies may also be listed on the recognized stock exchanges, particularly for units of investment strategies with redemption frequency greater than a week.

6.5. No Investment Strategy shall be launched by the AMCs unless such Investment Strategy is approved by the trustees, and subject to issuance of final observations on the offer documents by SEBI.

6.6. All provisions regarding the offer documents shall be on par with that of Mutual Fund schemes unless specified otherwise.

6.7. Only ‘Investment Strategies’ that are specified by SEBI from time to time, can be launched under the New Asset Class. For example, some of the investment strategies that may be permitted are illustrated below:

6.7.1. Long-short Equity Fund: A fund that seeks to deliver returns by taking long and short positions in equity and equity-related instruments. For e.g. the fund may be bullish on automobile sector and bearish on IT sector, and may invest in both these sectors by going long on automobile sector and short on IT sector.

6.7.2. Inverse ETF/Fund: A fund that seeks to generate returns that are negatively correlated to the returns of the underlying index.

| Consultation Proposal 7:

Is the nomenclature ‘Investment Strategy’ appropriate for the products/schemes offered under the New Asset Class? Please provide comments/suggestions with appropriate rationale. For better understanding, products launched under Mutual Funds are called ‘Schemes’, whereas products offered under PMS are usually termed as ‘Investment Approaches’. Consultation Proposal 8: Whether the overall structure of the New Asset Class, as specified in para 6 above, is appropriate? Consultation Proposal 9: What are your suggestions for various potential ‘Investment Strategies’ that can be launched under the New Asset Class as mentioned in para 6.7? |

7. Minimum Investment Threshold

7.1. The minimum investment amount for investment under the New Asset Class shall be INR 10 lakh per investor at the level of the New Asset Class within the AMC/MF. This means an investor must invest a minimum of INR 10 lakh, across one or more investment strategies, under the New Asset Class offered by an AMC/MF. This threshold shall deter retail investors from investing in this product, while attracting investors, with investible funds between INR 10 lacs – INR 50 lacs, who are today being drawn to unauthorized and unregistered portfolio management service providers.

7.2. Investors may also have an option of systematic plans such as Systematic Investment Plan (‘SIP’), Systematic Withdrawal Plan (‘SWP’) and Systematic Transfer Plan (‘STP’) for investment strategies under the New Asset Class.

7.3. At no point in time should the total invested amount of an investor fall below INR 10 lakh due to actions of the investor such as withdrawals or systematic transactions etc. However, the total amount may fall below INR 10 lakh due to depletion of the value of investments.

Consultation Proposal 10:

Whether the minimum investment threshold of INR 10 lakh is appropriate? Please provide your comments/suggestions with appropriate rationale.

Consultation Proposal 11:

Should the minimum investment threshold be applied at the per investment strategy level or at the level of New Asset Class within an AMC/MF?

8. Permissible Investments

8.1. All investments permissible to Mutual Funds under the SEBI (Mutual Funds) Regulations, 1996 shall be available for the New Asset Class.

8.2. Additionally, the New Asset Class shall be able to take exposure in derivatives for purposes other than hedging and portfolio rebalancing, subject to compliance with relevant provisions. This will provide more flexibility and risk-taking in investments and potentially generate higher returns.

8.3. The ‘Investment Strategies’ shall not borrow for the purpose of investments except to meet temporary liquidity needs of the New Asset Class for repurchase, redemption of units or payment of interest or dividend to the unitholders, as currently applicable in the case of Mutual Funds.

| Consultation Proposal 12:

Whether any other investments, apart from those permitted to Mutual Funds and as mentioned in para 8 above, be made available for investments under the New Asset Class? Please provide comments/suggestions with appropriate rationale. Consultation Proposal 13: Whether the New Asset Class should be allowed to take exposure in derivatives for purposes other than hedging and portfolio rebalancing? Please provide comments/suggestions with appropriate rationale. |

9. Relaxations to the investment restrictions

Schedule VII of the SEBI (Mutual Funds) Regulations, 1996 provides restrictions on investments for Mutual Fund schemes. Additionally, SEBI Master Circular for Mutual Funds also provide certain restrictions on investments by Mutual Funds. However, for the purpose of the New Asset Class, the proposed relaxations to the investment restrictions are as follows:

| Sr. No. | Details | Existing limits under MF Regulations |

Proposed limits for New Asset Class |

| 9.1 | Minimum investment size | INR 500 (some MFs also accept SIP of as low as INR 100) | INR 10 lakh per investor across investment strategies at the level of New Asset Class within the AMC/MF |

| 9.2 | Single issuer limit for debt securities (Refer: Clause 1 of seventh schedule of MF Regulations) | 10% of NAV

(+2% with approval of trustees and AMC Board) |

20% of NAV

(+5% with approval of trustees and AMC Board) |

| 9.3 | Credit risk based single issuer limit for debt securities (Refer: Clause 12.8.3.1 of Master Circular for Mutual Funds) | AAA – 10% of NAV

AA – 8% of NAV A & below – 6% of NAV (+2% with approval of trustees and AMC Board) |

AAA – 20% of NAV

AA – 16% of NAV A & below – 12% of NAV (+5% with approval of trustees and AMC Board) |

| 9.4 | Ownership of paid-up capital carrying voting rights (Refer: Clause 2 of seventh schedule of MF Regulations) | 10% | 15% |

| 9.5 | Percentage of NAV in equity and equity related instruments of any company (Refer: Clause 9 of seventh schedule of MF Regulations) | 10% | 15% |

| 9.6 | Investment in REITs & InvITs (Refer: Clause 13 of seventh schedule of MF Regulations) |

Single issuer limit at Mutual Fund level across all schemes – 10% |

Single issuer limit at New Asset Class level across all investment strategies – 20% |

| No scheme shall invest more than 10% of NAV in units of REITs and INVITs with not more than 5% of its NAV in

units of REIT and INVIT issued by a single issuer |

No scheme shall invest more than 20% of NAV in units of REITs and INVITs with not more than 10% of its NAV in units of REIT and INVIT issued by a single issuer |

||

| 9.7 | Sector level limits for debt securities (Refer: Clause 12.9.1 of Master Circular for Mutual Funds) | 20% in a particular sector | 25% in a particular sector |

| 9.8 | Derivatives | Allowed only for the purpose of hedging and portfolio rebalancing |

May also be allowed for the purpose of taking exposure |

Consultation Proposal 14:

Whether the relaxations from the provisions of the MF Regulations and Master Circular, as specified at para 9 above, are appropriate? Please provide comments/suggestions with appropriate rationale.

Consultation Proposal 15:

Any other relaxations/restrictions that may be considered for the New Asset Class? Please provide comments/suggestions with appropriate rationale.

10. Investment in derivatives

10.1. The investment strategies under the New Asset Class may invest in derivatives or derivative strategies as a way of taking exposure in the Market.

10.2. The cumulative gross exposure through all investable instruments including derivatives and any other instruments as may be permitted by SEBI from time to time should not exceed 100% of the net assets of the investment strategy. The following conditions may additionally be specified:

10.2.1. The total exposure through exchange traded derivative instruments shall not exceed 50% of the net assets of an investment strategy.

a. Further, the total exposure through derivatives of a single stock shall not exceed 10% of the net assets of an investment strategy.

Illustration: For para 10.2.1(a) and 9.5 read together:

| Exposure in derivatives segment | Exposure in

equity segment |

Acceptable (✓) /Not acceptable (X) |

|

| Maximum exposure in ABC Ltd. | 0%

|

15%

(Acceptable in line with para 9.5) |

✓ |

| Maximum exposure in ABC Ltd. | 10%

|

5% | ✓ |

| Maximum exposure in ABC Ltd. | 11%

(breach of para 10.2.1(a) |

4% | X

(as the exposure to derivatives segment of ABC is more than 10%) |

| Maximum exposure in ABC Ltd. | 7%

|

10% | X

(as it |

b) Such limit of 50% shall not be applicable in case of Index funds/ETFs launched under the New Asset Class, on such indices (for example broad based, non-bespoke indices) as may be specified by SEBI.

10.3. The total exposure at any point of time shall be the sum of exposure through instruments in both the cash market and derivatives market.

10.4. The exposure shall be calculated as below:

10.4.1. Futures (long and short) = Futures Price * Lot Size * Number of Contracts

10.4.2. Options bought = Option premium paid * Lot size * Number of contracts

10.4.3. Options sold = Market price of the underlying * Lot size * Number of contracts

10.4.4. In case of any other derivative exposure, the exposure is proposed to be calculated as the notional market value of the contract.

10.5. Sum of all exposures, excluding offsetting transactions, shall be termed as ‘Gross Exposure’. Offsetting of positions at the portfolio level shall be allowed for cash and derivatives as well as between derivative positions (i.e. on the basis of futures equivalent exposure).

10.6. NAV of the investment strategy shall be the sum of value of all securities adjusted for mark to market gains/losses (including cash and cash equivalents).

The illustrative example for the above provisions is provided at

Annexure A.

Consultation Proposal 16:

Whether the proposal under para 10 above is appropriate? Provide comments/suggestions with appropriate rationale.

Consultation Proposal 17:

Whether the limit of 50% on the exposure in derivative segment, as specified in para 10.2.1, is appropriate?

11. Disclosures

11.1. Risk-o-meter: Similar to Mutual Fund schemes, the investment strategies under the New Asset Class shall also be categorized under a Risk-o-meter. However, to avoid any confusion amongst investors, the Risk-o-meter for the New Asset Class shall have a different depiction and nomenclature than that of Mutual Fund schemes. For example, the nomenclature for the same could be ‘Risk Band’ and depiction could be as shown below:

11.2. Portfolio Disclosure: The New Asset Class shall disclose portfolio of all its ‘Investment Strategies’ on its website on monthly basis.

11.3. Constitutional documents: All constitutional documents (i.e. SID/SAI/KIM) shall be publicly available.

Consultation Proposal 18:

Whether the nomenclature and depiction of Risk Band suggested at para 11.1 above, is appropriate? Please provide your comments/suggestions with appropriate rationale.

Consultation Proposal 19:

Whether provisions regarding Portfolio Disclosure, frequency of such disclosure and constitutional documents, as specified at para 11.2 & 11.3, are appropriate?

Consultation Proposal 20:

What additional information, if any, should be disclosed to the public regarding the investment strategies under the New Asset Class, to enhance transparency and investor protection?

12. Global Practices

12.1. Global practices: Analysis of global practices relevant to the proposed New Asset Class is placed at Annexure B.

Consultation Proposal 21:

Any other suggestions or comments on the overall proposal for the New Asset Class as outlined in this Consultation paper?

*****

Public Comments on this Consultation Paper

1. Public Comments

Public comments are invited on the proposal of ‘Introduction of New Asset Class/ Product Category’. The comments/ suggestions should be submitted through the following mode latest by August 06, 2024:-

- Online web-based form

a) The comments may be submitted through the following link: https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doP ublicComments=yes

b) The instructions to submit comments on the consultation paper are as under:

i Before initiating the process, please read the instructions given on top left of the web form as “Instructions”.

ii. Select the consultation paper you want to comment upon from the dropdown under the tab – “Consultation Paper” after entering the requisite information in the form.

iii. All fields in the form are mandatory;

iv. Email Id and phone number cannot be used more than once for providing comments on a particular consultation paper.

v. If you represent any organization other than the types mentioned under dropdown in “Organization Type”, please select “Others” and mention the type, which suits you best. Similarly, if you do not represent any organization, you may select “Others” and mention “Not Applicable” in the text box.

vi. There will be a dropdown of Proposals in the form. Please select the proposals one- by-one and for each of the proposal, please record your level of agreement with the selected proposal. Please note that submission of agreement level is mandatory.

vii. If you want to provide your comments for the selected proposal, please select “Yes” from the dropdown under “Do you want to comment on the proposal” and use the text boxes provided for the same.

viii. After recording your response to the proposal, click on “Submit” button. System will save your response to the selected proposal and prompt you to record your response for the next proposal. Please follow this procedure for all the proposals given in the dropdown.

ix. If you do not want to react on any proposal, please select that proposal from the dropdown and click on “Skip this proposal” and move to the next proposal.

x. After recording your response to all the proposals, you may see your draft response to all of proposals by clicking on “Check your response before submitting” just before submitting response to the last proposal in the dropdown. A pdf copy of the response can also be downloaded from the link given in right bottom of the web page.

xi. The final comments shall be submitted only after recording your response on all of the proposals in the consultation paper.

c) In case of any technical issue in submitting your comments through web based public comments form, you may contact the following through email with a subject “Consultation Paper on Introduction of New Asset Class/ Product Category”:

i. Mr. Peter Mardi, Deputy General Manager (peterm@sebi.gov.in)

ii. Mr. Rushikesh Vijay Bhopatrao, Assistant Manager (rushikeshb@sebi.gov.in)

Issued on: July 16, 2024

Annexure A – Illustration on investments in derivatives

Investment Strategy ‘ABC Fund’ has AUM of INR 10 crore. The following table specifies the list of securities identified for investment:

| Security | Value | Lot size |

| Index 50 | 22,000 | 25 |

| XYZ Ltd. | 2,000 | 500 |

The following table illustrates the maximum amount/contracts that can be bought/sold:

| Details | Provisions / Exposure calculation | Actual amount |

| Maximum amount that can be invested in equity derivatives |

Max 50% | INR 5 crore |

| Maximum number of Index-50 Index Future contracts that can be bought/sold |

Futures (long and short) = Futures Price * Lot Size * Number of Contracts | 90 contracts = 5 crore / (22000 * 25) |

| Maximum number of Index-50 call/put option contracts, trading at INR 100, that can be shorted | Options sold = Market price of the underlying * Lot size * Number of contracts |

90 contracts = 5 crore / (22000*25) |

| Maximum number of Index-50 call/put option contracts, trading at INR 100, that can be bought | Options bought = Option premium paid * Lot size * Number of contracts | 20000 contracts = 5 crore / (100*25) |

| Maximum number of XYZ Ltd. call/put option contracts, trading at INR 50, that can be shorted | Options sold = Market price of the underlying * Lot size * Number of contracts Exposure to single stock derivatives cannot be more than 10% of net assets. Ref. para 10.2.1(a) |

10 contracts = 1 crore / (2000*500) |

| Maximum number of XYZ Ltd. call/put option contracts, trading at INR 50, that can be bought | Options bought = Option premium paid * Lot size * Number of contracts

Exposure to single stock derivatives cannot be more than 10% of net assets. Ref. para 10.2.1(a) |

400 contracts = 1 crore / (50*500) |

Annexure B – Global practices

1. Liquid Alternative Funds/ Hedge Funds Lite structure in United States of America (‘USA’) 1 2

1.1. Introduction: Hedge fund lite or liquid alternatives refer to investment vehicles that employ hedge fund like strategies but are available to a broader range of investors, offering greater liquidity than traditional hedge funds. These funds aim to provide access to alternative investment strategies, including long/short equity, event-driven and managed futures, but with the liquidity of mutual funds.

1.2. They are designed to give retail and smaller institutional investors exposure to hedge fund-like returns and diversification benefits while mitigating some of the risks and lock-in periods associated with traditional hedge funds.

1.3. Regulatory Framework: These funds in the USA are primarily regulated by Securities and Exchange Commission (SEC) under the Investment Company Act of 1940, as they are often structured as mutual funds (1940 Act funds) or Exchange-Traded Funds (ETFs). Under this framework, Liquid Alternatives are subjected to more stringent regulations than those applied to traditional hedge funds, including liquidity requirements, leverage limitations, and diversification standards.

1.4. Minimum Investment Size: The minimum investment size for hedge fund lite or liquid alternatives can vary significantly depending on the fund and its management. However, as they are structured to be more accessible to retail investors than traditional hedge funds, the minimum investments are generally much lower and usually within minimum investment requirements ranging from USD 1,000 to USD 10,000.

1.5. Examples of Liquid Alternatives or Hedge Fund lite in USA:

1.5.1. AQR Long-Short Equity Fund – The Fund seeks to deliver positive returns by taking long and short positions in equity and equity-related instruments that are deemed to be relatively attractive or unattractive, respectively, based on AQR’s investment models.3 (AUM – USD 1.1 billion as on January 2024, Management Fee and Cost – 1.36%)

1.5.2. FS Managed Futures Fund 4 – The Fund seeks to achieve its investment objective by actively allocating its assets across a broad spectrum of alternative investment strategies. It may provide exposure to alternative strategies across the five major asset classes (commodities, currencies, fixed income, equities and credit).

2. Inverse Funds/ETFs & Bear Funds in Australia5

2.1. Introduction: Inverse funds, often referred to as bear funds, are specialized investment vehicles designed to profit from a decline in the value of an underlying benchmark or asset class. In Australia, as in other markets, these funds use derivatives such as futures and swaps to achieve their investment objectives, offering investors a way to hedge against market downturns or to speculate on market declines.

2.2. Regulatory Framework: Inverse funds, in Australia, are regulated by the Australian Securities and Investments Commission (ASIC) under the Corporations Act 2001. They are subject to the same regulatory standards as other managed funds, including requirements for transparency, fair dealing, and investor protection. Obtaining Australian Financial Services License (AFSL) is mandatory for providing these funds.

2.3. Minimum Investment Size: While the minimum investment in inverse funds can vary widely depending on the fund provider and the specific fund, mostly under ETF structure, one can buy or sell units of the fund like any other stock listed on the Australian Stock Exchanges.

2.4. Types of inverse funds: Inverse funds in Australia typically focus on major indices, such as the ASX 200, or specific sectors. They can be broadly categorized into:

- Single Inverse Funds: Aim to deliver the inverse (opposite) daily performance of their benchmark index.

- Leveraged Inverse Funds: Seek to deliver multiple times the inverse daily performance of the benchmark, amplifying both potential gains and losses.

2.5. Examples of Inverse funds/Bear Funds in Australia:

2.5.1. Australian Equities Bear Hedge Fund (ASX: BEAR)6 7: BEAR seeks to generate returns that are negatively correlated to the returns of the Australian Share market. (AUM – $A 47 Million as on January 2024, Management Fee and Cost – 1.48%)

2.5.2. Australian Equities Strong Bear Hedge Fund (ASX: BBOZ8): BBOZ seeks to generate magnified returns (by employing leverage) that are negatively correlated to the returns of the Australian Share market. (AUM – $A 379 Million as on January 2024, Management Fee and Cost – 1.38%)

Notes:-

1 Reference – Investopedia

2 Reference – finra.org

3 https://funds.aqr.com/funds/aqr-long-short-equity-fund#about

4 https://www.morningstar.com/funds/xnas/fmgfx/quote

5 https://www.betashares.com.au/category/inverse-etfs/

6 https://www.betashares.com.au/fund/australian-equities-bear-fund/

7 https://www.betashares.com.au/files/factsheets/BEAR-Factsheet.pdf

8 https://www.betashares.com.au/fund/australian-equities-strong-bear-fund/

SEBI’s initiative to introduce a new asset class is an important development for the investment ecosystem. Such regulated investment products can provide investors with more choices while maintaining transparency and risk awareness. Financial research platforms like Kapitales Research help investors stay updated with evolving market trends and investment opportunities.