The Securities and Exchange Board of India (SEBI) has released a consultation paper seeking public feedback on expanding the scope of the sustainable finance framework within the Indian securities market. This move aligns with recent budget announcements aimed at simplifying compliance and promoting sustainable finance. The paper proposes redefining “green debt security” to “sustainability-linked security” to encompass a broader range of instruments beyond environmental sustainability, including Social, Sustainable, and Sustainability-linked Bonds, collectively termed ESG Debt Securities. The proposal also includes introducing a framework for Sustainable Securitised Debt Instruments, which would allow originators to pool assets tied to sustainable finance and offer them as securities. SEBI aims to align these frameworks with international standards like the Green Bond Principles of the International Capital Market Association (ICMA), while adapting them to Indian requirements. Additionally, SEBI suggests implementing mandatory independent external reviews to ensure transparency and credibility in ESG Debt Securities and Sustainable Securitised Debt Instruments. The consultation paper emphasizes the need for a robust framework to support India’s commitments to sustainable development and climate action, and invites public comments on these proposals by September 6, 2024.

Securities and Exchange Board of India

DEPARTMENT OF DEBT AND HYBRID SECURITIES – POD I

Consultation Paper on Expanding the Scope of Sustainable Finance Framework in The Indian Securities Market

Dated: Aug 16, 2024 | Reports : Reports for Public Comments

Click here to provide your comments

Timeline to Respond

Comments on the Consultation paper (CP) may be sent by September 06, 2024

1. OBJECTIVE

1.1. The objective of this consultation paper is to seek comments, views and suggestions from the public on the proposals related to expanding the scope of sustainable finance framework in the Indian securities market.

1.2. The Hon’ble Finance Minister in the budget announcements for FY 2023-24, inter-alia, made an announcement to simplify, ease and reduce cost of compliance for participants in the financial sector through a consultative approach.

1.3. Accordingly, to align the process of review with the budget announcement, a working group for review of compliance requirements under SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021(hereinafter ‘NCS Regulations’) was formed, which recommended certain measures to promote the ease of doing business for issuance of non-convertible securities.

1.4. One of the recommendations of the working group was to redefine “green debt security” as “sustainability-linked security” as sustainability-linked security would cover a wider spectrum of sustainable finance instruments whereas green debt securities appears to only reflect the instruments related to environmental sustainability.

1.5. Further, SEBI is in receipt of representation from market participants including Confederation of Indian Industry (CII) to expand the scope of regulatory framework pertaining to sustainable finance to include Social Bonds, Sustainable Bonds and Sustainability-linked Bonds in addition to existing Green Debt Securities as a mode of raising sustainable finance, in line with global practices. These securities (Green Debt Securities, Social Bonds, Sustainable Bonds, and Sustainability-linked Bonds) are at times termed as Environment, Social and Governance (ESG) Debt Securities.

1.6. It is also noteworthy that the Hon’ble Finance Minister in the budget announcements for FY 2024-25, inter-alia mentioned that taxonomy for climate finance for enhancing the availability of capital for climate adaptation and mitigation will be developed. This will support achievement of the country’s climate commitments and green transition. Its notable that Green Debt Securities inter-alia includes climate change adaptation as one of the eligible categories for raising funds through issuance of Green Debt Securities, and such taxonomy can accordingly be useful and benefit Indian corporate issuers.

1.8. Building on all these feedback and developments, it is proposed to provide for a framework for Social Bonds, Sustainable Bonds and Sustainability Linked Bonds, Further, it is also proposed to introduce the concept of Sustainable Securitised Debt Instruments

1.9. The detailed proposals and consultation matters are mentioned in Paragraph 3 to 5 of this consultation Paper.

2. Background and Need for Review:

2.1. The 2030 Agenda for Sustainable Development1, adopted by all United Nations Member States in 2015, provides a shared blueprint for peace and prosperity for people and the planet, now and into the future. At its heart are the 17 Sustainable Development Goals (SDGs)2, which are an urgent call for action by all countries – developed and developing – in a global partnership. They recognize that ending poverty and other deprivations must go hand-in-hand with strategies that improve health and education, reduce inequality, and spur economic growth – all while tackling climate change and working to preserve our oceans and forests. The SDGs highlight the strong interconnections between the environmental, social and economic aspects of sustainable development.

2.2 A tremendous amount of financing is required to achieve the Sustainable Development Goals. As per World Bank3, sustainable finance is the process of taking due account of ESG considerations when making investment decisions in the financial sector, leading to increased longer-term investments into sustainable economic activities and projects.

2.3 The bond markets offers a relatively long-term asset class that matches the profile of SDG activities with the scale to fill the SDG financing gap.

2.4 Accordingly, SEBI introduced the regulatory framework for listed issuances of green debt securities as a mode of sustainable finance, in 2017.

2.5 SEBI undertook a review of the regulatory framework for green debt securities with a view to align the extant framework for green debt securities with the updated Green Bond Principles (GBP) of International Capital Market Association (ICMA), which are recognised by International Organization of Securities Commissions (IOSCO). Accordingly, in February 2023, SEBI revamped the regulatory framework pertaining to issuance of green debt securities by:

2.5.1 enhancing the scope of definition of ‘green debt security’ by including new modes of sustainable finance in relation to pollution prevention and control, eco-efficient products, etc.;

2.5.2 Introducing the concept of blue bonds (related to water management and marine sector), yellow bonds (related to solar energy) and transition bonds as sub categories of Green debt securities.

2.5.3 For a complete definition of ‘green debt securities’ please refer to Annexure – I.

2.6 Generally, Thematic Bonds (including ESG Debt securities) are classified into two types:

2.6.1 use of proceeds (UoP) bonds: UoP bonds are securities earmarked for specific projects designed to generate the intended impacts.

2.6.2 key performance indicator (KPI) bonds: KPI bonds are required to meet the overarching goals of sustainability and ESG objectives but are not tied to any project or specified output like UoP bonds.4

2.7 SEBI’s extant regulatory framework covers only a limited part of UoP bonds focusing only on the projects/ asset class related to environmental sustainability in terms of the extant definition of Green Debt Securities. It does not cover other classes of UoP Bonds and KPI Bonds as a mode of sustainable finance. Therefore, to enable issuers to tap the market to raise funds through issuance of Social Bonds, Sustainable Bonds and Sustainability Linked Bonds. These together with green debt securities will be termed ESG Debt Securities. It is proposed to introduce the framework for such securities as set out in the subsequent paragraphs.

3. Proposal for introduction of framework for Social Bonds, Sustainable Bonds and Sustainability linked bonds (which together with Green Debt Securities are termed ESG Debt Securities) to expand the sustainable finance in the Indian Securities Market

3.1 It is proposed that for raising sustainable finance, in addition to existing green debt securities, issuers may also raise funds through issuance of social bonds, sustainable bonds and sustainability-linked bonds (together with green debt securities will be termed ESG Debt Securities), and will be in accordance with such international frameworks as adapted or adjusted to suit Indian requirements that are specified by SEBI from time to time. To give effect to this proposal suitable amendments would be made to the NCS regulations.

3.2 In evaluating which international frameworks that are considered suitable and with what adaptation or adjustments that are necessary, SEBI shall draw upon the Industry Standards Forum (ISF) for necessary recommendations and feedback.

3.3 Some of the international frameworks which could be considered are listed below:

- Green Bond Principles5 of ICMA, or

- Social Bond Principles6 of ICMA, or

- Sustainability Bond Guidelines7 of ICMA, or

- Sustainability-Linked Bond Principles8 of ICMA, or

- Climate Bond Standard of the Climate Bond Initiative9

Certain regional groups have also published standards or taxonomies which could be considered by ISF, if are relevant to issuers of ESG Debt Securities or to investors in ESG Debt Securities.

3.4 Initial and continuous disclosure requirements for ESG Debt Securities shall be drawn basis the international frameworks identified, and with such adaptation or adjustments that are necessary. Initial disclosures could be in the offer document for the ESG Debt Securities, while continuous disclosures could be in the Annual Report or the Business Responsibility and Sustainability Report (BRSR) or in such form, manner and substance as may be specified. SEBI shall work with the Industry Standards Forum (ISF) for necessary recommendations and feedback in specifying such disclosure requirements.

| Consultation 1: Introduction of framework for Social Bonds, Sustainable Bonds and Sustainability-linked Bonds (which together with Green Debt Securities are termed ESG Debt Securities) as a mode of sustainable finance

Kindly provide your comments separately for each of the below items along with supporting rationale: 1) Whether the proposal to introduce a framework for Social Bonds, Sustainable Bonds and Sustainability linked Bonds (which together with green debt securities are termed ESG Debt Securities) is appropriate and adequate? 2) Are there any other international frameworks/guidelines in addition to frameworks listed at Para 3.3, that should be considered? |

4. Proposal for introduction of sustainable securitised debt instruments to expand the sustainable finance in the Indian Securities Market

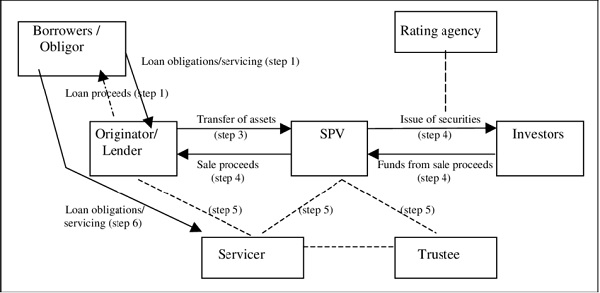

4.1 Securitization is the process in which certain types of assets are pooled so that they can be repackaged into interest-bearing securities. The interest and principal payments from the assets are passed through to the purchasers of the securities10. An illustrative securisation process flow is as under:

Source: https://www.researchgate.net/figure/Securitisation-processfig1317310763

4.2 SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008 (hereinafter referred as ‘SDI Regulations’) inter-alia provide the regulatory framework for issuance and listing of Securitised Debt Instruments (SDIs). Regulation 2(1)(s) of SDI Regulations defines “securitised debt instrument” as any certificate or instrument, by whatever name called, of the nature referred to in sub-clause (ie) of clause (h) of section 2 of the Act issued by a special purpose distinct entity.

4.3 With a view to expanding the sustainable finance in Indian Securities Market, it is proposed to introduce the concept of “Sustainable Securitised Debt Instruments” for the purpose of providing originators of the underlying credit facilities which are within such international or domestic frameworks for sustainable finance, and thereby provide investors as well an opportunity to participate in the sustainable securitized debt instruments.

4.4 Accordingly, it is proposed to suitably amend the SDI Regulations so as to introduce the framework for “Sustainable Securitised Debt Instruments” i.e. instruments which have sustainable finance credit facilities as the underlying debt, and satisfies such international frameworks (as adapted or adjusted to suit Indian requirements) that are specified by SEBI from time to time.

4.5 Some of the international frameworks which could be considered are listed below:

- Green Bond Principles11 of ICMA, or

- Social Bond Principles12 of ICMA, or

- Sustainability Bond Guidelines13 of ICMA, or

- Sustainability-Linked Bond Principles14 of ICMA, or

- Climate Bond Standard of the Climate Bond Initiative

- Sustainability-Linked Loans Principles15 published by the Asia Pacific Loan, Market Association, Loan Market Association and Loan Syndications and Trading Association,

Certain regional groups have also published standards or taxonomies which could be considered by ISF, if are relevant to originators of the underlying credit facilities of Sustainable Securitised Debt Instruments or to investors in Sustainable Securitised Debt Instruments.

4.6 Initial and continuous disclosure requirements for Sustainable Securitised Debt Instruments shall be drawn basis the international frameworks identified, and with such adaptation or adjustments that are necessary. Initial disclosures could be in the offer document for the Sustainable Securitised Debt Instruments, while continuous disclosures could be in such form, manner and substance as may be specified. SEBI shall work with the Industry Standards Forum (ISF) for necessary recommendations and feedback in specifying such disclosure requirements.

| Consultation 2: Proposals for introduction of sustainable securitised debt instruments

Kindly provide your comments separately for each of the below items along with supporting rationale: 1) Whether the proposal to introduce a framework for sustainable securitised debt instruments is appropriate and adequate? 2) Are there any other frameworks/ guidelines in addition to frameworks listed at Para 4.5, that should be considered by ISF for providing recommendation on sustainable securitised debt instruments? |

5. Independent External Review

5.1 To facilitate transparency and augment the credibility of ESG Debt Securities and Sustainable Securitised Debt Instruments, the issuers of ESG Debt Securities would be required to appoint an independent external reviewer/ certifier. Similarly for sustainable securitized debt instruments, the originator of Sustainable Securitised Debt Instruments shall appoint an independent external reviewer/ certifier. The special purpose distinct entity and its trustees shall ensure that an independent external review is conducted or has been conducted by the originator in the form, manner and substance required by SEBI.

5.2 In line with international approaches, independent external review may take one or more of the following forms:

- Second Party Opinion

- Verification

- Certification

- Scoring / Rating

5.3 Independent external review for ESG Debt Securities and for Sustainable Securitised Debt Instruments will constitute an essential component of the trust but verify approach for reassurance of the investors and the market on the UoP and/or KPIs that such debt securities or instruments specify. SEBI may also consider whether ESG Rating Providers could undertake such independent external review, if there are no conflicts of interest.

| Consultation 3: Proposals for Independent External Review

Kindly provide your comments separately for each of the below items along with supporting rationale: 1. Whether the proposed requirement of independent external review for ESG Debt Securities and Sustainable Securitised Debt Instruments is appropriate and adequate? 2. Whether SEBI registered ESG Rating Providers could also be permitted to undertake such independent external review? |

6. Request for Public Comments

6.1 Considering the implications of the aforementioned matters on the market participants, public comments are invited on the above-detailed proposals. The comments/ suggestions should be submitted by any of the following modes latest by September 06, 2024 :-

6.2 Preferably through Online web-based form: The comments may be submitted through the following link:

https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?d oPublicComments=yes

6.3 The instructions to submit comments on the consultation paper are as under:

| 1. Before initiating the process, please read the instructions given on top left of the web form as “Instructions”.

2. Select the consultation paper you want to comment upon from the dropdown under the tab – “Consultation Paper” after entering the requisite information in the form. 3. All fields in the form are mandatory; 4. Email Id and phone number cannot be used more than once for providing comments on a particular consultation paper. 5. If you represent any organization other than the types mentioned under dropdown in “Organization Type”, please select “Others” and mention the type, which suits you best. Similarly, if you do not represent any organization, you may select “Others” and mention “Not Applicable” in the text box. 6. There will be a dropdown of Proposals in the form. Please select the proposals one- by-one and for each of the proposal, please record your level of agreement with the selected proposal. Please note that submission of agreement level is mandatory. 7. If you want to provide your comments for the selected proposal, please select “Yes” from the dropdown under “Do you want to comment on the proposal” and use the text boxes provided for the same. 8. After recording your response to the proposal, click on “Submit” button. System will save your response to the selected proposal and prompt you to record your response for the next proposal. Please follow this procedure for all the proposals given in the dropdown. 9. If you do not want to react on any proposal, please select that proposal from the dropdown and click on “Skip this proposal” and move to the next proposal. 10. After recording your response to all the proposals, you may see your draft response to all of proposals by clicking on “Check your response before submitting” just before submitting response to the last proposal in the dropdown. A pdf copy of the response can also be downloaded from the link given in right bottom of the web page. 11. The final comments shall be submitted only after recording your response on all of the proposals in the consultation paper |

6.4 In case of any technical issue in submitting your comment through web based public comments form, you may contact the following through email with a subject: “Issue in submitting comments on consultation paper on expanding the scope of sustainable finance framework in the indian securities market “.

- Rishi Barua, DGM (rishib@sebi.gov.in)

- Appin Gothwal, AGM (apping@sebi.gov.in)

- Priyanka Meena, AM (priyankameena@sebi.gov.in)

Issued on: August 16, 2024

Annex-I

Green Debt Securities definition

“Green debt security” means a debt security issued for raising funds subject to the conditions as may be specified by the Board from time to time, to be utilised for project(s) and/ or asset(s) falling under any of the following categories:

I. renewable and sustainable energy including wind, bioenergy, other sources of energy which use clean technology,

II. clean transportation including mass/public transportation,

III. climate change adaptation including efforts to make infrastructure more resilient to impacts of climate change and information support systems such as climate observation and early warning systems,

IV. energy efficiency including efficient and green buildings,

V. sustainable waste management including recycling, waste to energy, efficient disposal of wastage,

VI. sustainable land use including sustainable forestry and agriculture, afforestation,

VII. biodiversity conservation,

VIII. pollution prevention and control (including reduction of air emissions, greenhouse gas control, soil remediation, waste prevention, waste reduction, waste recycling and energy efficient or emission efficient waste to energy) and sectors mentioned under the India Cooling Action Plan launched by the Ministry of Environment, Forest and Climate Change,

IX. circular economy adapted products, production technologies and processes (such as the design and introduction of reusable, recyclable and refurbished materials, components and products, circular tools and services) and/or eco efficient products,

X. blue bonds which comprise of funds raised for sustainable water management including clean water and water recycling, and sustainable maritime sector including sustainable shipping, sustainable fishing, fully traceable sustainable seafood, ocean energy and ocean mapping,

XI. yellow bonds which comprise of funds raised for solar energy generation and the upstream industries and downstream industries associated with it,

XII. transition bonds which comprise of funds raised for transitioning to a more sustainable form of operations, in line with India’s Intended Nationally Determined Contributions, and

Explanation: Intended Nationally Determined Contributions (INDCs) refer to the climate targets determined by India under the Paris Agreement at the Conference of Parties 21 in 2015, and at the Conference of Parties 26 in 2021, as revised from time to time.

XIII. any other category, as may be specified by the Board from time to time

Notes:

1 https://sdgs.un.org/2030agenda

2 https://sdgs.un.org/goals

3 https://www.worldbank.org/en/topic/financialsector/brief/sustainable-finance

4 https://www.ceew.in/cef/quick-reads/explains/thematic-bonds#:~:text=Thematic%20bonds%20are%20fixed%2Dincome,and%20access%20to%20financial%20services.

5 https://www.icmagroup.org/assets/documents/Sustainable-finance/2022-updates/Green-Bond-Principles-June-2022-060623.pdf

6 https://www.icmagroup.org/assets/documents/Sustainable-finance/2023-updates/Social-Bond-Principles-SBP-June-2023-220623.pdf

7 https://www.icmagroup.org/assets/documents/Sustainable-finance/2021-updates/Sustainability-Bond-Guidelines-June-2021-140621.pdf

8 https://www.icmagroup.org/assets/documents/Sustainable-finance/2024-updates/Sustainability-Linked-Bond-Principles-June-2024.pdf

9 https://www.climatebonds.net/files/files/climate-bonds-standard-v4-1-202403.pdf

10 https://www.imf.org/external/pubs/ft/fandd/2008/09/pdf/basics.pdf

11 https://www.icmagroup.org/assets/documents/Sustainable-finance/2022-updates/Green-Bond-Principles-June-2022-060623.pdf

12 https://www.icmagroup.org/assets/documents/Sustainable-finance/2023-updates/Social-Bond-Principles-SBP-June-2023-220623.pdf

13 https://www.icmagroup.org/assets/documents/Sustainable-finance/2021-updates/Sustainability-Bond-Guidelines-June-2021-140621.pdf

14 https://www.icmagroup.org/assets/documents/Sustainable-finance/2024-updates/Sustainability-Linked-Bond-Principles-June-2024.pdf

15 https://www.lsta.org/content/sustainability-linked-loan-principles-sllp/