Securities and Exchange Board of India

1. As announced in the Union Budget 2012-13, the Finance Act 2012 has introduced a new section 80CCG on ‘Deduction in respect of investment made under an equity savings scheme‘ to give tax benefits to new investors who invest up to Rs. 50,000 and whose gross total annual income is less than or equal to Rs. 10 lakhs. The objective of the scheme is to encourage flow of savings in the financial instruments and improve the depth of the domestic capital market.

2. Vide notification 51/2012, dated November 23, 2012 (copy enclosed), the scheme has been notified by the Department of Revenue, Ministry of Finance (MoF). The notification is available on the website of Income Tax Department under section “Notifications”.

3. Stock exchanges, Depositories, Mutual Funds, Asset Management Companies (AMCs), Trustee Companies and Boards of Trustees of Mutual Funds are directed to take note of the notification and take necessary steps to implement the scheme. AMCs/Trustees shall ensure that RGESS eligible Exchange Traded Funds (ETFs) and Mutual Funds (MFs) schemes are in compliance with the aforementioned notification.

4. With regard to implementation of the MoF notification, the following is clarified:

(i) For RGESS eligible close-ended Mutual Funds schemes, advice given by AMCs to the depository for extinguishment of units of close-ended schemes upon maturity of the scheme shall be considered as settled through depository mechanism and therefore RGESS compliant.

(ii) AMCs shall disclose that the concerned RGESS eligible Exchange Traded Funds and Mutual Fund schemes is in compliance with the provisions of RGESS guidelines notified by Ministry of Finance vide notification no. 51/2012 F. No. 142/35/2012-TPL, dated November 23, 2012, in Scheme Information Document (SID), in case of new fund offer, or by way of addendum, in case of existing RGESS eligible Exchange Traded Funds and Mutual Fund schemes.

(iii) Section 6(c) of the notification states that the eligible securities brought into the demat account will automatically be subject to lock-in during the first year, unless the new investor specifies otherwise and for such specifications, the new retail investors shall submit a declaration in Form B indicating that such securities are not to be included within the above limit of investment. It is clarified that such declaration shall be submitted by an investor to its Depository Participant within a period of one month from the date of transaction.

(iv) For transactions undertaken by investors through their RGESS designated demat account, Depositories may seek necessary transactional details from stock exchanges viz. Actual Trade value, Trading date, Settlement number, etc., for the purpose of enforcing lock-in and for generating reports mandated vide MoF notification on RGESS. On receipt of such request from depositories, stock exchanges shall provide the details to depositories on an immediate basis. It shall also be ensured that a uniform file structure is used by stock exchanges and depositories for such intimation of transaction details.

(v) With regard to point 3(ix)(a) & (b) of RGESS notification, depositories may seek confirmation, as applicable, from stock exchanges.

(vi) With regard to the securities held in the RGESS designated account, treatment of the corporate actions shall be as given at Annexure A.

5. Stock exchanges shall furnish list of RGESS eligible stocks/ETFs/MF schemes on their website. Further, the list shall also be forwarded to the depositories at monthly intervals and whenever there is any change in the said list. For this purpose, Mutual Funds/AMCs shall communicate list of RGESS eligible MF schemes/ETFs to the stock exchanges.

6. Stock exchanges and the depositories are directed to:

(i) make necessary amendments, if any, to the relevant bye-laws, rules and regulations for the implementation of the scheme.

(ii) create wide publicity of the scheme among the investors and market participants, including through investor programs and displaying details on their website.

(iii) communicate to SEBI, the status of implementation of the provisions of this circular, as applicable.

7. Mutual Funds/AMCs are directed to create wide publicity of the scheme among the investors, including displaying details on their website

8. This circular is being issued in exercise of the powers conferred by Section 11 (1) of Securities and Exchange Board of India Act, 1992, Section 19 of the Depositories Act, 1996 and the Regulation 77 of SEBI (Mutual Funds) Regulations, 1996 to protect the interest of investors in securities and to promote the development of, and to regulate, the securities market.

Yours faithfully,

Maninder Cheema

Deputy General Manager

maninderc@sebi.gov.in

ANNEXURE A

TREATMENT OF CORPORATE ACTIONS

(i) Involuntary corporate actions: In case of corporate actions where investors has no choice in the matter, for example: demerger of companies, etc, the compliance status of RGESS demat account shall not change.

(ii) Voluntary corporate actions: In case of corporate actions where investors has the option to exercise his choice and thereby result in debit of securities, for example: buy-back, etc, the same shall be considered as a sale transaction for the purpose of the scheme.

Consolidated list of ‘corporate actions’

| Sr. No. | Corporate Action | Classification (Involuntary or Voluntary) |

| 1 | Amalgamation | Involuntary |

| 2 | Scheme of Arrangement | Involuntary |

| 3 | Reduction of Capital | Involuntary |

| 4 | Bonus issue | Involuntary |

| 5 | Buy Back of Shares | Voluntary (Involuntary in case of court intervention) |

| 6 | Stock Split | Involuntary |

| 7 | Consolidation of Shares | Involuntary |

| 8 | Conversion of Partly Paid up | Involuntary |

| 9 | Dividend [Final/Interim/Special] | Involuntary |

| 10 | Exchange of Share Certificate [Name change] | Involuntary |

| 11 | Rights Issue | Voluntary |

| 12 | Conversion (compulsory)* | Involuntary |

| 13 | Conversion (optionally)* | Involuntary |

| 14 | Redemption | Involuntary (voluntary, if there is option to continue with revised terms) |

| 15 | Dividend on Mutual Fund | Involuntary |

| 16 | Redemption of Mutual Fund | Involuntary on maturity (voluntary, if there is option to shift between different scheme(s) or on account of exit option due to change in fundamental attributes of scheme) |

*Considering any conversion into equities (e.g.: Conversion of warrants into equities)

ANNEXURE B- ILLUSTRATION OF LOCK-IN PERIOD IN RGESS

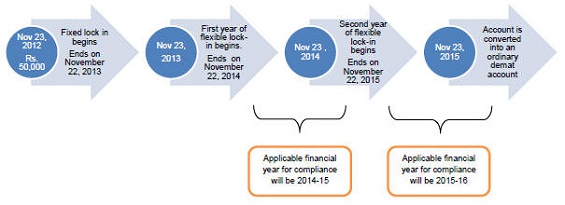

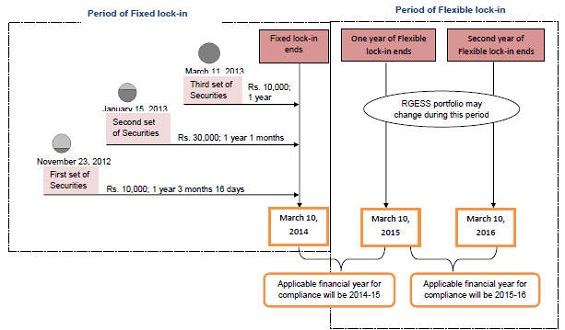

I. RGESS lock-in period if investments are brought in at once

ILLUSTRATION OF LOCK-IN PERIOD IN RGESS

II. RGESS lock-in period if investments are brought are in installment

MoF notification No. 51/2012 F.No.142/35/2012-TPL dated November 23, 2012

MoF notification No. 51/2012 F.No.142/35/2012-TPL dated November 23, 2012