Introduction

SEBI on 14th November, 2018 issued an informal guidance under SEBI (Substantial Acquisition of Shares and Takeover) Regulation, 2011 herein refer to as “SEBI (SAST), 2011”, which gives clarity regarding exemption provided under regulation 10 of SEBI (SAST), 2011 under Off-Market Transaction.

This article provides an analysis of the Informal Guidance given by SEBI.

Fact of the case

S.S Toshniwal (“Applicant”) one of the Shareholder and Promoter Group entity of Lactose (India) Limited (“Target Company”) had requested SEBI to issue an Informal Guidance Scheme with respect to its following queries were raised:

1. Effect of conversion of warrant into equity share capital of the Target Company, issued to the Applicant, by April 2019 will lead to increase in the shareholding pattern, from its existing 0.52% to 1.26%.

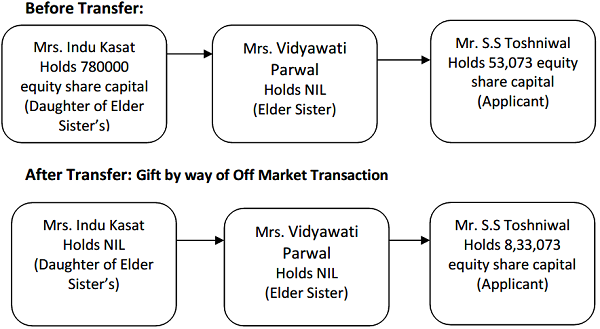

2. Applicant’s elder sister’s daughter, Mrs. Indu Kasat wants to gift equity shares by way of an off-market transaction to her mother, Mrs. Vidyawati Parwal constituting to 7.76% of the paid up equity share capital of the Target Company.

3. Vidyawati Parwal wish to gift the same as mentioned in point (2) to the Applicant by way of an off-market transaction.

S.S Toshniwal holds 53,073 equity shares of the Target company which constitutes 0.52% of equity share capital of the Target Company, in addition to the above it also holds 75000 convertible warrant, convertible into equity share capital of the Target company by April, 2019. After conversion its holding shall increase to 1,28,073 which constitutes 1.26% of equity share capital of the Target Company.

Her elder sister’s daughter Mrs. Indu Kasat holds 780000 equity share capital of the Target Company which constitutes to 7.76% of paid up equity share capital of the Target Company.

She wants to gift these shares by way of Off Market Transaction (Gift) to her mother (Mrs. Vidyawati Parwal).

Mrs. Vidyawati Parwal wants to gift theses shares to the Applicant by way of Off Market Transaction.

The off – market transaction would lead to change in total shareholding of the promoter group from current 34.28% to 42.04%. Further, warrant conversion promoter group shareholding shall be 43.51% of the paid up equity share capital of the Target company. There shall be no change in control and management of the Target Company even if shareholding of promoter group changes as above.

The above Applicant seeks for exemption as provided under regulation 10 of SEBI (SAST), 2011 and as the transaction is an off market transaction it will not attract regulation 4(1) of SEBI (Prohibition of Insider Trading) regulation 2015.

Further, the applicant states that since it is an off-market interse transfer among immediate relatives it will not trigger an open offer as per regulation 3(1) of SEBI (SAST), 2011 and offer price as per regulation 8 of SEBI (SAST), 2011.

Requirement under SEBI (Substantial Acquisition of Shares and Takeover), 2011

General Exemptions: Regulation 10

Sub-clause (i) clause (a) sub-regulation (1):

1. The following acquisitions shall be exempt from the obligation to make an open offer under regulation 3 and regulation 4 subject to fulfilment of the conditions stipulated therefor,—

a. acquisition pursuant to interse transfer of shares amongst qualifying persons,

being,—

(i) immediate relatives

Sub-regulation 5

In respect of acquisitions under clause (a) of sub-regulation (1), and clauses (e) and (f) of sub-regulation (4), the acquirer shall intimate the stock exchanges where the shares of the target company are listed, the details of the proposed acquisition in such form as may be specified, at least four working days prior to the proposed acquisition, and the stock exchange shall forthwith disseminate such information to the public.

Sub-regulation 6:

In respect of any acquisition made pursuant to exemption provided for in this regulation, the acquirer shall file a report with the stock exchanges where the shares of the target company are listed, in such form as may be specified not later than four working days from the acquisition, and the stock exchange shall forthwith disseminate such information to the public.

Sub-regulation 7:

In respect of any acquisition of or increase in voting rights pursuant to exemption provided for in clause (a) of sub-regulation (1), sub-clause (iii) of clause (d) of sub- regulation (1), clause (h) of sub-regulation (1), sub-regulation (2), sub-regulation (3) and clause (c) of sub-regulation (4), clauses (a), (b) and (f) of sub-regulation (4), the acquirer shall, within twenty-one working days of the date of acquisition, submit a report in such form as may be specified along with supporting documents to the Board giving all details inrespect of \acquisitions, along with a non-refundable fee of rupees one lakh fifty thousand by way of direct credit in the bank account through NEFT/RTGS/IMPS or any other mode allowed by RBI or by way of a banker’s cheque or demand draft payable in Mumbai in favour of the Board.

Disclosure of acquisition and disposal: Regulation 29

Sub-regulation 1:

Any acquirer who acquires shares or voting rights in a target company which taken together with shares or voting rights, if any, held by him and by persons acting in concert with him in such target company, aggregating to five per cent or more of the shares of such target company, shall disclose their aggregate shareholding and voting rights in such target company in such form as may be specified.

Sub-regulation 2:

Any person, who together with persons acting in concert with him, holds shares or voting rights entitling them to five per cent or more of the shares or voting rights in a target company, shall disclose the number of shares or voting rights held and change in shareholding or voting rights, even if such change results in shareholding falling below five per cent, if there has been change in such holdings from the last disclosure made under sub-regulation (1) or under this sub-regulation; and such change exceeds two per cent of total shareholding or voting rights in the target company, in such form as may be specified.

Immediate Relative: Regulation 2

Clause (l) sub-regulation 1:

Means any spouse of a person, and includes parent, brother, sister or child of such person or of the spouse.

Person Acting in Concert: Regulation 2

Clause (q) sub-regulation 1:

Persons who, with a common objective or purpose of acquisition of shares or voting rights in, or exercising control over a target company, pursuant to an agreement or understanding, formal or informal, directly or indirectly co-operate for acquisition of shares or voting rights in, or exercise of control over the target company.

Sub-regulation (2):

Without prejudice to the generality of the foregoing, the persons falling within the following categories shall be deemed to be persons acting in concert with other persons within the same category, unless the contrary is established,—

(i) a company, its holding company, subsidiary company and any company under the same management or control;

(ii) a company, its directors, and any person entrusted with the management of the company;

(iii) directors of companies referred to in item (i) and (ii) of this sub-clause and associates of such directors;

(iv) promoters and members of the promoter group;

(v) immediate relatives;

Offer Price: Regulation 8

Sub-regulation (1):

The open offer for acquiring shares under regulation 3, regulation 4, regulation 5 or regulation 6 shall be made at a price not lower than the price determined in accordance with sub-regulation (2) or sub-regulation (3), as the case may be.

SEBI’s informal guidance for the same

SEBI has replied to the query sought by the Applicant in two stage that are as follows:

From the definition of Immediate Relative, SEBI has interpreted following as immediate relative:

1. Parwal and Mrs. Indu Kasant

2. Parwal and Applicant

I. The first off-market transaction between Mrs. Parwal and Mrs. Indu kasat will lead to the following as shown in the table given below:

Heading |

Shareholding (Current) |

Increase/ Decrease in shares (off-market) |

Shareholding Post off-market Transaction |

Whether there is any trigger requiring open offer |

Whether exempt under General Exemption |

Whether disclosure requirement under Reg 29 as applicable |

Mrs. Indu Kasat |

780000 shares (7.77%) |

-78000 shares (7.77%) |

NIL |

– |

– |

– |

Mrs. Parwal |

NIL |

+780000 shares (7.77%) |

780000 shares (7.77%) |

Yes-Reg 3 (2) |

Reg 10 (10)(a)(i) |

Yes |

Promoters+ PAC’s |

34,41,425 shares (34.28%) |

+780000 shares (7.77%) |

42,21,425 shares (42.05%) |

Subject to the compliance with the condition mentioned under proviso to Regulation 10(1)(a) and Regulation (5), (6) and (7) of the Takeover Regulations, 2011:

Mrs. Parwal who is an immediate relative is also acting as Person acting in concert as defined above with the acquirer thus the total shareholding increase from 34.28% to 42.05% i.e more than 5% would trigger open offer requirement under Regulation 3 (2) of Takeover regulation 2011. However, since the transaction is between immediate relative the exemption under regulation 10 shall apply and therefore the transaction shall be exempt.

II. The Second off market transaction between Ms. Parwal and the Applicant

Heading |

Shareholding (Current) |

Increase/Decrease in shares (off-market) |

Shareholding Post off-market Transaction |

Whether there is any trigger requiring open offer |

Whether exempt under General Exemption |

Whether disclosure requirement under Reg 29 as applicable |

Mrs. Parwal |

780000 shares (7.77%) |

-780000 shares (7.77%) |

NIL |

– |

– |

– |

S.S Toshniwal |

53073 shares (0.53%) |

+780000 shares (7.77%) |

8,33,073 shares (8.30%) |

Yes-Reg 3 (2) |

Yes – Reg 10 (10)(a)(i) |

Yes |

Promoters+ PAC’s |

34,41,425 shares (34.28%) |

+780000 shares (7.77%) |

42,21,425 shares (42.05%) |

Subject to the compliance with the condition mentioned under proviso to Regulation 10(1)(a) and Regulation (5), (6) and (7) of the Takeover Regulations, 2011:

Mrs. Parwal who is an immediate relative is also acting as Person acting in concert as defined above with the acquirer thus the total shareholding increase from 34.28% to 42.05% i.e. more than 5% would trigger open offer requirement under Regulation 3 (2) of Takeover regulation 2011. But since the transaction is between immediate relative the exemption under regulation 10 shall apply and therefore the transaction shall be exempt.

Further, the off market transaction shall be exempt under Regulation 10(1)(a)(i) of the Takeover Regulation, 2011 from making an open offer and also under Regulation 8 of Takeover Regulation, 2011 would not apply.

With regard to conversion of warrant, it shall depend upon the shareholding pattern prevailing at the time of conversion.

Conclusion

Thus from the above it can be interpreted that the transaction between immediate relative in normal course or off – market transaction both are exempted under regulation 10 of SEBI (SAST), 2011 subject to the compliance of the respective condition prescribed under the regulation.

Further any allotment of warrant done whose conversion is to be done in future shall solely depends upon the nature, condition and existing shareholding pattern at the time of conversion.

The purpose of SEBI (Substantial Acquisition of Shares and Takeover) Regulation 2011 is to protect the interest of minority shareholder and to protect them from hostile takeover.

Author Bio