Objective

1. To solicit the comments/views from stakeholders including on issues related to trading in derivatives, participant’s profile, product mix, stock eligibility, leverage related matters and product suitability framework to further strengthen the framework in line with the emerging trends and global best practices.

Introduction

2. Derivatives market in India has been growing rapidly in recent years. Orderly growth, development and alignment of both cash and derivatives markets is important. Keeping this objective in mind, the discussion paper has been prepared to undertake an assessment of the derivatives market in India so as to evaluate whether there is a need to further strengthen the regulatory framework for derivatives in India.

Background

3. SEBI constituted a committee under the chairmanship of Dr. L. C. Gupta in November 1996 to “develop appropriate regulatory framework for derivatives trading in India”. In March 1998, the L. C. Gupta Committee (LCGC) submitted its report recommending the introduction of derivatives market in a phased manner beginning with the introduction of index futures.

4. In addition to the above, SEBI had also constituted Derivative Market Review Committee under the Chairmanship of Prof M Rammohan Rao to review development of the derivatives market and suggest future course of action. The committee interalia recommended to widen the range of products such as option contracts with longer life or tenure, creation of Volatility index & F&O contacts on it, options of futures, exchange traded currency contracts and mini contracts on equity indices. The committee had also made recommendations on operational issues such as revision of eligibility criteria for introduction of F&O on stocks & upward revision on position limits etc.

Relevant extracts of L C Gupta Committee

5. The Committee strongly favors the introduction of financial derivatives in order to provide the facility for hedging in the most cost-efficient way against market risk. This is an important economic purpose. At the same time, it recognizes that in order to make hedging possible, the market should also have speculators who are prepared to be counter-parties to hedgers. A derivatives market wholly or mostly consisting of speculators is unlikely to be a sound economic institution. A soundly based derivatives market requires the presence of both hedgers and speculators.

6. The Committee is of the opinion that the entry requirements for brokers/dealers for derivatives market have to be more stringent than for the cash market. These include not only capital adequacy requirements but also knowledge requirements in the form of mandatory passing of a certification programme by the brokers/dealers and the sales An important regulatory aspect of derivatives trading is the strict regulation of sales practices.

7. The objective of SEBI is to make both derivatives market and cash market fair, efficient and transparent. Economically, it is important to realize that equity cash market and equity derivatives market are of one piece. Their sound development is inter-related closely.

8. The Committee recognizes that an efficient cash market is required for an efficient futures market. The Committee also recognizes the danger that if the cash market behavior is erratic or does not reflect fundamentals, a futures market, based on such a cash market, will fail to give a correct indication of future prices and its usefulness for price discovery will be reduced.

9. With regard to participation of individual investors it is pertinent to mention here that L C Gupta committee in its report has given emphasis on Regulation of Sales Practices and Disclosures for Derivatives. The committee has observed following:

“The Committee has identified broker-client relationship and sales practices for derivatives as needing special regulatory focus. The potential risk involved in speculating (as opposed to hedging) with derivatives is not understood widely. In the case of pricing of complex derivatives contracts, there is a real danger of unethical sales practices. Clients may be fooled or induced to buy unsuitable derivatives contracts at unfair prices and without properly understanding the risks involved”.

Products available for trading in derivative segment

10. Accordingly BSE and NSE were permitted to introduce trading in derivatives on June 09, 2000 with launch of Equity Index futures followed by Index options. Subsequently, Futures & Options on Individual stocks were permitted in 2001. Currently, the following products are available for trading in the equity derivative segment of exchanges;

Table No 1

| Products | Settlement type |

| Index Futures | Cash Settled |

| Index Options | Cash Settled (European style) |

| Stock Futures | Cash/Physical Settled |

| Stock Options | Cash/Physical Settled (European style) |

11. Stock Exchanges were provided flexibility to offer cash settled or physically settled products and were allowed to offer either European style or American style stock options contracts. Exchanges (BSE & NSE) have introduced European style option contracts.

12. Presently, minimum contract size in equity derivatives segment is Rs. 5 lakhs. Therefore the lot size for derivatives contracts in equity derivatives segment is fixed in such a manner that the contract value of the derivative on the day of review is within 5 lakhs and Rs. 10 lakhs.

13. SEBI has prescribed eligibility criteria for introduction of derivatives on stocks and The eligibility criteria inter-alia includes the following:

a) A stock to be part of Top 500 stocks in terms of average daily market capitalization and average daily traded value in the previous six months on a rolling basis,

b) The stock’s median quarter-sigma order size over the last six months shall be not less than Rupees 10 Lakh and

c) The market wide position limit (MWPL) in the stock shall not be less than Rupees 300 crores etc.

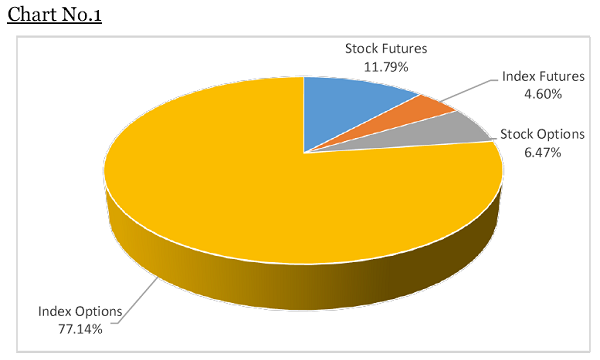

14. Below mentioned pie-chart depicts the share of turnover of various products available under the equity derivatives segment for FY 2016-17:

Chart No.1

Source NSE

Note: Significant trading in Nifty Futures takes place on SGX. Refer section 21.

15. For the FY 2016-17, it is seen that Equity derivatives turnover is largely dominated by index options which contributed 77.14% to the total turnover, followed by Stock Futures at 11.79%, Stock Options at 6.47% and Index Futures at 4.60%.

16. Index options and stock options dominate trading in the derivatives segment by accounting for 83.61% of total trading in derivative segment. The possible reasons for greater trading interest in the options could be that the Security Transaction tax (STT) on options is chargeable on option premium value & thus could be lower in term of value than that of futures where it is chargeable on notional value and also the trading in options enable market participant’s to deploy various trading strategies to earn upfront premium that may be used to off-set losses or enhance gains in their trading position in futures or in cash market.

Growth in Derivatives market in India

17. The following table shows the trend in volumes in equity cash segment and equity derivative segment at BSE and NSE:

Table No. 2

| Financial Year(FY) | Market Capitalisation of the Exchange (BSE) |

Turnover in Equity cash segment (Rs. Crores) |

Turnover in Equity Derivatives segment (Notional Values) (Rs. Crores) |

Ratio: Turnover in Equity derivatives / Equity cash |

| 2004-05 | 16,98,428 | 16,58,787 | 25,46,982 | 1.54 |

| 2005-06 | 30,22,191 | 23,85,641 | 48,24,174 | 2.02 |

| 2006-07 | 35,45,041 | 29,01,474 | 73,56,242 | 2.54 |

| 2007-08 | 51,38,015 | 51,29,893 | 1,30,90,478 | 2.55 |

| 2008-09 | 30,86,076 | 38,52,097 | 1,10,10,482 | 2.86 |

| 2009-10 | 61,65,620 | 55,16,833 | 1,76,63,665 | 3.20 |

| 2010-11 | 68,39,084 | 46,82,439 | 2,92,48,375 | 6.25 |

| 2011-12 | 62,14,9112 | 34,78,391 | 3,21,58,208 | 9.25 |

| 2012-13 | 63,87,887 | 32,57,053 | 3,86,96,523 | 11.88 |

| 2013-14 | 74,15,296 | 33,30,152 | 4,74,30,842 | 14.24 |

| 2014-15 | 1,01,49,290 | 51,84,500 | 7,59,69,194 | 14.65 |

| 2015-16 | 94,75,328 | 49,77,072 | 6,93,00,842 | 13.92 |

| 2016-17 | 1,21,54,525 | 60,54,174 | 9,43,77,241 | 15.59 |

| 2008-09 | 30,86,076 | 38,52,097 | 1,10,10,482 | 2.86 |

Cash market turnover and equity derivatives turnover include the total turnover at NSE & BSE.

18. It is observed from Table No. 2 above that between the period FY 2004-05 to FY 2016- 17, the compounded annual growth rate (CAGR) for turnover in cash market has been 11.39%, whereas CAGR for turnover in equity derivatives has been 35.10%. The market capitalization of listed companies (BSE) has grown has been 17.82% CAGR during this It is also observed that the ratio of turnover of equity derivatives to equity cash has increased from 1.54 to 15.59 during the aforesaid period.

19. The increase in the turnover over the years may be attributed to various reasons including the higher index levels and increase in stock prices resulting in growth of notional turnover, reduced STT on equity futures from 0.017% to 0.01% and introduction of commodity transaction tax at 0.01% on non-agricultural commodity futures in the Budget 2013 etc.

20. Over the years more than 95% of equity derivative trading in India happens on NSE. In this context, feedback has been received from market participants regarding derivative trading in mid-cap indices, exchange-wise position limits and to allow inter-operability of Clearing Corporations (CCs) to allow market participants to consolidate clearing with a CC of their choice to achieve economies of scale and efficiency gains.

21. Futures and options on Indian Indices (mainly NIFTY & SENSEX) are available for trading in other jurisdictions. Table No. 3 shows the name of the jurisdictions where derivative contracts on such Indices are available.

Table No.3

| Exchange | International Stock exchange on which Indian Index / indices are traded |

| NSE | Singapore Exchange Ltd. (SGX) |

| Osaka Exchange Inc. (OSE) | |

| Chicago Mercantile Exchange Inc. (CME) | |

| London Stock Exchange | |

| BSE | Hong Kong Exchange and Clearing Ltd |

| BM & BOVESPA SA, Brazil | |

| Johannesburg Stock Exchange, SA | |

| Public Joint Stocks Company MICEX RTS, Moscow | |

| The Korea Exchange Incorporated | |

| Dubai Gold & Commodities Exchange, Dubai |

Source: NSE & BSE

22. The SGX S&P CNX Nifty index future is one of the highly traded derivatives contract on the Nifty. The Singapore Stock Exchange started trading Nifty futures in September 2000, three months after they were launched on NSE. Month-wise turnover in NSE NIFTY Futures and Options and SGX NIFTY Futures and Options is given in Table No. 4 below:

Table No. 4 for the year 20 16-17

| Month | Nifty Futures | Nifty Options – Notional Turnover | ||||

| NSE Turnover (Rs Crores) |

SGX Turnover (Rs Crores) |

NSE Market Share (%) |

NSE Turnover (Rs Crores) |

SGX Turnover (RS Crores) |

NSE Market Share (%) |

|

| Apr-16 | 2,20,791 | 1,78,072 | 55.4% | 35,66,314 | 565 | 100.0% |

| May-16 | 2,75,662 | 2,04,118 | 57.5% | 42,35,370 | 1,851 | 100.0% |

| Jun-16 | 2,64,310 | 1,98,923 | 57.1% | 37,33,629 | 1,429 | 100.0% |

| Jul-16 | 2,04,709 | 1,77,874 | 53.5% | 30,20,394 | 743 | 100.0% |

| Aug-16 | 2,55,707 | 2,13,536 | 54.5% | 33,30,661 | 2,438 | 99.9% |

| Sep-16 | 2,30,831 | 2,21,035 | 51.1% | 31,92,692 | 3,736 | 99.9% |

| Oct-16 | 1,94,384 | 1,99,434 | 49.4% | 28,06,048 | 916 | 100.0% |

| Nov-16 | 2,71,903 | 2,21,925 | 55.1% | 37,57,529 | 584 | 100.0% |

| Dec-16 | 2,03,206 | 1,69,592 | 54.5% | 31,72,874 | 1,191 | 100.0% |

| Jan-17 | 1,87,600 | 1,68,122 | 52.7% | 26,66,564 | 1,109 | 100.0% |

| Feb-17 | 1,98,973 | 1,82,520 | 52.2% | 29,21,308 | 977 | 100.0% |

| Mar-17 | 2,17,219 | 2,18,506 | 49.9% | 28,82,720 | 1,867 | 99.9% |

| FY 16-17 | 27,25,293 | 23,53,655 | 53.7% | 3,92,86,102 | 17,407 | 100.0% |

For converting SGX volumes in to Rupee terms – SGX No of Contracts * 2 * Average Nifty Value for the month * Average USD-INR RBI reference rate for the month.

Participant’s profile:

23. Equity Derivatives market has a combination of participants from the Institutional investors, Stock brokers trading on own account (Proprietary trades), Corporates and other investors. Table No.5 shows the client category-wise turnover contribution in Equity Derivatives for the FY 16-17:

Table No 5:

| Broad Category | Equity Derivatives Turnover Contribution (%) | Client Category | Equity Derivatives Turnover Contribution (%) |

| Institutions | 14.15% | Foreign Portfolio Investors (FPIs) |

13.75% |

| Mutual Funds | 0.40% | ||

| Domestic Financial Institutions (DFIs) |

0.00% | ||

| Banks | 0.00% | ||

| Insurance Companies | 0.00% | ||

| Proprietary Trades | 42.07% | Proprietary Trades | 42.07% |

| Non Institutional Non Proprietary |

43.78% | Individual Investors | 25.67% |

| Corporates | 8.25% | ||

| Partnership firms | 8.22% | ||

| HUFs | 1.41% | ||

| Others | 0.19% | ||

| NRIs | 0.05% |

Source: NSE

Product wise profiling of investors:

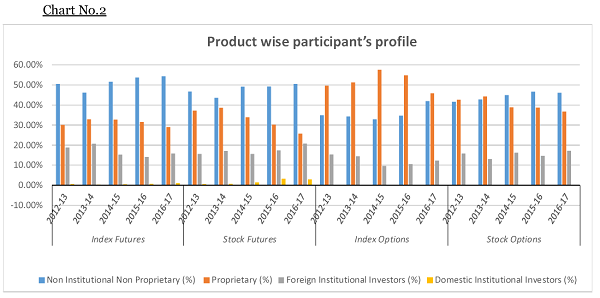

24. The data regarding participants of the market are further sliced to analyse their product-wise participation. The following graph displays product wise segregation of participants in the derivative market.

Chart No.2

Source NSE

25. The analysis of profile of the participants in the equity derivative segment reveal the following;

- The proprietary trades i.e., trading by stock brokers on their proprietary account dominate trading in Index options. The proprietary trades contribute between 45% -55% of total trading volume in index options. Non Institutional Non Proprietary category which includes individual investors and proprietary category together contributed around 85% of the total trading volume in index options.

- In case of stock options, both proprietary trades and non-institutional non-proprietary contributed for around 80% of trading stock options.

- One possible reason for the active trading by proprietary trades in derivatives especially options could be upfront income in the form of option premium on writing of options.

- It is observed that non-institutional non-proprietary investors which include individual investors contribute the highest volume in futures (index as well as stock). (It is observed from Table No 5 and Chart No 2 that Individual investors accounts for 58% of trading by non-institutional non-proprietary category.) The possible reasons for such trading preference could be that futures are less complex than options and also Individual investors familiarity with trading in index futures and stock futures.

- It is observed that Foreign Investors contribute between 15%-20% in the total volume across all product categories available in equity derivatives segment. The FPIs are present in all types of product categories to hedge their underlying exposure and they may not be taking speculative positions.

- Further, low FPIs participation could also be because of trading of futures and options on major indices in foreign markets such as Singapore, Hong Kong and Dubai etc.

- Domestic institutional investors are not active in derivatives and their turnover is negligible in the derivative segment. The lower trading interest by the domestic institutions such as mutual funds could be attributed to certain regulatory restrictions viz not allowed to write option contracts and exposure to option premium paid must not exceed 20% of the net assets of the scheme etc.

26. It is observed from Table No. 5 and Chart No 2 that Individual Investors contributed for 25.67% of total turnover and these investors constitute 58% in the category of non-institution non-proprietary trading which dominates trades in index futures and stock Therefore it could be inferred that individual investors are present across all types of derivative products and their trading may be concentrated in index futures, stock future and stock options.

27. As evaluated from the data, individual investors are present across all product categories including products such as index option/stock options which are inherently more complex and are thus more risky, particularly selling of options.

28. The participation of individual investors and their contribution in the derivative segment has been shown in the Table No 6 below:

Table No. 6

| Calendar Year |

No of Individual Investors (in Lakhs) |

Contribution of Individuals in equity derivative as a % of total turnover in equity derivative segment |

| 2010 | 10.60 | 33.88 |

| 2011 | 9.22 | 30.33 |

| 2012 | 7.61 | 29.32 |

| 2013 | 6.84 | 26.32 |

| 2014 | 6.87 | 26.83 |

| 2015 | 7.28 | 26.99 |

| 2016 | 7.26 | 28.50 |

| 2017* | 5.70 | 29.71 |

*Till May 2017 (Source:NSE)

29. It is seen from the Table No 6 above that the contribution of individual investors to the total turnover in the equity derivative segment remained in the range of 26% to 33%. However, taking into account the increase in turnover in the equity derivative segment and the number of investors trading in equity derivative segment it can be inferred that trading turnover in the equity derivative segment per investor has increased.

30. In order to ascertain trading behavior of such investors, the trading activity of these investors in the cash segment has been taken as a proxy. The profiling is done on the basis of trading activity of individual investors in cash segment. The Table No 7 below display categorization by cash market trading of above individual investors during 2016-17:

Table No. 7: Individual investors:-Comparative trading pattern of Cash and derivative segment

| Cash Market turnover of Individual Investors

(A) |

Percentage of Individual Investors to total Individual Investors traded in Derivatives.

(B) |

Percentage of turnover to total turnover by Individual Investors in Derivative Segment.(C) |

Percentage of turnover by individual investor in derivative to total investors in derivatives.( D)= (C)*25.67 ($) |

| Above Rs. 1 Crore | 22.80 | 55.90 | 14.34 |

| Between Rs. 50 Lakhs and Rs. 1 Crore | 8.50 | 7.30 | 1.87 |

| Between Rs. 10 Lakhs and Rs. 50 Lakhs | 20.40 | 13.50 | 3.48 |

| Between Rs. 2 Lakh and Rs. 10 Lakhs | 16.50 | 7.50 | 1.92 |

| Below Rs. 2 lakhs | 17.40 | 5.90 | 1.51 |

| Not traded | 14.40 | 9.90 | 2.54 |

Source: NSE

($)Contribution of Turnover by Individual investors in the Equity Derivative Segment.

31. It is observed from Table No 7 that;

- Investors with trades of less than equal to Rs.10 lakhs accounts for about 6% of the total derivative trading by individual investor, of these investors not traded in cash market accounts for 2.5% of total derivative trading by individual investor.

- Approximately 68% of total Individual Investors traded in the derivative segment are falling in the category of trades greater than Rs.2 lakhs in cash segment. These Individual Investors account for more than 84% of turnover in Derivative Segment in the Individual Investor category.

- Number of Individual Investors traded in the derivative segment are scattered in terms of their turnover in cash segment.

- Individual investors traded for value greater than Rs.10 lakhs in cash segment have around 77% of concentration in turnover in derivative segment (in the category of Individual Investors).

- Approximately 23% of individual investors who have traded in the equity derivatives have a cash market turnover of less than Rs.10 lakhs.

- Around 14% of Individual Investors who have contributed approximately 10% of the turnover of equity derivatives segment have not traded in the cash segment. Such trading could be speculative in nature.

- More than 50% trading in the derivative segment in the category of Individual Investors is concentrated by investors who have greater than Rs.1 crore exposure in cash market.

32. Derivatives products by nature are complex instruments. The valuation of derivatives such as options depends on many variables and option writers are exposed to significant risk if that do not have corresponding position. Therefore it is important that investors have a good understanding of derivatives and the ability to absorb the risk of their position. Indian market does not have the concept of product suitability framework. Investors may not have adequate understanding and financial capability to withstand risk posed by complex derivative instruments. It may be pertinent to mention that L C Gupta committee in its report has also given emphasis on Regulation of Sales Practices and Disclosures for Derivatives.

Comparison of Turnover ratios across foreign markets vis-a vis India market

Table No.8

| Years | Ratio: Turnover in Equity derivatives / Equity cash (Based on Premium Value) | Ratio: Turnover in Equity derivatives / Equity cash (Based on Notional Value) |

| 2012-13 | 2.33 | 11.88 |

| 2013-14 | 2.19 | 14.24 |

| 2014-15 | 2.54 | 14.65 |

| 2015-16 | 2.47 | 13.92 |

| 2016-17 | 2.58 | 15.59 |

Source: BSE & NSE

33. It may be observed that the ratio of notional turnover in equity derivatives to equity cash segment was 1.54 for the FY 2004-05. The same ratio increased to 15.59 for the FY 2016-17. The ratio of turnover in equity derivatives segment after taking into account the premiums paid for option contracts to turnover in cash segment for the period from FY 2012-13 to FY 2016-17 are given below in Table No.10.

34. The ratio of turnover in equity derivatives to turnover in equity cash market across various countries are given below;

Table No. 9

| Jurisdiction | Ratio: F&O/Cash (Notional) |

| Australian Securities Exchange | 2.32 |

| Hong Kong Exchanges and Clearing | 7.23 |

| Japan Exchange Group Inc. | 1.90 |

| Korea Exchange | 24.05 |

| BME Spanish Exchanges | 1.13 |

| Euronext | 1.87 |

| Moscow Exchange | 3.92 |

| India | 15.59 |

Source: World Federation of Exchanges (WFE) Monthly Statistics- Calendar Year 2016

Note: US market statistics are not readily due to large shares of Electronic Communication Network (ECN), Dark pools etc.

35. The ratio of turnover in equity derivatives segment after taking into account only the premiums paid for option contracts to turnover in equity cash segment for the Calendar year 2015 are given below;

Table No. 10

| Jurisdiction | Ratio: F&O/Cash (premium) |

|

| South Korea | 2.23 | |

| China (*) | 1.55* | |

| India | 2.53 |

Source WFE IOMA 2015 survey (premium data is available only in case of few jurisdictions who has reported the data for the year 2015. (*) In China only stock index futures are available

36. It is observed from the above Table No.9 that the ratio of turnover in equity derivatives to turnover in equity cash market in India is high and second only to South Korea. Comparative turnover on the basis of option premium in other foreign markets as stated in the Table No.10 above indicate that the turnover ratio in India is also somewhat higher than that of foreign markets.

Factors governing trading behaviour in derivatives

I. Margin required for trading in Derivatives

37. Margin for equity derivatives is computed on a portfolio based approach using a software called – SPAN (Standard Portfolio Analysis of Risk). SPAN uses different types of scenarios to calculate margins. The minimum margin percentage on index futures is 5% and on the stock futures is 7.5% which are scaled up by look ahead period.

38. In case clients have off-setting positions such as Index futures/stock futures and constituent stock/stock futures, then cross margin benefit is provided wherein margin requirement is reduced due to off-setting nature of the positions. Further, margins are levied at the exchange/clearing corporation level. No adjustment in margins is permitted for taking off-setting positions in two different exchanges.

39. In cash segment, no adjustment in margins is allowed on off-setting positions.

II. Securities Transaction Tax (STT) framework in India

40. Securities Transaction Tax (STT) is levied on the transactions done in the equity derivatives segment of the stock exchanges. STT came into effect from October 1, 2004. Table No. 11 below shows the changes in STT rates applicable to transactions in cash segment and equity derivatives segment since its introduction.

Table No. 11: STT Rates

| Date | Cash Deliverable (Buy and Sell) |

Cash Non Deliverable (Sell) | Equity Futures (Sell) | Options Notional Amount (Sell) | Option Premiu m (Sell) | Exercised Options on Notional (buyer) |

| 1-Oct-04 | 0.075 | 0.015 | 0.01 | 0.017 | – | 0.01 |

| 1-Jun-05 | 0.10 | 0.020 | 0.0133 | 0.017 | – | 0.0133 |

| 1-Jun-06 | 0.125 | 0.025 | 0.017 | 0.017 | – | 0.017 |

| 1-Jun-08 | 0.125 | 0.025 | 0.017 | – | 0.017 | 0.125 |

| 1-Jun-13 | 0.10 | 0.025 | 0.01 | – | 0.017 | 0.125 |

| 1-Jun-16 | 0.10 | 0.025 | 0.01 | – | 0.05 | 0.125 |

Source: NSE

41. From the above Table, the following observations are made:

- In Cash segment, the STT rate is higher for delivery based transactions than non-delivery transactions;

- STT in Options was levied on the seller of options on the notional value of the contract (strike price plus premium). However, with effect from June 1, 2008, STT is being levied only on the premium amount.

- STT is levied at 0.05% on the option premium on the seller of the option whereas on exercise of the option, STT is levied at 0.125% on the notional value of the option on the buyer of the option.

Observations:

42. From the data that have been placed in the preceding Tables, the following is observed:

- Between the period from FY 2004-05 to 2016-17, the growth in the turnover of equity derivatives segment outpaced the growth in turnover of cash segment. The ratio of notional turnover in equity derivatives to equity cash segment increased from 1.54 for the FY 2004-05 to 15.59 for the FY 2016-17. However, in case the option turnover is based on premium value, the ratio of cash to derivatives is somewhat in line with international trend.

- There is significant concentration of volumes in terms of products, exchange and investor category.

- In terms of indices NIFTY futures is highly traded and volumes are almost divided between domestic and SGX Nifty futures indicating overseas interest in the NIFTY futures.

- Options dominate trading in the derivatives segment by accounting for 83.61% of total trading in derivative segment.

- Proprietary trades and Individual investors contribute 43% and 26% respectively of the total volume of the equity derivatives in India.

- Around 14% of Individual Investors who have contributed approximately 2.5% of the total turnover of equity derivatives segment have not traded in the cash More than 50% trading in the derivative segment in the category of Individual Investors is contributed by investors who have greater than Rs.1 Crore exposure in cash market;

- Large number of individual investors are active in derivative segment. Going by their trading pattern in cash segment, it is observed that these investors may or may not have adequate financial capability to withstand risks posed by complex derivative instruments. In the absence of a product suitability framework, this may not be in the interest of securities market.

SEBI Initiatives

43. SEBI has taken steps to develop the cash market by initiating measures such as introduction of new products, redesigning existing products, conducting investor awareness initiative, etc. SEBI has revised the Margin Trading facility by rationalising initial margin requirements in cash market, permitting stocks as collateral for availing funding from stock brokers, etc.

44. Similarly to enhance the liquidity in the in the Securities Lending and Borrowing (SLB) mechanism the framework has been revised to make it more suited to the needs of the market participants. SEBI has received many suggestions to further improve the SLB SEBI is examining the suggestions with view to improve the SLB mechanism.

Feasibility of Product Suitability for trading in derivatives

45. Though the observations of L C Gupta Committee regarding Regulation of Sales Practices and Disclosures for Derivatives in India were made at the time of the introduction of derivative trading in India, are still relevant. SEBI Investor Survey 2015 brought out the risk perceptions of investors with regard to the various financial In the said report, it is observed that 31% of investor’s responded consider bonds/debenture more risky that equity and mutual funds. Further, 57% respondents believe that bonds/debentures are unsafe. Thus there is need to have focused investor awareness with regard to financial instruments particularly derivative products.

46. Derivatives are complex products and there are many variables which are required to be considered for valuation of the derivative contracts. Under the current framework, the trading members are required to have qualified approved user and sales person who have passed a Certification programme approved by SEBI to operate in derivative market. However, a concept of product suitability framework for clients as prevalent in other jurisdictions is not present in India.

Matters for discussion

i. Ratio of turnover in derivatives to turnover in cash market is around 15 times. To what extent the drivers of this ratio in India are comparable with drivers in other

ii. What are the global best practices and experience in international markets to align cash and derivative markets.

iii. Considering the participants’ profile, what measures would be required to create balanced participation in equity derivatives market.

iv. Taking into account trading of individual investors in derivatives, especially options, is there a need to introduce a product suitability framework in our

v. Considering participants’ profile, product mix and leverage in equity derivatives, what could be the guiding principles for setting minimum contract size and open position limits for equity derivatives.

vi. Whether there is a need to review existing criteria for introduction of derivatives on stocks or derivatives on indices.

vii. Taking in to account the margin levied in the derivative segment and consequent leverage, is the present margin framework adequate. Is there a need to review trading and risk management framework for derivatives.

viii. Whether there are any inefficiencies in the market that needs to be addressed. Whether there is any regulatory arbitrage that needs to be addressed.

ix. Whether there is any regulatory arbitrage that needs to be addressed.

47. Comments/ suggestions may be provided in the format given below:-

| Name of entity / person / intermediary/ Organization | |||

| Sr. No. | Issues | Suggestions | Rationale |

Comments may please be emailed on or before August 10, 2017 to vishalp@sebi.gov.in or sent by post, to:-

Vishal M Padole

Assistant General Manager

Division of Policy, Market Regulation Department

Securities and Exchange Board of India SEBI Bhavan, Plot No. C4-A, “G” Block, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051