1. Background

1.1 Sustainable Finance is the process of taking due account of environmental, social and governance (ESG) considerations while making investment decisions in the financial sector, leading to increased longer-term investments into sustainable economic activities and projects.1

1.2 The need for sustainable finance was felt in the aftermath of repeated environmental disasters and extreme weather events, corporate finance being driven purely by profit motives and corporate governance norms being followed as the exception rather than the norm. This has been bolstered by the demand for sustainable avenues of investments from a section of the new- age investors as well as with the substantial rise in the prominence of the Stakeholder’s theory over Shareholder’s theory.

1.3 The COP 26 mandate: In the 2021 United Nations Climate Change Conference, more commonly referred to as COP26, held in Glasgow, Scotland, 197 Countries, including India, have made enhanced commitments towards mitigating climate change and promising more climate finance for developing countries to adapt to climate impacts. This means that sustainable finance will be the mainstay of world business, which in turn, will mean more demand for funds in this domain.

2. SEBI’s regulatory regime on Green bonds:

2.1 The concept of ‘green debt securities’ was introduced under the erstwhile Securities and Exchange Board of India (Issue and Listing of Debt Securities) Regulations, 2008 vide circular dated May 30, 20172.

2.2 Regulation 2(1)(q) of the Securities and Exchange Board of India (Issue and Listing of Non-Convertible Securities) Regulations (NCS Regulations) defines ‘green debt security’, which reads as under:

“Green debt security” means a debt security issued for raising funds that are to be utilised for project(s) and/or asset(s) falling under any of the following categories, subject to the conditions as may be specified by the Board from time to time:

(i) Renewable and sustainable energy including wind, solar, bioenergy, other sources of energy which use clean technology,

(ii) Clean transportation including mass/public transportation,

(iii) Sustainable water management including clean and/or drinking water, water recycling,

(iv) Climate change adaptation,

(v) Energy efficiency including efficient and green buildings,

(vi) Sustainable waste management including recycling, waste to energy, efficient disposal of wastage,

(vii) Sustainable land use including sustainable forestry and agriculture, afforestation,

(viii) Biodiversity conservation, or

(ix) a category as may be specified by the Board, from time to time

2.3 Further, Chapter IX of the Operational Circular on the NCS Regulations, 2021 dated August 10, 2021, as amended on date, specifies the following with reference to issuers of green debt securities:

a. Additional disclosure requirements in the offer document;

b. Continuous disclosure requirements in annual report and financial results;

c. Responsibilities of the issuer.

3. Mandate of this consultation paper

3.1. Since the framework of green debt securities was laid down by SEBI, there have been multiple events in the sustainable finance space around the world, thereby necessitating a review in the Indian context.

3.2. In this context, SEBI, through this consultation paper, is seeking public comments on a proposed regulatory framework:

a. to amplify the definition of green debt securities,

b. to introduce the concept of blue bonds

c. to reduce the compliance cost for issuers of green debt securities with while not creating any perverse incentives that may lead to ‘greenwashing’.

3.3. Suggestions are also solicited towards increasing avenues for sustainable finance in India, while considering India’s unique goals of pursuing high growth with sustainable development.

3.4. This consultation paper follows a series of discussions held with multiple stakeholders, including the sub-committee formed under the Corporate Bonds Securitization Advisory Committee (CoBoSAC) of SEBI.

4. Global scenario

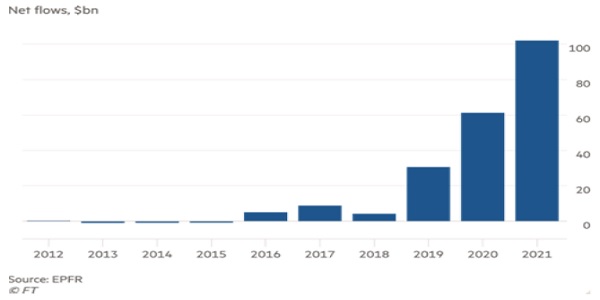

4.1 Issuance of green, social, sustainable and sustainability-linked (GSSS) bonds as a percentage of total global bond issuance rose from roughly 2 per cent at the start of 2018 to a peak of over 12 per cent at the end of 20213. Prices continued to rise as the demand from investors exploded. Figures from data provider EPFR, as given in the graph below, show that flows into ESG and socially responsible investing bond funds rose from a net of $4.2bn in 2018 to $102bn in 2021.

4.2 With economic growth slowing globally — owing to high inflation, high commodity prices and higher interest rates — issuers of bonds, both green and conventional, have pulled back. As the sustainable bonds are subject to the same headwinds as that of the broader market, green bond issuances in this year are expected to be roughly in line with 2021. That is a notable slowdown, given how quickly the market has been growing. Despite the above fact, rating agencies forecast that global issuance of GSSS bonds will be around $1tn this year4.

5. Present Fund raising through Green Bonds – India

5.1. As per the Economic Survey 2019-205, climate bonds worth USD 10.3 billion were issued in the first half of 2019 in India. Climate Bonds in India are focused on green bonds, which are specifically linked to climate-change mitigation, adaptation and resilience.

5.2. A number of Government agencies have contributed to issuance of such bonds, particularly Indian Renewable Energy Development Agency (IREDA) and the Indian Railway Finance Corporation (IRFC).

5.3. Currently, green bonds raised by various issuers are listed on India INX. Similarly, various issuers have also issued and listed their bonds on other international stock exchanges such as Luxembourg SE, Singapore Exchange, etc.

5.4. Indian companies raised nearly USD 7 billion through ESG and Green bonds in 2021, compared to USD 1.4 billion and USD 4 billion in 2020 and 2019, respectively.

5.5. As of February 12, 2020, the outstanding amount of green bonds in India was US$16.3 billion.

5.6. As per Economic Survey 2020-21 and Emerging Markets Green Bonds Report 2020, India occupies the 2nd spot (after China) in the cumulative emerging market Green Bond Issuance, 2012-20206.

Cumulative Emerging Market Green Bond Issuance, 2012-2020 (US$ million)

5.7. The above graph shows that in most countries, green bond issuances by corporate entities vastly exceed the issuances by government/ sovereign agencies. The only exceptions are Chile, Poland, Indonesia, Hungary, Egypt and Argentina.

5.8. As on June 30, 2022, under the SEBI framework for green bonds, 14 issuers have raised Rs. 4,539 crore (about $ 0.5 billion).

5.9. As can be seen from above, there is a stark divergence between the amount raised by listing green bonds in Indian jurisdictions versus foreign jurisdictions or autonomous jurisdictions like INX (India International Exchange). It may be noted that issuers are finding it more attractive to list on bourses falling outside SEBI Framework.

5.10. Most of the green bonds issued by Indian issuers are listed on offshore exchanges. Informal consultation with the industry participants attribute this to:

– Lack of demand for such bonds among the Indian investors

– Favourable pricing in overseas market.

6. Scope for sustainable finance in India

6.1 At the COP-26 summit in Glasgow, India had made the following commitments towards its climate change goals7:

a. Raising non-fossil fuel based energy capacity to 500 GW.

b. Lowering total projected carbon emission by one billion tons.

c. Meeting 50% of the country’s energy needs through renewable sources.

d. Reduce the carbon intensity of the economy to sub 45% level.

e. Commitment to achieve net-zero emissions by 2070.

6.2 Government of India has initiated the following schemes/ policies in pursuit of the goals towards COP-26 targets:

a. Commission on Air Quality Management (CAQM) – phasing out of coal use in National Capital Region from January 2023, but exempting thermal power plants using low-sulphur coal.

b. National Biomass Co-firing policy to use biomass like paddy stubble and cow-dung in coal power plants8.

c. Mandate the use of flue gas desulphurization (FGD) techniques in both existing and upcoming thermal power plants.

d. Government has targeted to achieve 100 Million Tonnes of Coal Gasification by 20309.

e. National Mission on Transformative Mobility and Battery Storage10.

f. Productivity Linked Incentives (PLI) Scheme on Advanced Cell Chemistry and Battery Storage11.

g. India Cooling Action Plan12.

6.3 Views/ comments sought on:

a. Whether the above mentioned initiatives offer any scope for financing through green bonds?

b. Please offer comments on whether there are any additional policies/ schemes in line with the above objective, if any?

7. Potential in emerging areas

7.1. The sub-committee constituted by the CoBoSAC had presented its report, which has covered areas like priority sector lending to green sectors, investment by institutional investors, tax recommendation for green bonds and updation of extant guidelines in line with updated Green Bond Principles published by the International Capital Markets Association13.

7.2. There is a need to further channel the investment in emerging areas like Data Centers which are receiving policy traction (Draft Data Center Policy). This field assumes importance in light of government push for data localization and the storage necessities for large volumes of data collected in India. Data Centers need tremendous cooling facilities, some of which can be attractive avenues for sustainable finance.

7.3. New concepts like circular economy and regional resource based manufacturing are gaining currency, as a mode to balance job creation with inter-generational environmental equity. Though definitions of these need deeper analysis, there is a need for encouraging flow of green finance in these initiatives. The Government of India has presented schemes like One District One Product, Zero Effect Zero Defect and promotion of these goods through local post offices and railway stations.

7.4. Ecosystem services evaluation- The Natural Capital Accounting and Valuation of Ecosystem Services (NCAVES) India Forum is being organized by Ministry of Statistics and Programme Implementation (MoSPI) in collaboration with the United Nations Statistics Division (UNSD), European Union and UN Environment. India has also implemented the System of Environmental Economic Accounting (SEEA) which provides policy makers and decision-makers with information that accounts for the value nature contributes to our economies.14

7.5. Agritech companies investing in net-zero for agriculture: – Agriculture and allied sectors like animal husbandry are responsible for over 85% of anthropogenic greenhouse gas emissions. Sustainable finance and technology in this sector can take out a major source of climate change.

7.6. National Hydrogen Mission- India is targeting to produce three-fourths of its hydrogen from renewable resources by 2050.15

7.7. Blue economy and ocean conservation.16

8. Potential for blue bonds

8.1. According to the World Bank, the blue economy is the “sustainable use of ocean resources for economic growth, improved livelihoods, and jobs while preserving the health of ocean ecosystem.”17 European Commission defines it as “All economic activities related to oceans, seas and coasts.

8.2. For a country like India that has a 7500 km long coastline and 14,500 km of navigable inland waterways, the development of Blue Economy can serve as a growth catalyst in realizing the vision to become a $10 trillion economy by 2032. The Blue economy currently comprises 4.1% of India’s economy.

8.3. The Government of India has kickstarted the initiative to develop the blue economy by announcing project Sagarmala, a first of its kind port-led development programme in India. The Sagarmala Programme plans to bring in development around India’s coastal regions based on the following four pillars: Port Modernization & New Port Development, Port Connectivity Enhancement & Port-linked Industrialization.

8.4. The Ministry of Earth Sciences (MoES) has rolled out the draft Blue Economy policy, inviting suggestions and inputs from various stakeholders.

8.5. It emphasizes policies across several key sectors to achieve holistic growth of India’s economy. It recognizes the following thematic areas:

a. National accounting framework for the blue economy and ocean governance.

b. Coastal marine spatial planning and tourism.

c. Marine fisheries, aquaculture, and fish processing.

d. Manufacturing, emerging industries, trade, technology, services, and skill development.

e. Logistics, infrastructure and shipping, including trans-shipments.

f. Coastal and deep-sea mining and offshore energy.

g. Security, strategic dimensions, and international engagement.

h. India’s Exclusive Economic Zone of over 2 million square kilometres has a huge living and non-living resources with significant recoverable resources such as crude oil and natural gas.

9. Scope of blue bonds in India

India has tremendous scope for deployment of blue bonds in various aspects of the blue economy, like:

9.1 Oceanic resource mining: Polymetallic nodules and methane hydrates are abundant in the Indian Ocean Region. Mining of polymetallic nodules present in the seabed in the Central Indian Ocean Basin can help India improve availability of nickel, copper, cobalt and manganese. Through an agreement with the International Seabed Authority, India has a right to explore and mine polymetallic nodules over 750,000 square km.18

9.2 Sustainable fishing: As the developing countries face new challenges at WTO to phase out Illegal, Unreported and Unregulated (IUU) fishing, it is time the country phases out exploitative fishing devices like bottom trawlers. India has an exclusive economic zone of 2.37 million sq. km.

9.3 National Offshore Wind Energy Policy: Ministry has set a target of 5.0 GW of offshore wind installations by 2022 and 30 GW by 2030 which has been issued to give confidence to the project developers in Indian market.

9.4 Coral degradation: India can invest in technologies like biorock to rejuvenate the corals along its coastline, by forming an artificial substrate.

9.5 India has acceded to the Marine Pollution (MARPOL) convention covering prevention of pollution of the marine environment by ships from operational or accidental causes.

9.6 Geoengineering techniques like ocean fertilization or ocean nourishment is a type of climate engineering based on the purposeful introduction of plant nutrients to the upper ocean to increase marine food production and to remove carbon dioxide from the atmosphere.

9.7 Blue flag beach is an eco-tourism model endeavouring to provide the tourists/ beachgoers clean and hygienic bathing water, facilities, a safe and healthy environment and sustainable development of the area.19

9.8 Views/ comments sought on:

a. Whether the above mentioned initiatives offer any scope for financing through blue bonds?

b. Whether introducing coloured bonds (blue bonds for blue economy, yellow bonds for solar power) will help increase channels for funding to green projects?

c. Please offer comments on whether any additional policies/ schemes, if any?

10. Recommendations made by the sub-committee of CoBoSAC on green bonds

The sub-committee has proposed the following amendments to SEBI guidelines in order to align with the updated Green Bond Principles (GBP) published by the International Capital Market Association (ICMA):

| Sr. No. | Existing clause | Need for change | Proposed amendment |

| a. | Definition of green debt security (GDS) Regulation 2(1)(q) of SEBI (Issue and Listing of Non-Convertible Securities), Regulations, 2021) | The extant SEBI framework defines GDS as debt security issued for raising funds that are to be utilised for projects or assets falling under certain categories.

GBP 2021 have included two additional categories, namely, pollution prevention and control and circular economy adapted products, as eligible green projects. In order to align with GBP 2021 principles, these additional categories may be included. |

The following may be included in addition to the existing list of eligible categories for issuance of GDS:

a. Pollution prevention and control (including reduction of air emissions, greenhouse gas control, soil remediation, waste prevention/minimization, waste reduction, waste recycling and energy/ emission efficient waste to energy). b. Circular economy adapted products, production technologies and processes (such as the design and introduction of reusable, recyclable and refurbished materials, components and products, circular tools and services) and/or certified eco efficient products. |

| b. | Utilisation of issue proceeds Clause 1 of Chapter IX of SEBI Circular dated December 17, 2021 | The extant SEBI framework for GDS do not mandate disclosure of temporary placement for the balance of unallocated net proceeds, if any.

GBP 2021 have recommended that the issuer should make known to investors the intended types of temporary placement for the balance of unallocated net proceeds. In view of the same, the temporary utilization of proceeds raised for green debt securities may be specified in order to have better disclosure and increased transparency. |

In addition to the existing disclosure requirements, we may include that, the issuer shall disclose the intended types of temporary placement for the balance of unallocated net proceeds. |

| c. | Utilisation of issue proceeds

Clause 2 of Chapter IX of SEBI Circular dated December 17, 2021 |

The extant SEBI framework for GDS do not mandate disclosure of utilization of issue proceeds for each debt security issued by an issuer.

GBP 2021 recommends that the proceeds of Green Bonds can be managed per bond (bond-by-bond approach) or on an aggregated basis for multiple green bonds (portfolio approach). In order to have clear distinction between the uses of proceeds of multiple issuances of green debt security by a single issuer for various green projects, bond by bond approach may be adopted. |

In addition to the existing disclosure requirements, we may include that, the utilisation of proceeds from each issue of GDS made by an issuer shall be tracked and disclosed separately (i.e. on a bond by bond approach) or on an aggregated basis for multiple green bonds (portfolio approach). |

| D. | Disclosure Requirements

Clause 2 of Chapter IX of the SEBI circular dated December 17, 2021 |

The extant SEBI framework for GDS does not mandate disclosure of taxonomy, standards, certifications, etc. referred for project selection by the issuer.

GBP 2021 recommends the issuer to provide information, if relevant, on the alignment of projects with official or market-based taxonomies, related eligibility criteria, including if applicable, exclusion criteria; and also disclose any green standards or certifications referenced in project selection. In line with recommendations of GBP 2021, the aforementioned disclosure may be made applicable to issuers of GDS. |

In addition to the existing disclosure requirements for selection of projects to be financed through GDS, we may include that, the issuer shall disclose any taxonomies, green standards or certifications, if referenced in the project selection. Issuers should provide information regarding the alignment of projects with said taxonomies, related eligibility criteria, including if applicable, exclusion criteria. |

| e. | Disclosure Requirements

Clause 1 of Chapter IX of the SEBI circular dated December 17, 2021 |

With respect to refinancing of assets from proceeds of GDS, the extant SEBI framework requires the issuer to disclose details of projects and/ or assets or areas where the issuer proposed to utilize the proceeds of the issue of GDS including towards refinancing of existing green projects and/or assets, if any.

GBP 2021 recommends the following: – In the event that all or a proportion of the proceeds are or may be used for refinancing, issuers provide an estimate of the share of financing vs. re-financing, and where appropriate, also clarify which investments or project portfolios may be refinanced, and, to the extent relevant, the expected look-back period for refinanced eligible Green Projects. – In line with recommendations of GBP 2021, the disclosure of utilization of proceeds of green debt securities is proposed to be aligned with GBP principles for better disclosure on use of proceeds for refinancing. |

In order to enhance disclosure requirements for refinancing of projects through GDS, Clause 1.4 of Chapter IX of the SEBI circular dated December 17, 2021 may be amended as follows:

“a. Details of identified project(s) and/or asset(s) where the issuer proposes to utilise/ allocate the proceeds of the issue of GDS. b. In case a portion of the proceeds of the issue are proposed to be utilized/ allocated for refinancing, the following details shall be disclosed with regard to such refinancing: i. Details of projects/portfolios that are proposed to be refinanced. ii. Percent share of financing and refinancing. iii. Look-back period for refinanced Green Projects. Explanation: “Look-back period” in the clause above refers to a maximum period in the past that an Issuer will look back to identify assets/earlier disbursements to such eligible green projects that will be included in the disclosures associated with the green debt securities issued.” |

| f. | Disclosure Requirements

Clause 1 of Chapter IX of the SEBI circular dated December 17, 2021 |

The extant SEBI framework does not provide for specific disclosure regarding identification and management of perceived social and environmental risks associated with the projects to be financed through GDS.

GBP 2021 recommends, “the issuer should provide complementary information on processes by which the issuer identifies and manages perceived social and environmental risks associated with the relevant project(s)”. In line with recommendations of GBP 2021, the issuer may be required to disclose the processes by which the issuer identifies and manages perceived social and environmental risks. |

In addition to the existing disclosure requirements in the offer documents, the issuer may provide information on processes by which the issuer identifies and manages perceived social and environmental risks associated with the project(s) proposed to be financed/ refinanced. |

| g. | Disclosure Requirements

Clause 1 of Chapter IX of the SEBI circular dated December 17, 2021 |

The extant SEBI framework provides that an issuer of GDS may appoint an independent third party reviewer/ certifier, for reviewing/ certifying the processes including project evaluation and selection criteria, project categories eligible for financing by green debt securities, etc. Such appointment is at the option

of the issuer; however, any such appointment of reviewer/ certifier, is required to be disclosed in the offer document. In this regard, GBP 2021 recommends the following: – issuers should appoint (an) external review provider(s) to assess through a pre-issuance external review the alignment of their Green Bond or Green Bond programme and/ or Framework with the four core components of the GBP. – Post issuance, it is recommended that an issuer’s management of proceeds be supplemented by the use of an external auditor, or other third party, to verify the internal tracking and the allocation of funds from the Green Bond proceeds to eligible Green Projects. – The GBP encourage external review providers to disclose their credentials and relevant expertise and communicate clearly the scope of the review(s) conducted. Issuers should make external reviews publicly available on their website and/or through any other accessible communication channel as appropriate and if feasible, as well as use the template for external reviews available in the sustainable finance section of ICMA’s website. In line with the recommendations of GBP 2021, the disclosure requirement may be amended to disclose the aforementioned information. |

In order to enhance disclosure requirements for third party review and certification of projects and processes with regard to issues of GDS, Clause 1.5 of Chapter IX of the SEBI circular dated December 17, 2021 may be amended as follows:

“Appointment of third party reviewers/ certifiers/ auditors: An issuer may appoint external reviewers/ certifiers/ auditors for purposes including, but not limited to, (i) assessment of alignment of the objectives of the green bond to be issued with the clause XX of this circular (ii) post-issue management of use of proceeds from the green bond (iii) verification of the internal tracking and the fund allocation from the Green Bond proceeds to eligible Green Projects etc. Such appointment is optional for the issuer. However, any such appointment of reviewer/ certifier/ auditor shall be disclosed in the offer document(s). Such external reviews shall also be disclosed on the stock exchanges where the bonds are listed or proposed to be listed.” |

| h. | Disclosure Requirements

Clause 2 of Chapter IX of the SEBI circular dated December 17, 2021. |

The extant SEBI framework provides that an issuer of green debt securities

or any agent appointed by the issuer complying with globally accepted standard(s) for the issuance of green debt securities including measurement of the environmental impact, identification of the project(s) and/ or asset(s), utilisation of proceeds, etc., shall disclose the same in the offer document and/ or as part of continuous disclosures. With regard to impact reporting, the GBP 2021 recommends the following: – The annual report should include a list of the projects to which Green Bond proceeds have been allocated, as well as a brief description of the projects, the amounts allocated, and their expected impact. In line with recommendations of GBP 2021, the disclosure requirements may be amended to provide for impact reporting as such disclosure will enable investors to gather information pertaining to the impact of the project on the environment. |

In addition to the existing disclosure requirements for

measurement of impact reporting, the following may also be included: a. “Impact Reporting: “An issuer, or any agent appointed by the issuer shall disclose information pertaining to reporting of the environmental impact of the projects financed by the green debt securities in the offer document and/or as a continuous disclosure. Reporting standards or taxonomies followed by the issuer with regard to reporting of environmental impact may also be disclosed, if any. Such disclosure is optional and is at the part of issuer and may be done on a project-by-project basis.” |

10.1 Views/ comments sought on:

a. Is there a need to revisit the existing green bond framework on the lines of the GBPs mentioned above? If so, which are the recommendations that have to be adopted?

b. Please offer comments on whether any additional policies/ schemes, if any.

11. Greenwashing

11.1. One of the main hurdles for further growth has been a consistent and robust approach to identifying what is considered ‘green’. A lack of clarity in this regard leads greenwashing which is defined as the practice of channelling proceeds from green bonds towards projects or activities having negligible or negative environmental benefits. Various issuers in the past have been accused of greenwashing, and the same has caused significant reputational risk for socially conscious investors seeking to diversify their investment portfolios by investing in environmental, social and governance (ESG) practices.

11.2. Bankers and lenders are cautious about financing new asset classes in the green bond market in the absence of adherence to widely accepted standards and taxonomies. On the other hand, no issuer would want to risk their reputation by issuing a bond which is criticized for not being adequately green or transformational, particularly due to lack of availability of a domestic green assessment framework to rate them in a transparent and uniform manner.

11.3. SEBI guidelines on green bonds provide a list of categories wherein funds raised through debt securities are eligible to be classified as ‘green’ debt securities.

11.4. While China and the European Union (EU) have issued their own taxonomies regarding assets eligible to be financed through ‘green’ bonds, India does not have a detailed taxonomy of such assets. Further, in the absence of the same, major issuers such as SBI, Yes Bank, IREDA etc. have their own internal green bond frameworks to identify and finance projects.

11.5. In this regard, it is proposed that the list of sectors identified as “eligible” under the SEBI framework may be updated in line with the updated ICMA guidelines and market feedback/public consultations.

11.6. As per extant regulations, green bonds which do not permit recourse to the issuer are not available in India. However, ‘green revenue bonds’ or ‘green project bonds’ as defined by ICMA are not envisaged under extant SEBI Regulations.

11.7. Similarly, ‘securitized debt obligations’ as defined under SEBI (Issue and Listing of Securitized Debt Instruments and Security Receipts) Regulations, 2008 that may have ‘green’ assets in their underlying asset pool are also excluded from the current framework.

11.8. Feedback is sought regarding addition of such ‘alternative’ debt securities as defined by ICMA to be considered as eligible ‘green debt securities’. An indicative description of the same is as follows:

a. Green Revenue Bonds which limit exposure to the green project being financed and does not provide recourse to the issuer may

b. Green Project Bond which provides for credit exposure to a single / multiple green projects, with or without recourse to the issuer

c. Green securitized bonds collateralized by cash flows from the projects.

11.9. Views/ comments sought on:

a. Whether such sub-categorization of green bonds will help reduce greenwashing?

b. Please offer comments on whether any additional regulatory/ technical solutions against greenwashing?

12. Public Comments on this Consultation Paper Public comments are invited on the proposal. The comments/ suggestions may be provided as per the format given below:

|

Name of the person/entity proposing comments: |

||||

| Name of the organization (if applicable): | ||||

| Contact details: | ||||

| Category: whether market intermediary/ participant (mention type/ category) or public (investor, academician etc.) | ||||

| Sr. No. | Extract from Consultation Paper | Issues (with page/para nos., if applicable) | Proposals/ Suggestions | Rationale |

Kindly mention the subject of the communication as, “Comments on Consultation Paper on Green and Blue Bonds as a mode of Sustainable Finance”.

Comments as per aforesaid format may be sent to the following, latest by August 31, 2022, in any of the following manner:

a. By email to: pradeepr@sebi.gov.in; nikhilc@sebi.gov.in; and vikramj@sebi.gov.in; or

b. By post to the following address:

Pradeep Ramakrishnan,

General Manager,

Department of Debt and Hybrid Securities,

Securities and Exchange Board of India,

SEBI Bhavan, C4-A, G-Block,

Bandra Kurla Complex, Bandra (East),

Mumbai – 400051

Issued on: August 04, 2022

Notes:

1 https://www.worldbank.org/en/topic/financialsector/brief/sustainable-finance

2 Subsumed in the Operational Circular on the NCS Regulations, 2021 – please see Chapter IX

3 https://www.ft.com/content/32dbf37c-8ff5-436b-88f3-9873fc864a7b

4 https://www.climatebonds.net/2022/01/500bn-green-issuance-2021-social-and-sustainable-acceleration-annual-green-1tn-sight-market

5 https://www.indiabudget.gov.in/budget2020-21/economicsurvey/index.php

6 https://www.indiabudget.gov.in/budget2021-22/economicsurvey/index.php

7 https://www.mea.gov.in/Speeches-

Statements.htm?dtl/34466/National_Statement_by_Prime_Minister_Shri_Narendra_Modi_at_COP26_Summit_in_Glasgow

8 https://powermin.gov.in/sites/default/files/Revised_Biomass_Policy_dtd_08102021.pdf

9 https://pib.gov.in/Pressreleaseshare.aspx?PRID=1650096

10 https://www.niti.gov.in/e-mobility-national-mission-transformative-mobility-and-battery-storage

11 https://www.niti.gov.in/sites/default/files/2022-02/Need-for-ACC-Energy-Storage-in-India.pdf

12 https://www.iea.org/policies/7455-india-cooling-action-plan-icap

13 https://WWW.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/green-bond-principles-gbp/

14 https://seea.un.org/content/natural-capital-accounting-and-valuation-ecosystem-services-india

15 https://pib.gov.in/PressReleasePage.aspx?PRID=1799067

16 https://www.worldbank.org/en/news/infographic/2017/06/06/blue-economy

17 https://www.worldbank.org/en/news/feature/2018/10/29/sovereign-blue-bond-issuance-frequently-asked-questions

18 https://pib.gov.in/newsite/PrintRelease.aspx?relid=170138