Repatriation of funds holds crucial significance for non-residents and Non-Resident Indians (NRIs), necessitating a comprehensive understanding of regulations and taxation. This guide elucidates the permissible limits, requisite permissions, and taxation nuances governing fund repatriation from India.

Repatriation of Funds by NRIs:

Brief:

√ Max Limit without RBI permission: USD 1 Million.

√ Above USD 1 Million, need RBI prior approval.

√ Remittance should be by NRI only.

√ Remittance should be from his/her NRO account in India.

√ Funds remitted can be one of the following:

i. balances held in NRO accounts

ii. sale proceeds of assets

iii. the assets acquired by way of inheritance/legacy

Detailed Text:

As per Foreign Exchange Management (Remittance of Assets) Regulations, 2016, Para 4 “Permission for remittance of assets in certain cases”, Regulation 2:

A Non-Resident Indian (NRI) or a Person of Indian Origin (PIO) may remit through an authorised dealer an amount, not exceeding USD 1,000,000 (US Dollar One million only) per financial year,

(i) out of the balances held in the Non-Resident (Ordinary) Accounts (NRO accounts) opened in terms of Foreign Exchange Management (Deposit) Regulations, 2016/ sale proceeds of assets/ the assets acquired by him by way of inheritance/ legacy on production of documentary evidence in support of acquisition, inheritance or legacy of assets by the remitter;

(ii) Under a deed of settlement made by either of his parents or a relative (relative as defined in Section 2(77) of the Companies Act, 2013) and the settlement taking effect on the death of the settler, on production of the original deed of settlement;

Provided that where the remittance under Clause (i) and (ii) is made in more than one instalment, the remittance of all instalments shall be made through the same Authorised Dealer.

Provided further that where the remittance is to be made from the balances held in the NRO account, the account holder shall furnish an undertaking to the Authorised Dealer that “the said remittance is sought to be made out of the remitter’s balances held in the account arising from his/ her legitimate receivables in India and not by borrowing from any other person or a transfer from any other NRO account and if such is found to be the case, the account holder will render himself/ herself liable for penal action under FEMA.

Further, as per Regulation 7 “Reserve Bank’s prior permission in certain cases” of the said regulations:

A person who desires to make a remittance of assets in the following cases, may apply to the Reserve Bank, namely:

(i) Remittance exceeding USD 1,000,000 (US Dollar One million only) per financial year –

(a) on account of legacy, bequest or inheritance to a citizen of foreign state, resident outside India; and

(b) by a Non-Resident Indian (NRI) or Person of Indian Origin (PIO), out of the balances held in NRO accounts/ sale proceeds of assets/ the assets acquired by way of inheritance/ legacy.

(ii) Remittance to a person resident outside India on the ground that hardship will be caused to such a person if remittance from India is not made;

II. Repatriation of Funds by Resident Individuals:

Brief:

√ Resident Individuals can freely remit funds from India under Liberalised Remittance Scheme (LRS).

√ LRS maximum limit is upto USD 2,50,000 per individual per financial year.

√ Purpose of remittance should be other than negative list in detailed text below.

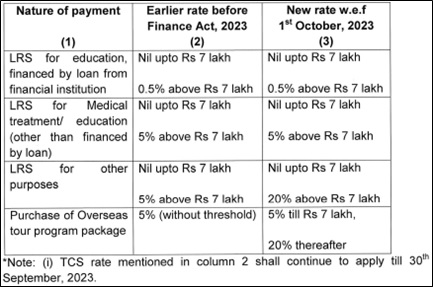

√ Upto INR 7 Lakhs no TCS shall apply.

√ Above INR 7 Lakhs, TCS shall apply:

i. For remittances made upto 30th Sep, 2023 – @5%

ii. For remittances made on/after 1st Oct, 2023 – @20%

√ TCS paid is NOT a cost, and can be claimed as refund/set-off against other tax liability by filing the income tax return

√ Gift is not taxable in hands of recipient between relatives (definition in detailed text)

Detailed Text:

Under the Liberalised Remittance Scheme, all resident individuals, including minors, are allowed to freely remit up to USD 2,50,000 per financial year (April – March) for any permissible current or capital account transaction or a combination of both.

Individuals can avail of foreign exchange facility for the following purposes within the LRS limit of USD 2,50,000 on financial year basis:

i. Private visits to any country (except Nepal and Bhutan)

ii. Gift or donation

iii. Going abroad for employment

iv. Emigration

v. Maintenance of close relatives abroad

vi. Travel for business, or attending a conference or specialised training or for meeting expenses for meeting medical expenses, or check-up abroad, or for accompanying as attendant to a patient going abroad for medical treatment/ check-up

vii. Expenses in connection with medical treatment abroad

viii. Studies abroad

ix. Any other current account transaction which is not covered under the definition of current account in FEMA 1999

The AD bank may undertake the remittance transaction without RBI’s permission for all residual current account transactions which are not prohibited/ restricted transactions under FEMA Act/Regulations. It is for the AD to satisfy themselves about genuineness of transaction, as hitherto.

The remittance facility under the Scheme is not available for the following:

i. Remittance for any purpose specifically prohibited under Schedule-I (like purchase of lottery tickets/sweep stakes, proscribed magazines, etc.) or any item restricted under Schedule II of Foreign Exchange Management (Current Account Transactions) Rules, 2000.

ii. Remittance from India for margins or margin calls to overseas exchanges / overseas counterparty.

iii. Remittances for purchase of FCCBs issued by Indian companies in the overseas secondary market.

iv. Remittance for trading in foreign exchange abroad.

v. Capital account remittances, directly or indirectly, to countries identified by the Financial Action Task Force (FATF) as “non- cooperative countries and territories”, from time to time.

vi. Remittances directly or indirectly to those individuals and entities identified as posing significant risk of committing acts of terrorism as advised separately by the Reserve Bank to the banks.

vii. Gifting by a resident to another resident, in foreign currency, for the credit of the latter’s foreign currency account held abroad under LRS.

For remittances under LRS, Tax Collection at Source (TCS) shall apply as per Section 206C of the Income Tax Act, 1961 as per below summary table:

Further, Money received from relatives, by way of Gift is not chargeable to tax in the hands of recipient in terms of Section 56(2).

Relatives of an individual for this purpose shall mean:

a) Spouse of the individual;

b) Brother or sister of the individual;

c) Brother or sister of the spouse of the individual;

d) Brother or sister of either of the parents of the individual;

e) Any lineal ascendant or descendent of the individual;

f) Any lineal ascendant or descendent of the spouse of the individual;

g) Spouse of the persons referred to in (b) to (f).

Conclusion:Navigating the landscape of fund repatriation entails a nuanced understanding of regulatory frameworks and taxation implications. Non-residents and NRIs must adhere to prescribed limits, obtain necessary approvals, and comply with taxation requirements to facilitate seamless fund transfers. By staying abreast of regulations and leveraging available exemptions, individuals can optimize fund repatriation processes while ensuring compliance with applicable laws.

Author Bio