Page Contents

Type of TDS / TCS Return Form

Deductor is liable to deduct tax and file the TDS Return. There are various types of TDS Return Forms that are applicable for different situations based on the Nature of Income of the deductee or the type of deductee on whom the TDS is imposed.

| Type of TDS Return Form | Particulars of the TDS Return Form |

| Form 24Q | Statement for tax deducted at source from salaries |

| Form 26Q | Statement for tax deducted at source on all payments other than salaries. |

| Form 27Q | Statement for tax deduction on income received from interest, dividends, or any other sum payable to non residents. |

| Form 27EQ | Statement of collection of tax at source. |

| Form 27D | Tax Collection Certificate in respect of deductees, reported in Form 27EQ Statements |

24Q: In this form the deductor should file the Tds for the employees whose salary is taxable.

26Q: In this form the deductor deduct the Tds on various services such as Rent, Contractor, Legal & Profession, and Interest other than securities, Commission, Interest on Securities, Winning from lotteries.

27Q: This form is based on the payments of foreigners and NRIs other than salary. It is compulsory for non govt. Deductors to mention the PAN in the form.

27D: This form is based on Tax Collection at Source (TCS). TCS is basically the tax that is collected by Seller from Buyer of certain goods when debiting the amount payable to the account of buyer by buyer or when receiving the amount from the buyer in the form of cheque, cash, demand draft or other modes of payment for selling certain prescribed goods as per the Section 206C (1) for the purpose of business and not for personal us.

27EQ: The Declaration is a quarterly statement of TCS. TCS is basically the tax that is collected by Seller from Buyer of certain goods when debiting the amount payable to the account of buyer by buyer or when receiving the amount from the buyer in the form of cheque, cash, demand draft or other modes of payment for selling certain prescribed goods as per Section 206C (1) for the purpose of business and not for personal use.

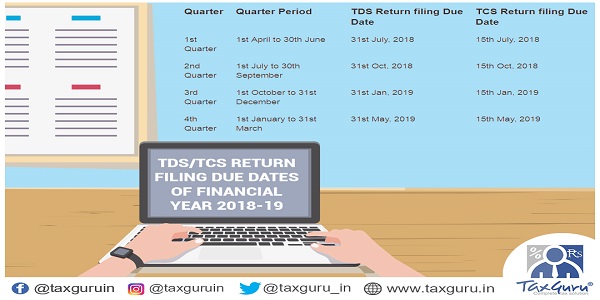

TDS/TCS Return Filing Due Dates of Financial Year 2018-19

| Quarter | Quarter Period | TDS Return filing Due Date | TCS Return filing Due Date |

|---|---|---|---|

| 1st Quarter | 1st April to 30th June | 31st July, 2018 | 15th July, 2018 |

| 2nd Quarter | 1st July to 30th September | 31st Oct, 2018 | 15th Oct, 2018 |

| 3rd Quarter | 1st October to 31st December | 31st Jan, 2019 | 15th Jan, 2019 |

| 4th Quarter | 1st January to 31st March | 31st May, 2019 | 15th May, 2019 |

TCS Rates for F.Y. 2016-17 to 2018-19

Section |

Nature of Payment |

Thres-hold Amount |

TCS Rates (%) |

|||||

|---|---|---|---|---|---|---|---|---|

F. Y. 2016-17 to 2017-18 |

F. Y. 2018-19 |

|||||||

Individual / HUF |

Other |

Individual / HUF |

Other |

|||||

| 206C | Scrap | – | 1 | 1 | 1 | 1 | ||

| 206C | Tendu Leaves | – | 5 | 5 | 5 | 5 | ||

| 206C | Timber obtained under a forest lease or other mode | – | 2.5 | 2.5 | 2.5 | 2.5 | ||

| 206C | Any other forest produce not being a timber or tendu leave | – | 2.5 | 2.5 | 2.5 | 2.5 | ||

| 206C | Alcoholic Liquor for human consumption | – | 1 | 1 | 1 | 1 | ||

| 206C | Parking Lot, toll plaza, mining and quarrying | – | 2 | 2 | 2 | 2 | ||

| 206C | Minerals, being coal or lignite or iron ore (applicable from July 1, 2012) | – | 1 | 1 | 1 | 1 | ||

| 206C | Bullion if consideration (excluding any coin / article weighting 10 grams or less) exceeds Rs. 2 Lakhs | – | 1 | 1 | 1 | 1 | ||

| 206C | TCS on sale in cash of any goods (other than bullion/jewellery) | 200000 | – | – | 1 | 1 | ||

| 206C | TCS on providing of any services (other than Ch-XVII-B) | 200000 | – | – | 1 | 1 | ||

| 206C | TCS on Motor Vehicle | 1000000 | – | – | 1 | 1 | ||

Interest for Late Payment of TDS

Interest should be paid before filing of TDS return

| Section | Nature of Default | Interest subject to TDS/TCS amount | Period for which interest for late payment of TDS / TCS is to be paid |

| 201A | Non deduction of tax at source, either in whole or in part | 1% per month | From the date on which tax deductable to the date on which tax is actually deducted |

| After deduction of tax, non payment of tax either in whole or in part | 1.5% per month | From the date of deduction to the date of payment |

Penalty for filling Late TDS Return

Under Section 234E, you will have to pay a fine of Rs 200 per day (two hundred) until your return is filed. You have to pay this for every day of delay until the fine amount is equal to the amount you are supposed to pay as TDS.

In case of Nil Return, for 26Q Declaration is given through traces online. But it is not compulsory to give the declaration for nil return.

In case, if in any of the quarter the return for 24Q is submitted and in 4th Quarter there is no TDS deducted then also it is compulsory to file the nil return.

If there is any delay in filling nil return or in giving declaration then, there is no penalty of tax.

In case of 24Q form 16 are issued by the deductor to the employees.

In case of 26Q form 16A are issued by the deductor to others.

Author Bio

There are various types of TDS Return Forms that are applicable for different situations based on the Nature of Income of the deductee or the type of deductee on whom the TDS is imposed.

Realy This article help to us to know about TDS AND TCS Froms