Taxability on sale of Foreign Currency

In this 21st century, purchase or sale of Foreign Currency (‘FC’) {herein together referred to as FOREX Transaction) is very common transaction. There can be various reasons to make such FOREX Transaction some examples are listed below:

-Visit outside India on a foreign tour;

-To make payments to vendors situated outside India;

-Receipt of sale consideration from customer;

-Investment in foreign securities of foreign assets outside India;

-Medical treatment abroad; etc.

However, there is always an ambiguity on, whether a particular sale of FC would attract tax in India under the Income tax Act 1961(“the Act”) or whether appreciation in FC would be liable to tax. It is important to understand tax implication on sale of FC, as Foreign Exchange Management Act, 1991 (‘FEMA’} allows an individual to hold FC equivalent to USD 2,50,000 on account of current account transaction. In this article an attempt has been made to conclude, whether conversion of one currency into another is taxable or not.

Let us first understand the taxability from an individual perspective who does not conduct any business activity, he purchases the FC for personal purpose, which may be medical treatment abroad or for a foreign trip outside India. However on completion of the mentioned purpose, if an individual is left with balance currency then he will have to surrender it to Authorized dealer within 180 days from the date or receipt or date of return to India as per Regulation 7 of FEMA Regulation 2015. It might be possible, from the date of purchase and up to the date of sale there can be appreciation in FC and due to which a person can make profits on such sale of FC. However, there can be loss on such sale of FC if there is a devaluation of such FC.

As and when there is a transaction of sale, we need to check the tax implication on the same. Since in this case we have already clarified above there is no business activity, the question of such conversion getting taxed under the head ‘Profits and Gains from Business or Profession’ does not arise. Now we proceed to check taxability under the capital gains head for such transaction. In this regard Section 45 provides for chargeability which reads as under:

“Any profits or gains arising from the transfer of a capital asset effected in the previous year shall, save as otherwise provided in sections 54, 54B, 54D, 54E, 54EA, 54EB, 54F, 54G and 54H, be chargeable to income-tax under the head “Capital gains”, and shall be deemed to be the income of the previous year in which the transfer took place.”

Capital gains head would trigger on fulfilment of three parameters, first there should be transfer, second there should be transfer of capital asset and at last there should be profits and gains from the transfer. Here it is important to note that profits and gains includes losses on such transfer. If all the three are satisfied we can say sale of FC are taxable under the head capital gains.

First parameter is there should be transfer, in this regard Section 2(47) of the Act gives an inclusive definition which inter alia includes sale, exchange, relinquishment of asset, extinguishment of any rights. Can a mere conversion from one currency to another can be said as transfer. It was held in by Karnataka High Court in case of Jayakumari and Dilharkumari [1986] 29 Taxman 177, the relevant extract is reproduced hereunder:

The ‘transfer’ contemplated under section 2(47) envisages, no doubt, sale exchange or relinquishment of the asset, etc. But mere conversion of one currency into another currency cannot be considered as ‘exchange’. The exchange in the context must mean transfer of one capital asset from another capital asset. Like a sale it requires two persons. There cannot be a sale to oneself. So too in the case of exchange. In the present case, the ownership of the money remained with the assessee even after the exchange in the first place. Secondly, it was just a conversion of one kind of currency into another kind in the normal course and not connected with any business. Such a conversion could never be considered as exchange within the meaning of section 2(47).

Karnataka High Court has ruled out the possibility to consider FC transaction as sale or exchange, as it requires transaction between two persons. The said decision was also upheld by Madras High Court in case of E.I.D. Parry Ltd (38 Taxman 84). Hence the requirement of first parameter itself are not satisfied.

Conclusion – Taxability will not trigger on conversion of one currency to another

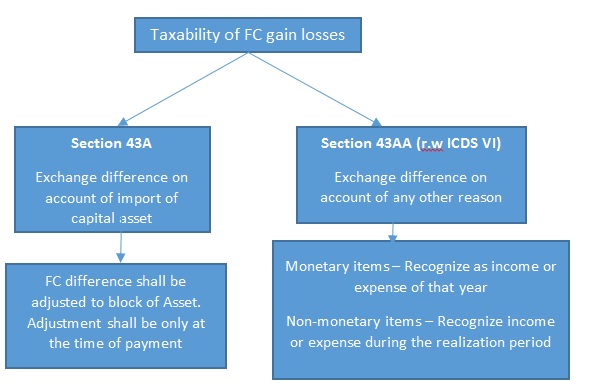

Now, let’s understand these topic from business perspective. If a person is doing business and when he enters into any transaction in foreign currency, he is exposed to exchange fluctuation risk on such transaction unless the same is hedged by the person through hedging techniques such as Forward Contracts, Invoicing in FC etc. The risk associated with such transactions may result into either Exchange Gain or Exchange Loss. Since there is a business activity, any income arising due to such business would attract Section 28 of the Act. Once Section 28 gets triggered, we are under the business head and there is a separate section under this head to charge tax on such income.

The summary of taxability under the Business head is explained under the flow chart as follows-

Flow chart – Taxability on sale of Foreign Currency

For more details regarding monetary and non-monetary items it is advisable to refer Income Computation Disclosure Standard VI (‘ICDS VI)