The stage is set to catch hold the shifting of profit from high tax jurisdiction to low tax jurisdiction. Yes, the reading is correct, the OECD embarked upon another pioneering journey to introduce a concept of global minimum tax, called Pillar 2. The objective behind the introduction of pillar 2 is that each jurisdiction levies a minimum tax, failure of which will reallocate the taxing right to another jurisdiction. This write-up aims to provide the readers with a prima facie understanding of this new framework.

The key component of pillar 2, commonly referred to as the “global minimum tax” or “GloBE,” delves into a minimum effective tax rate of at least 15%, calculated based on a specific rule set. In sum and substance, a Group with an Effective Tax Rate (“ETR”) below the minimum of 15 % in any particular jurisdiction would be required to pay top-up tax (“TUT”).

ETR of the jurisdiction is determined by dividing the amount of covered taxes by the amount of income as determined under the GloBE rules. Thus, the GloBE rule will only apply if ETR is less than the Minimum tax rate of 15%. The shortfall will result in TUT liability.

The Mechanics to recover the TUT liability are as follows:

Domestic Minimum Top-up Tax (“DMTT”) – The GloBE rules provide the primary taxing rights to the jurisdiction having a taxation rate below ETR i.e known as Low Tax Jurisdiction (“LTJ”). Thus LTJ will have the first right to tax the entity situated therein. If the LTJ does not implement the DMTT, it will provoke the Income Inclusion Rule, explained in the ensuing para.

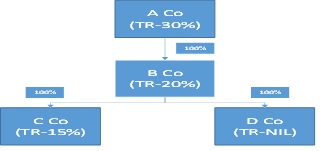

Income Inclusion Rule (“IIR”) – IIR imposes a top-up tax on a parent entity in respect of the income of subsidiaries and permanent establishments that is taxed at less than a 15% minimum effective tax rate. The Ultimate Parent Entity (“UPE”) has the first priority to pay the IIR liability in respect of the entity in LTJ. However, if the UPE does not implement the GloBE rule then the liability to pay IIR shifts to the Immediate Parent Entity (“IPE”). Let us understand the IIR Rule with the following example:

Country D does not levy the tax on the income earned by the entities there and thus it will be termed LTJ. Now, the primary right to collect tax with respect to the income of D Co would lie with Country D via imposing a minimum tax rate known as DMTT.

However, on failing to impose the DMTT by Country D will trigger the IIR Rule and consequently, Country A being UPE will be able to recover TUT under IIR.

Further, there might be a scenario where the UPE i.e Country A in the given case does not impose the IIR. In such a scenario, the liability to pay IIR shifts to the jurisdiction of the next parent entity i.e County B in the given case above will collect the IIR from B Co (Immediate Parent Entity “IPE”). The above approach is known as the top-down approach.

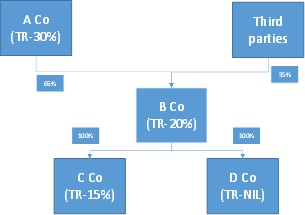

The top-down approach has one exception, where more than 20% of the ownership interest in Immediate Parent Entity is held by parties outside the MNE group, the first priority to pay the IRR liability of LTJ shifts in favor of such partially owner entity. The below example would help to clarify the position:

Here, more than 20% of the ownership interest in B Co. is held by a third party, the liability to pay tax with respect to D Co will shift to B Co. This approach is known as the Split ownership approach.

At last, if the TUT is not recovered as per the IIR then Under-Taxed Payments Rule (UTTR) acts as a backstop to collect TUT. Where none of the jurisdictions are able to recover the TUT under the IRR then the same is recovered via UTTR. The top-up tax would be collected under the UTPR by the countries in which the other entities are located. The mechanism to collect TUT under UTTR is based on the relative level of a substance in the form of tangible assets and employed in each UTTR implementing jurisdiction. The number of employees and the net book value of tangible Assets each account for half of the UTPR percentage of the UTPR Jurisdiction.

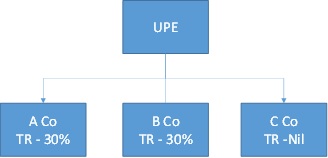

The following pictographic example would help in a better understanding of UTTR

Here, Country C has a nil tax rate as an LTJ. Assuming UPE does not implement IRR, the tax of LTJ will be collected via UTTR by Country A and Country B in equal proportion of net book value and tangible assets.

Exception to GloBE Rule – The GloBE Model Rules will apply to MNEs that have consolidated revenues of EUR 750 million in at least two out of the last four years.

Authored by : Chintan Rachh and CA Priyanka Hotchandani.