When it comes to planning for retirement, one of the most popular investment options in India is the National Pension System (NPS). This government-sponsored scheme allows individuals to save for their retirement while also providing tax benefits. However, understanding the ins and outs of the NPS can be overwhelming, which is why it’s important to have a comprehensive guide. In this article, we’ll cover everything you need to know about the NPS, including its features, benefits, and how to get started. So, let’s dive in!

To develop and regulate the pension sector, Government of India establishes “Pension Fund Regularly and Development Authority” on dated 10th Oct., 2003.This authority made or draft a new pension scheme under the name “National Pension Scheme” that has been implemented w.e.f 01st Jan 2004.

Initially, this pension scheme is applicable only on all government employees except employees of armed forces. But w.e.f 01st may 2009 , this scheme made open for all citizens of India on voluntary basis. Whether you are form organized sector or unorganized sector, you may invest under the new scheme.

In union budget 2010-11, a new additional scheme named “Swavalaban Scheme” has been introduced. Under this scheme, government deposits ₹1,000/- into the pension subscriber account if subscriber deposits ₹1,000/- or more into the pension account. This scheme is applicable to all except the following: –

a. Center Government Employees

b. State Government Employees

c. Employees of Autonomous Body

After some years this scheme has been closed and later replaced with “Atal Pension Yojna” probably in F.Y 2016-17.

Central Recordkeeping Agency

A Central Recordkeeping Agency has been made so that proper implementation of the pension scheme can be made. some of the main work of Central Recordkeeping Agency are as follow:

a. Recordkeeping

b. Maintaining data

c. Administration

d. Customer service function

Now, who is Central Recordkeeping Agency?

National Security Depository Limited (NSDL) is Central Recordkeeping Agency for the purpose of National Pension Scheme.

Point of Presence

These are the places where all the offline work is done like account opening, all type of customer services and only here the person gets into direct contact with the agency’s employee to get knowledge about np sans to get assistance or help regarding the national pension scheme.

Different institutions like banks and other has been registered as Point of Presence. Annuity Service Provider

These are responsible for delivering a regular monthly pension. More details have been discussed in withdrawal section.

How to get register under NPS?

Offline:

Go to any Point of Presence with the required Documents, they will guide, assists and help for the rest procedure.

Some of the required Documents are:

- Aadhar card

- Pan Card

- Passport size photograph

And others

Online:

Go to website of NSDL i.e. enps.nsdl.com

On this website, you will find instruction about NPS subscription

Click on National Pension Scheme then on registration

Then fill your details and do the required procedures.

Note: “Take professional advice before registration”

NPS CHARGES

National Pension Schemes is one of the cheapest investment products available with extremely low charges, Pension Fund Manager fees are capped at 0,01% compared to 2.2,5% for mutual funds, Other charges in the NPS are also extremely low as you will notice from the table below,

| Intermediary | Charge head | Service Charges* |

| CRA (Central

Record-Keeping Agency) |

Account Opening charges | Rs. 50 |

| Annual Maintenance cost per account | Rs. 190 | |

| Charge per transaction | Rs. 4 | |

| POP (Point-of- Presence) | Initial subscriber registration and contribution upload | Rs. 100 |

| Initial contribution upload | 0.25% of the initial contribution amount from subscriber subject to a minimum of Rs,20 and a maximum of Rs,25,000 |

NOTE: This charges may change, please check the latest one.

As soon as person get registration, he/she will get a UNIQUE PRAN i.e. “Permanent Retirement Account Number”.

This number will remain always same even if you change your employer or you change yourself from employee to self-employment or vice versa.

Type of accounts under NPS

| BASIS | TIER 1 | TIER 2 |

| Compulsory or optional | This account is Compulsory i.e. when you register under this scheme, you will get tier 1 account. |

This is Optional / Voluntary |

| Tax Exemption | Tax Exemption Allowed for the amount deposited in this account | Tax Exemption Not Allowed for the amount deposited in this account.

But in Budget 2019, Finance Minister of India, announce that if you deposit amount in tier 2 with a lock-in period of 3 years, then tax exemption is allowed. |

| Initial Contribution | Minimum ₹500/- | Minimum ₹1,000/- |

| Annual minimum contribution | ₹1,000/- | N.A |

| Contribution per installment | Minimum ₹5000/- | Minimum ₹250/- |

TAX EXEMPTIONS

| SECTION UNDER INCOME TAX ACT,1961 | TAX EXEMPTION LIMIT IN AMOUNT |

| Section 80c | Maximum ₹1,50,000/- under this section |

| Section 80ccd(1b) | Exemption of ₹50,000/- in addition to above Section |

| Section 80ccd(2) | Exemption to amount against employer’s contribution |

NOTE: – in case of employer’s contribution maximum limit for exemption is limit to 1/10th of the salary i.e. basic pay plus dearness allowance.

Return on NPS

There is no fixed rate of return in NPS like other investments like FDRs.

CLASSIFICATION OF ASSETS UNDER NPS

a. Equity (E)

b. Corporate Bond (C)

c. Government Bond (G)

d. Alternative Asset (A)*

*Alternative Asset mainly includes Real Estate Investment Trust (REIT) and Infrastructure Investment Trust (InVITs).

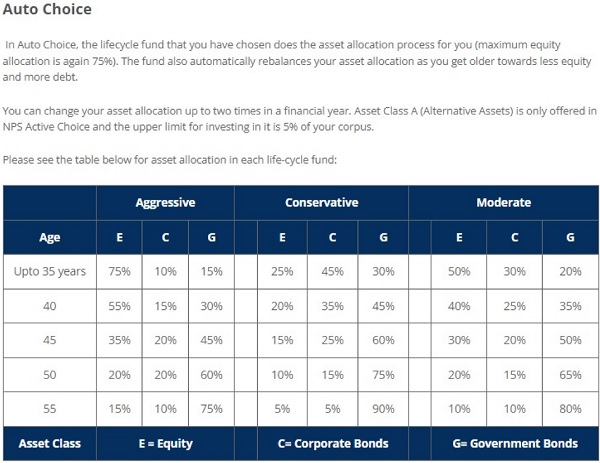

Now, the question arises here is how much of our contribution will invest or classify under which assets, the answer to this question is that there are two choices in hands of NPS Subscriber :

a. Active choice

b. Auto choice

Allocation under different choices can be seen in the following tables:

Equity Allocation Matrix in Active Choice:

| Age | Max. Equity Allocation |

| Upto 50 years | 75% |

| 51 years | 72.5% |

| 52 years | 70% |

| 53 years | 67.5% |

| 54 years | 65% |

| 55 Years | 62.5% |

| 56 Years | 60% |

| 57 Years | 57.5% |

| 58 Years | 55% |

| 59 Years | 52.5% |

| 60 Years | 50% |

WITHDRAWAL/EXIT FROM NPS

Generally, maturity under this scheme comes when the subscriber attains the age of 60 years, rather the person may extend it up to age of 70 years on voluntary basis.

For the amount accumulated at the time of maturity, you may withdraw the 60% of the amount as lump-sum amount and may purchase the annuity for the balance.

Now, the main question arises here that whether in any emergency or need, can amount from NPS be withdrawn?

So the answer to that is, there is a lock in period of 3 years from the date of account opening, after that a person may withdraw the amount for only three times during the life before the maturity and this withdrawn amount cannot exceed the 25% of the contribution amount under this scheme.

Additionally, this amount can be withdrawn before maturity in some pre-stated cases or situation after fulfilling certain criteria. Some of those situations are as follow-

a. Children education

b. Children marriage

c. First house buy/build

d. Critical illness

Etc.

*****

Disclaimer: The views expressed are the personal views of the author only. Therefore, the same should not be considered as final opinion on the subject matter. There may be other views also. So, the readers are advised to consider all the points before relying upon the above write ups. The write up is only for academic purposes and not for professional use.

Author Bio