In simple terms the Income Tax Return is the document wherein the assesse submits its earned income to Government and makes payment for the services and facilities availed by him called as tax which is supposed to be used by the Government for the welfare of the country only.

Technically speaking the form approved by Income Tax Authorities as per the requirements of the Income Tax Act 1961 is commonly called as the Income Tax Return comprising of various heads of income under which the assessment is done. broadly speaking the Income Tax Return is divided in to following five heads of income-

1. Income from Salary

3. Profits and Gains from Business and Profession

4. Capital Gains

As per the requirement of the law, the income earned in the previous year is assessed in the subsequent year which is called the Assessment year.

To simplify, it means that the income earned in the year 2018-19(Previous year) will be furnished to Government in the form of Income Tax Return in the year 2019-20(Assessment Year) as applicable in the respective cases of the assesses depending upon the amount of income earned and subsequent falling in the particular slab.

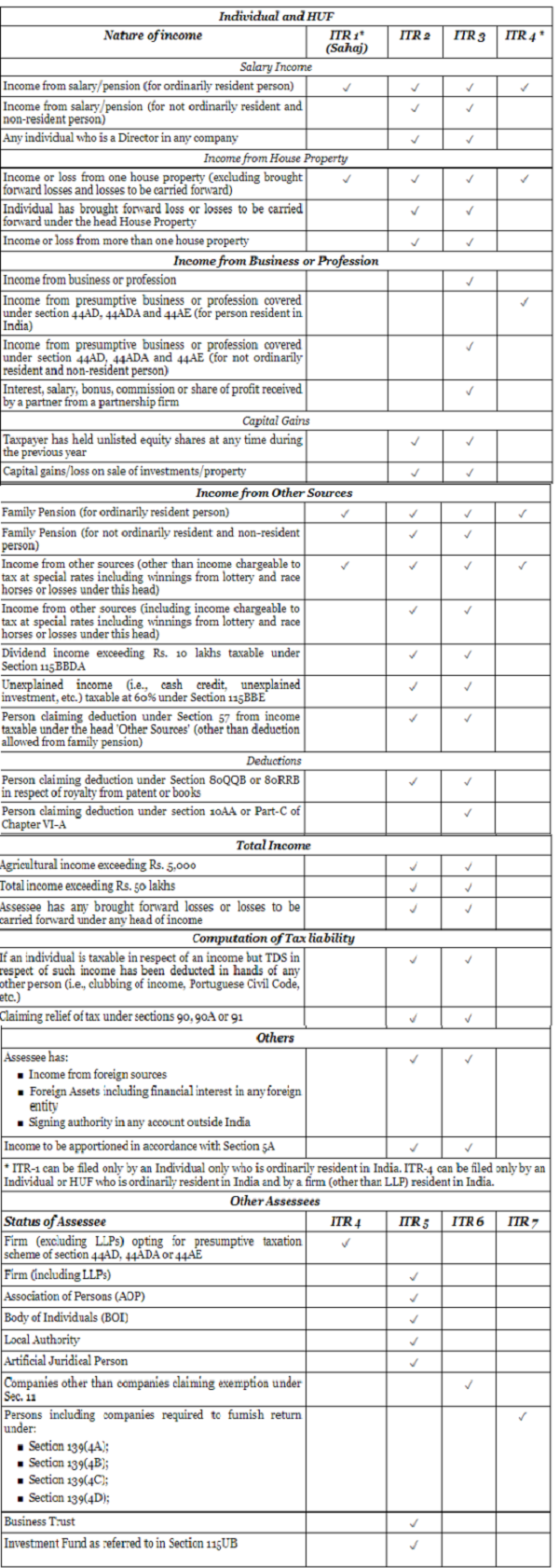

Selection of the ITR form

– After logging in the E-Filing account at the Government website- www.incometaxindiaefiling.gov.in click the filing link appearing on the screen

– Select the assessment year

– Applicable ITR form is to be selected

This is the most important part while filing income tax return on the portal. The assesse has to select the right ITR form while filing return on the portal failing which the ambiguity will prevail for the Government as well as the assesse. It will make the return defective or may consider as not filed.

CBDT has notified new ITR forms for AY 2019-20 and FY 2018-19 as explained below-

Documents required while Filing Income Tax Returns-

1. Form 16 for salaried class

Form 16 is the document issued by the employer to its employees wherein the details of the deduction of tax(TDS on salaries as per Sec 194) is shown for the previous year. Based upon the deductions made in the form 16 and the corresponding salary income earned in the previous year, the employee furnishes its income tax return on the govt portal along with any other deductions etc which were not part of the Form 16.

2. Interest Certificates from Banks/ Post offices etc

This is required while showing your income under the head of income from other sources. The interest received by the assesse on his savings is cumulated and summed up figure is shown while filing Income Tax Return.

3. Form 16 A/ B/ C

This is applicable when banks have already deducted your tax say on eth fixed deposits etc. the amount of tax already deducted will get adjusted while finalizing the final figure of tax to be paid to the Government.

4. FORM 26 AS

The form 26 AS can be downloaded from TRACES which is infact a government portal wherein the details of all your deducted tax under form 16, 16 A, 16 B, 16 C etc are consolidated and showed in a compiled form. This is required to re-verify the deductions made and the final figures to be shown while filing the income tax return.

5. Proofs of investments done for saving tax

The Income Tax Act 1961 allows the assesses to save its tax amount by investing its income in the various Government approved schemes for tax benefits. Accordingly the assesse who has invested his income under the various schemes as applicable can declare such amounts under the Chapter VI A i.e. deductions being shown from Sec 80C onwards.

6. Home Loan Statements

Where an assesse has taken a home loan, the interest paid on the loan is deducted from the income of house property. Where there is no income from house property but still loan has been taken for construction etc, the loss i.e. negative income can be shown under the head income from house property and the same gets adjusted in the final income. For adjusting the amount of loss / interest amount, the statement from bank is required while filing income tax return.

7. AADHAR Card

Last but not the least is the AADHAR card. It’s a mandatory requirement while filing your income tax return. Sec 139 AA of the Income Tax Act requires that every individual who is filing his income tax return has to mention his AADHAR card number and in case the same is applied for then the corresponding enrolment number has to be mentioned in the return form.

Author Bio

please let me know which ITR 2 or 3 to be filled up

for NRI have income below 2.50 ;lacs in india.

since TDS has been deducted on NRO SB AC is to be claimed.

Madam, Thanks for above details. But, the details of Income from Captial Gains is not elaborated properly. We well know that ITR-3 is mandatory those who are receiving income from Capital Gain. But, more number of professionals (CA/CS/ICWA/Advocate) are doing Long Term investment in Shares. (NOT day to day trading) and they are filing Lengthy ITR-3 unnecessarily whose income may be 5 to 10 lakhs only.

(1) In these cases, shall they file ITR-4 (presumptive) which include “Income from Profession AND Income from Long Term Investment (i.e) Capital Gain by selecting

“income from other sources” ?

(2) If yes, whether any limit is available ? For example ITR-4 can file (?) Income From profession and Income from Captial Gain does NOT exceed 50 Lakhs only ? Is it correct ?