Case Law Details

JCIT Vs Dozco India Private Limited (ITAT Kolkata)

The Income Tax Appellate Tribunal, Kolkata, considered the Revenue’s appeal and the assessee’s cross objection against the order dated 22.01.2026 passed by the National Faceless Appeal Centre (NFAC) under Section 250 of the Income-tax Act, 1961 for Assessment Year 2012-13. The Tribunal first took up the assessee’s cross objection, as it challenged the validity of the appellate proceedings.

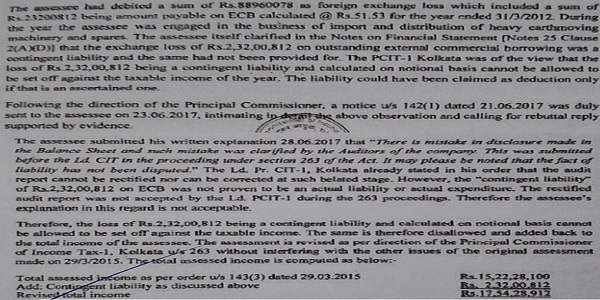

The assessee had filed its return of income on 22.09.2012 declaring income of ₹7,06,02,924. An assessment under Section 143(3) was completed on 29.03.2015 determining income at ₹15,22,28,100 under the normal provisions. Subsequently, the Principal Commissioner of Income Tax passed an order under Section 263 on 13.02.2017 directing the Assessing Officer to frame a fresh assessment. Pursuant to those directions, the Assessing Officer passed an order under Sections 263/143(3) on 03.08.2017 making an addition of ₹2,32,00,812 on account of contingent liability.

The assessee appealed against the fresh assessment. Before the CIT(A), it contended that the foreign exchange liability was an ascertained liability and not a contingent liability. It furnished the computation of the foreign exchange loss, submitted that the loss had been accounted for in accordance with Accounting Standard (AS)-11 prescribed by the ICAI by marking foreign exchange fluctuations to market, and relied upon the decisions in CIT v. Woodward Governor India Pvt. Ltd., Oil and Natural Gas Corpn. Ltd. v. DCIT, and DCIT v. Bank of Bahrain and Kuwait. The CIT(A) observed that the assessee had consistently claimed foreign exchange losses based on the exchange rate prevailing at the end of each financial year and that the same accounting principle had been followed in other years without any similar addition. On that basis, the CIT(A) directed deletion of the addition of ₹2,32,00,812 and allowed the appeal.

Aggrieved by the relief granted, the Revenue filed an appeal before the Tribunal. In its cross objection, the assessee challenged the validity of the proceedings themselves, contending that the order passed under Section 263 was void ab initio because the original assessment order under Section 143(3) no longer existed in law. The assessee submitted that the original assessment order dated 29.03.2015 had been quashed by the CIT(A) as being barred by limitation, that the Revenue’s appeal against that decision had been dismissed by the Tribunal by order dated 22.08.2023, and that the Tribunal’s order had subsequently been affirmed by the Calcutta High Court by order dated 14.08.2024. The assessee argued that once the original assessment ceased to exist, the consequential proceedings under Section 263 and the fresh assessment made pursuant thereto were also invalid.

The Revenue supported the impugned order but did not dispute that the Tribunal’s earlier order regarding the original assessment had been affirmed by the Calcutta High Court.

The Tribunal noted that the original assessment under Section 143(3) had been quashed as barred by limitation, that the Revenue had failed before both the Tribunal and the Calcutta High Court, and that the finding had attained finality. It further observed that, although the Principal Commissioner had passed the order under Section 263 while the original assessment proceedings were under challenge, the original assessment had ultimately been held to be non-existent in law. Consequently, the Tribunal held that any consequential order passed under Sections 263/143(3) could not survive and was invalid and void ab initio.

The Tribunal relied upon the judgment of the Calcutta High Court in Keshab Narayan Banerjee v. CIT, wherein it was held that when proceedings initiated under Section 147 were invalid, proceedings under Section 263 originating from those orders could not be initiated.

Accordingly, the Tribunal accepted the assessee’s contention, held that the consequential assessment order passed under Sections 263/143(3) was invalid and void ab initio, and allowed the cross objection. In view of this finding, the Tribunal held that it was unnecessary to examine the merits of the addition relating to foreign exchange loss. The Revenue’s appeal was dismissed as infructuous.

Cases Discussed:

- Keshab Narayan Banerjee vs. CIT, (1999) 238 ITR 694 (Cal.).

- DCIT v. Bank of Bahrain and Kuwait, (2010) 132 TTJ 0505 (SB).

- Oil and Natural Gas Corpn. Ltd. v. DCIT, 261 ITR (AT) 1 (Delhi ITAT).

- CIT v. Woodward Governor India Pvt. Ltd., 312 ITR 254 (SC).

FULL TEXT OF THE ORDER OF ITAT KOLKATA

These appeals and cross objection have been filed by the revenue and assessee are directed against the orders dated 22.01.2026 of the National Faceless Appeal Centre, Delhi (hereinafter referred to as the “Id. CIT(A)”) passed u/s 250 of the Income-tax Act, 1961 (hereinafter referred to as “the Act”) for the assessment year (A.Y.) 2012-13.

2. In the present case, the assessee has challenged the validity of the order passed u/s 250 of the Act. Hence, we are taking CO No.37/Kol/2026 for A.Y. 2012-13 as ‘lead’ case.

C.O. No.37/KoI/2026 (A.Y. 2012-13):

3. The facts of the case in brief are that the appellant filed its return of income on 22.09.2012, declaring income of Rs.7,06,02,924/- for A.Y. 2012-13. Subsequently, the case was completed u/s 143(3) of the Act on 29.03.2015 at income of Rs.15,22,28,100/- under normal provision. Further, the assessment was reviewed by Id. PCTI-1, and given direction u/s 263 of the Act to the AO vide order dated 13.02.2017 to pass a fresh assessment. The assessment proceedings were completed vide 263/143(3) order dated 03.08.2017 by making addition of Rs.2,32,00,812/- on account of contingent liability.

4. Aggrieved by the said order, the assessee preferred appeal before the Id. CIT(A), wherein the appeal of the assessee has been allowed by Id. CIT(A) by observing as follows:

“5. Appellate finding and decision:

5.1 I have perused the form no.35, grounds of appeal, the impugned assessment order, the written submissions and the facts of the case.

5.2 The background of the issue is that Id PCIT-1, Kolkata passed order u/s 263 dated 13.02.2017 on the specific issue of disallowance of contingent liability on external commercial borrowing (ECV) which was claimed as deduction in the profit and loss account by the appellant company. The assessment was framed afresh by the AO vide order dated 03.08.2017 wherein the addition of Rs.2,32,00,812/- was made by the AO by observing as under:

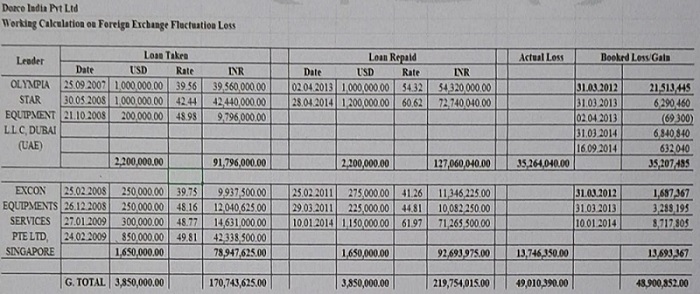

5.3 The appellant during the course of appellate proceedings has contended that the said liability was not contingent but an ascertained liability. The appellant has further given the exact working of the computation of the forex loss as under:

5.4 The appellant has further contended that the loss was booked as per the AS-11 prescribed by the ICAI by which the forex fluctuations are marked to market (MTM) and need to daim along with the expenses.

5.5 The appellant has further relied upon the decision of the Hon’ble Apex Court in the case of CIT v Woodward Governor India Pvt Ltd. 312 ITR 254 (SC). The appellant has also relied upon the decisions of Hon’ble 1TAT in the case of Oil and Natural Gas Corpn Ltd v DC1T 261 1TR (AT) 1 (Del 1TAT) and DCIT v Bank of Bahrain and Kuwait (2010) 132 TTJ 0505 (SB).

5.6 I have considered the submission of the appellant as well as the fact of the case. It is noted that the appellant had claimed the forex losses based on the rate of currency at the end of each financial year. Further it is noted that the appellant has followed the same accounting principle with respect to forex losses over other years as well but no addition has been made in other years except the relevant previous year 2011-12.

5.7 In view of the above the addition of Rs.2,32,00,812/- made by the AO is hereby directed to be deleted. The appellant gets relief on all the grounds of appeal.

6. In the result, the appeal filed by the appellant is treated as allowed.”

5. Being aggrieved, dissatisfied, the revenue filed appeal before us. In the appellate proceedings, the assessee has preferred Cross Objection, which we have taken first to decide it. The learned Authorized Representative (Id. AR) challenges the very impugned order thereby submitting that order passed by the Id. PCIT u/s 263 of the Act is void an initio since the original order u/s 143(3) of the Act never existed in laws as it was quashed by the Id. CIT(A) by holding that it is barred by limitation and the said order has been confirmed by the ITAT in an appeal filed by the revenue. The Id. AR submits that when the original order has been set-aside so the consequential order passed by the AO in pursuant to the order passed u/s 263 of the Act is invalid and void ab initio. The Id. AR further submits that order passed by the ITAT in which the appeal of the revenue has been dismissed has been confirmed by the Hon’ble Calcutta High Court when the revenue has preferred appeal before the Hon’ble High Court against such order. The Id. AR placed the following documents: (i) Original assessment order u/s 143(3), dated 29.03.2015, (ii) ITAT Order dated 22.08.2023 and (iii) Calcutta High Court order dated 14.08.2024.

6. Contrary to that, learned Senior Departmental Representative (Id. Sr. DR) supports the impugned order but did not raise any doubt, the order passed by the ITAT confirmed by Calcutta High Court in the original assessment order passed u/s 143(3) of the Act.

7. Upon hearing the submission of the Id. AR of the representative parties and on perusal of the facts, we find that original assessment order in the present case was passed on 29.03.2015. The assessee appealed against the same before the Id. CIT(A) that was allowed as barred by limitation. The revenue preferred appeal against the order passed by the Id. CIT(A) before the ITAT and Hon’ble ITAT vide its order dated 22.08.2023, dismissed the appeal of the revenue by confirming the order passed by the Id. CIT(A). The revenue carried the matter before the Hon’ble Calcutta High Court where in order passed by the ITAT has confirmed by dismissing the appeal of the revenue. It is a fact that when the matter was pending before the Id. CIT(A), Id. PCIT passed an order u/s 263 of the Act on the limited ground that the assessee claimed foreign exchange loss, which was contingent in nature and set-aside the matter to the AO to verify. The AO passed the order u/s 143(3) r.w.s. 263 of the Act and disallowed the said loss as contingent in nature. It is an admitted fact that an order passed by the AO u/s 143(3) r.w.s. 263 of the Act was placed before the Id. CIT(A), wherein the Id. CIT(A) allowed the appeal of the assessee by following the judgement of the various Court. Now, the revenue has filed against the same. There is no dispute that original order passed u/s 143(3) of the Act never existed in law as it was quashed by Id. CIT(A) as barred by limitation and the order passed by the Id. CIT(A) has attained its finality as the revenue has lost its battle up to the Hon’ble High Court. Since the order passed u/s 143(3) of the Act is become a non-existence so any consequential order passed by the AO u/s 143(3)/263 of the Act is invalid and void ab initio.

8. The Id. AR placed reliance on the judgement of Hon’ble Calcutta High Court in case of Keshab Narayan Banerjee vs. CIT, (1999) 238 ITR 694 (Cal.), wherein it has been held that whether where in absence of valid service of notice, orders u/s 147 passed against appellant were bad in law, proceedings u/s 263 originating from such orders could not be initiated against appellant.

9. Keeping in view the discussion made above, we find substance in the arguments of the Id. AR that when the original order u/s 143(3) of the Act never existed in law and quashed by Id. CIT(A) as bared by limitation, so the consequential order passed by the AO u/s 263/143(3) of the Act is invalid and void ab initio. Hence, the Cross Objection of the assessee is hereby allowed.

10. Since, we have decided the Cross Objection in favour of the assessee, hence, it is needless to discuss on merits and the appeal filed by the revenue (ITA No.1018/Kol/2026) becomes infructuous and hereby dismissed.

11. In the result, the appeal of the revenue is dismissed whereas the CO filed by the assessee is allowed.

The order is pronounced in the open Court on 08/07/2026.

Author Bio