Case Law Details

Arun Machaiah Cheppudira Somaiah Vs ITO (ITAT Bangalore)

The assessee filed an appeal before the ITAT Bangalore against the order dated 24.01.2025 passed by the Commissioner of Income Tax (Appeals), National Faceless Appeal Centre, Delhi under Section 250 of the Income-tax Act, 1961, for Assessment Year 2017-18.

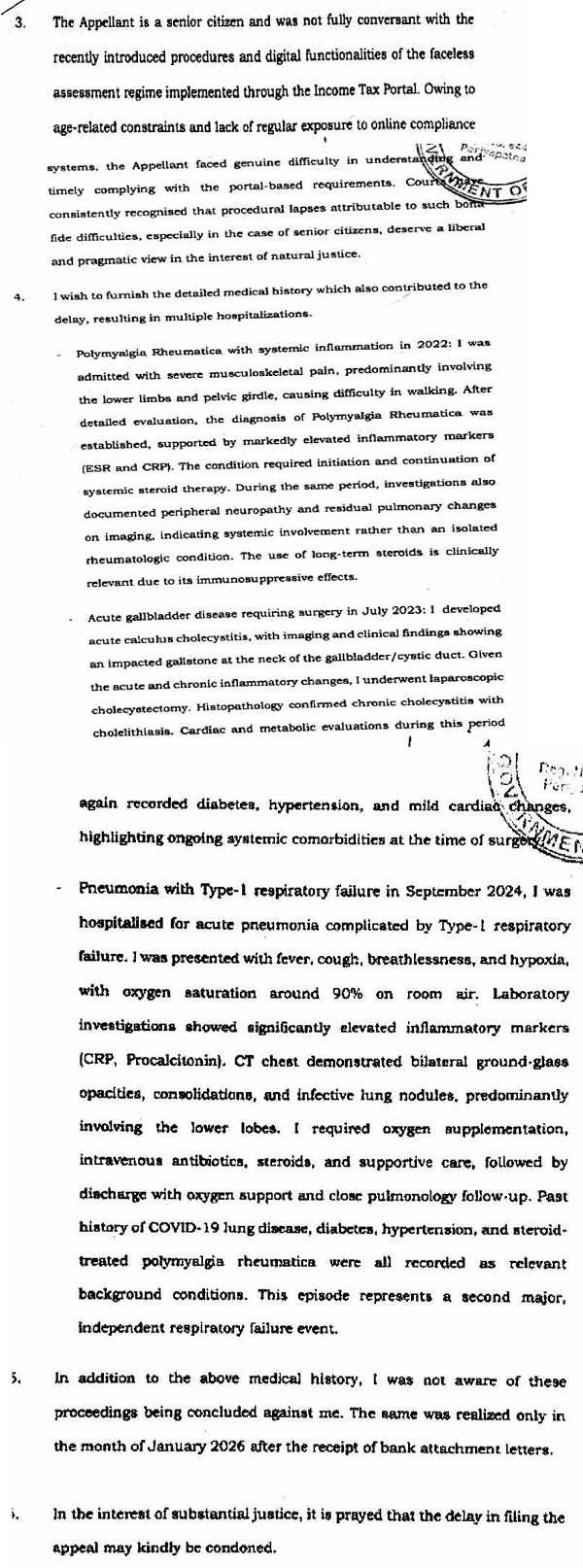

The appeal was delayed by 667 days. The assessee filed an application for condonation of delay supported by an affidavit explaining the reasons for the delay. The Tribunal found that the reasons fell within the parameters laid down by the Supreme Court in Collector Land Acquisition, Anantnag vs. MST Katiji and others, reported in 1987 SCR (2) 387. Referring to the principle that rules of procedure are handmaids of justice and that substantial justice should prevail over technical considerations, the Tribunal observed that the assessee did not stand to benefit from the delayed filing. On examining the affidavit, it held that sufficient cause had been shown and condoned the delay before proceeding to decide the appeal.

The assessee challenged the assessment on several grounds, including that the assessment order was bad in law, violated the principles of natural justice, and that the CIT(A) had passed the appellate order for non-prosecution without complying with Sections 250(6) and 250(4). The assessee also challenged the addition of 竄ケ22,18,713 made under Section 69A of the Act, contended that Section 69A was inapplicable to the facts of the case, alleged that the addition was based on surmises and presumptions, challenged the initiation of penalty proceedings under Section 271AAC(1), and disputed the demand raised under Section 156.

After considering the submissions and examining the material on record, the Tribunal noted that the CIT(A) had passed the impugned order ex parte due to the non-appearance of the assessee or his representative. Before the Tribunal, however, the assessee was represented by counsel and expressed the intention to pursue the appeal against the addition made by the Assessing Officer.

The Tribunal further found that the CIT(A) had dismissed the appeal merely on account of non-compliance with notices and had not adjudicated the grounds raised by the assessee on merits as required under Section 250(6) of the Act. Accordingly, the Tribunal considered it appropriate to set aside the impugned order and restore the matter to the file of the CIT(A) for de novo adjudication on merits.

The Tribunal directed that no order should be passed without affording the parties a reasonable opportunity of hearing. It also directed the assessee to appear before the CIT(A) on all dates of hearing fixed without default. Since the matter was restored to the CIT(A) for adjudication on merits, the Tribunal held that the remaining grounds raised in the appeal did not require adjudication at that stage. The appeal was accordingly allowed for statistical purposes.

FULL TEXT OF THE ORDER OF ITAT BANGALORE

1. The assessee has filed the present appeal against the impugned order dated 24.01.2025, passed under section 250 of the Income Tax Act, 1961 (“the Act”) by the learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre, Delhi [“learned CIT(A)”] for the assessment year 2017-18.

2. The present appeal is delayed by 667 days. Along with the appeal, the assessee has filed an application seeking condonation of delay, which is duly supported by the affidavit sworn by the assessee, submitting as follows: –

3. We find that the reasons stated by the assessee for seeking condonation of delay fall within the parameters for grant of condonation laid down by the Hon’ble Supreme Court in the case of Collector Land Acquisition, Anantnag vs. MST Katiji and others, reported in 1987 SCR (2) 387. It is well-established that the Rules of procedure are handmaid of justice. When substantial justice and technical considerations are pitted against each other, the cause of substantial justice deserves to be preferred. In the present case, the assessee did not stand to benefit from the late filing of the present appeal. In view of the above and having perused the affidavit filed by the assessee, we are of the considered view that there exists sufficient cause for not filing a present appeal within the limitation period, and therefore, we condone the delay in filing the appeal by the assessee, and we proceed to decide the appeal.

4. In this appeal, the assessee has raised the following grounds: –

1. The order passed by the Ld AO and CIT(A) in so far as it sustain additions to the impugned order in this appeal is totally opposed to law equity weight of evidence probabilities facts and circumstances of the case.

2. The impugned order of assessment is bad in law and void-ab-initio as assessment was concluded much opposed to the principle of natural justice.

3. The Ld.CIT(A) has erred in law and facts in passing orders on account of non-prosecution without adhering to the provisions of Section 250(6) and Section 250(4), which require a speaking order on merits.

4. The additions were made behind the back of the assessee and thus the assessment order require to be annulled.

5. The Ld.AO has erred in Law and on Facts in making addition of addition of Rs. 22,18,713 on account of cash deposits under the provisions of Section 69A of the Act.

6. The Ld.AO/CIT(A) have erred in law and on facts in not appreciating that provisions of Section 69A are not applicable to the facts in the present case given the background of the Appellant.

7. Since the addition has been made merely on the basis of surmises and presumptions, the impugned order is bad in law and liable to be quashed.

8. The order is unreasonably high-pitched and therefore liable to be quashed in its entirety.

9. The learned AO and CIT(A) have erred in law and on the facts in initiating a penalty Proceedings under section 271AAC(1) of the Act.

10. The learned AO and CIT(A) have erred in raising a demand vide issue of notice under section 156 of the Act.

5. We have considered the submissions of both sides and perused the materials available on record. In the present case, at the outset, it is evident that the learned CIT(A) has passed the order ex partedue to the non-appearance of/on behalf of the assessee. Now, in the present appeal before us, the assessee is duly represented by the learned AR and wishes to pursue the litigation against the addition made by the AO. We further find that the learned CIT(A) merely on the basis of non-compliance with the notices, dismissed the appeal filed by the assessee without adjudicating the grounds raised by the assessee on merits, as required under section 250(6) of the Act. Consequently, we deem it fit and proper to set aside the impugned order and restore the matter to the file of the learned CIT(A) for de novo adjudication of the appeal on merits. We further direct that no order shall be passed without affording reasonable opportunity of hearing to the parties. The assessee is directed to appear before the learned CIT(A) on all the dates of hearing as may be fixed without any default. As the matter is being restored to the file of the learned CIT(A) for adjudication on merits, the other grounds raised by the assessee in the present appeal do not call for adjudication at this stage. Accordingly, the grounds raised by the assessee are allowed for statistical purposes.

6. In the result, the appeal by the assessee is allowed for statistical purposes.

Order pronounced in the open court on 11th June, 2026.