Section 194R – FIR – First Information Report TDS on Benefits or Perquisites under Income Tax Act 1961

Why – Objectives of Taxation System & Canons of Taxation– Policy decision & procedural implementation

-To increase the Tax base under the Act

-To plug & detect the leakages of Tax Revenues arising on accounts of Benefits or Perquisites provided in the ordinary course of business or profession under the Act

-Thus, Section 194R is made applicable with the effect from July 1,2022 only.

Judicial Support

-Circular issued on July 7,1964 – 20-D of 1964 – Reference

Value of rent free accommodation as provided u/s 17(2) but it was issued giving reference of advocate providing services to the company as a lawyer

But tax levy was never demanded or emphasized in regular assessment proceedings of the tax payers

But of late, trend is changing to treat such transactions as subject to levy arising or accruing in direct or indirect or ancillary or incidental manner forming part of income of PGBP.

No valuation mechanism provided under the Act till date as I understand. Thus, valuation needs to be adopted as understood in common parlance. (Section 295(2)(c))

-Is Benefits defined under the Act? – undefined but reference provided u/s 28(iv) – PGBP

-Is perquisite defined under the Act? – defined under Income from Salaries – restrictive applicability

-Guidelines issued as approved by CG vide circular No.12/2022 dt 16.06.22 are applicable and binding on income tax authorities and specified tax payers providing such benefits or amenities.

Section 28(iv) – Profits and Gains of Business or Profession

(iv) the value of any benefit or perquisite, whether convertible into money or not, arising from business or the exercise of a profession;

Applicable to all the Taxpayers carrying on business or profession

Taxpayers is receiving such tax benefits from connected stakeholders of the business ( PGBP)

Includes benefits received in Cash or kind

Section 17(2) – Definition of Perquisite

Income from Salaries – Source of Income

17 (2) “perquisite” includes—

(i) the value of rent-free accommodation provided to the assessee by his employer;

(ii) the value of any concession in the matter of rent respecting any accommodation provided to the assessee by his employer;

Explanations 1 to 4………….

Provisos……………….

“family”, in relation to an individual, shall have the same meaning as in clause (5) of section 10; and

Section 10(5) – Family

10 (5) in the case of an individual, the value of any travel concession or assistance received by, or due to, him,—

(a) from his employer for himself and his family, in connection with his proceeding on leave to any place in India;

(b) from his employer or former employer for himself and his family, in connection with his proceeding to any place in India after retirement from service or after the termination of his service,

subject to such conditions as may be prescribed (including conditions as to number of journeys and the amount which shall be exempt per head) having regard to the travel concession or assistance granted to the employees of the Central Government:

Provided that the amount exempt under this clause shall in no case exceed the amount of expenses actually incurred for the purpose of such travel:

Provided further that for the assessment year beginning on the 1st day of April, 2021, the value in lieu of any travel concession or assistance received by, or due to, such individual shall also be exempt under this clause subject to the fulfilment of such conditions (including the condition of incurring such amount of such expenditure within such period), as may be prescribed.

Explanation 1.—For the purposes of this clause, “family”, in relation to an individual, means—

(i) the spouse and children of the individual; and

(ii) the parents, brothers and sisters of the individual or any of them, wholly or mainly dependent on the individual.

Explanation 2.—For the removal of doubts, it is hereby clarified that where an individual claims exemption and the exemption is allowed under the second proviso in connection with the prescribed expenditure, no exemption shall be allowed under this clause in respect of such prescribed expenditure to any other individual;

Section 295 – Power to make rules

Power to make rules.

295. (1) The Board may, subject to the control of the Central Government, by notification in the Gazette of India, make rules for the whole or any part of India for carrying out the purposes of this Act.

(2) In particular, and without

(a) the ascertainment and determination of any class of income; prejudice to the generality of the foregoing power, such rules may provide for all or any of the following matters:

(b) the manner in which and the procedure by which the income shall be arrived at in the case of—

(i) income derived in part from agriculture and in part from business;

(ii) persons residing outside India;

(iia) operations carried out in India by a non-resident;]

(iib) transactions or activities of a non-resident;]

(iii) an individual who is liable to be assessed under the provisions of sub-section (2) of section 64;

(c) the determination of the value of any perquisite chargeable to tax under this Act in such manner and on such basis as appears to the Board to be proper and reasonable;

Section 194 – Deduction of tax on benefit or perquisite in respect of business or profession.

194R. (1) Any person responsible for providing to a resident, any benefit or perquisite, whether convertible into money or not, arising from business or the exercise of a profession, by such resident, shall, before providing such benefit or perquisite, as the case may be, to such resident, ensure that tax has been deducted in respect of such benefit or perquisite at the rate of ten per cent of the value or aggregate of value of such benefit or perquisite:

Provided that in a case where the benefit or perquisite, as the case may be, is wholly in kind or partly in cash and partly in kind but such part in cash is not sufficient to meet the liability of deduction of tax in respect of whole of such benefit or perquisite, the person responsible for providing such benefit or perquisite shall, before releasing the benefit or perquisite, ensure that tax required to be deducted has been paid in respect of the benefit or perquisite:

Provided further that the provisions of this section shall not apply in case of a resident where the value or aggregate of value of the benefit or perquisite provided or likely to be provided to such resident during the financial year does not exceed twenty thousand rupees:

Section 194 – Deduction of tax on benefit or perquisite in respect of business or profession.

Provided also that the provisions of this section shall not apply to a person being an individual or a Hindu undivided family, whose total sales, gross receipts or turnover does not exceed one crore rupees in case of business or fifty lakh rupees in case of profession, during the financial year immediately preceding the financial year in which such benefit or perquisite, as the case may be, is provided by such person.

(2) If any difficulty arises in giving effect to the provisions of this section, the Board may, with the previous approval of the Central Government, issue guidelines for the purpose of removing the difficulty.

(3) Every guideline issued by the Board under sub-section (2) shall, as soon as may be after it is issued, be laid before each House of Parliament, and shall be binding on the income-tax authorities and on the person providing any such benefit or perquisite.

Explanation.—For the purposes of this section, the expression “person responsible for providing” means the person providing such benefit or perquisite, or in case of a company, the company itself including the principal officer thereof.

Section 194R Applicability

It is applicable to all the Taxpayers (subject to exceptions – refer to non applicability slide) carrying on business or profession who are providing any kinds of benefits or perquisites to all stakeholders deriving benefits from such business activities in direct or indirect manner (including ancillary or incidental manner).

It is applicable from July 1, 2022 onwards

Thus, it is not applicable to any kind of benefit or perquisites provided during the period April 1,2022 to June 30,2022.

If value of benefits or perquisites provided exceeds Rs.20,000/- in a financial year/previous year to each person , then only such provision is applicable.

If such benefit is less than 20,000/-, then such provision is not applicable.

Section 194R Non-applicability

Individual/HUF Taxpayer carrying on business having a sales, turnover & gross receipts of less than one crore ( ref. Section 44AB)

Individual/HUF Taxpayer carrying on profession and deriving professional receipts of less than Rs.50 lakhs ( ref. Section 44AB/44ADA – only specified professionals)

If a person is not carrying on business or profession, then it is not applicable.

194R is not applicable if such benefit or perquisite provided is less than 20K in a previous year & valuation thereof is not possible????

194R is not applicable also if such benefit or perquisite provided is treated as perquisite u/s 17(2), TDS is deducted u/s 192B of the Income Tax Act 1961 & reported in TDS Returns as well as Tax audit reports as applicable.

If benefit or perquisite provided to the employees is excluded as per the provisions of the Act, then provisions of Section 194R won’t ( Compulsory canteen facilities, medical facilities, insurance or vehicle facilities mandated by law)

Timelines

TDS on value of benefits or perquisites provided by the Taxpayer in excess of Rs.20,000/- from July 1,2022. (Does it mean Taxpayer needs to maintain record of each recipient wise in addition to books of accounts as mandated? – Answer is Yes)

TDS to be deducted @ 10% on or before providing such benefits or perquisites to any recipients or beneficiaries.

Thus, it is not applicable to any kind of benefit or perquisites provided during the period April 1,2022 to June 30,2022 but

Limit of Rs.20000/- to be computed from April 1,2022 for all such benefits or perquisite. (Accounting system needs to be configured for maintaining records from April 1,2022 for such quantifications)

Rate of TDS & TDS Compliance

Rate of TDS is specified to be 10% if PAN Number is available and if not available then rate of TDS would be 20%.

No option is provided to file application for Lower Tax deduction certificate u/s 197 of the Income Tax Act, 1961.

TDS to be deposited as per prescribed time limits specified under Chapter XVII-B of the Income Tax Act, 1961.

TDS Returns to be filed on quarterly basis in Form 26Q.

TDS certificates to be issued in Form 16A as per timelines provided under the Act.

206AB Tax compliances needs to be validated by the Taxpayers.

As Tax Auditor, you need to report such compliance under clause 34 of the Tax Audit Report in Form 3CD.

Consideration or Valuation of Benefits or Perquisites

FAQs on TDS applicability u/s 194R

Questions

Suggested Answers

Who is responsible to deduct the TDS u/s 194R ?

If Recipient is not having PAN Number then whether TDS would be deducted at 20% ? Whether surcharge and cess is applicable?

If Taxpayer has not claimed deduction in respect of such benefits and/or perquisite to provided to the Recipient , then whether TDS is deductible?

Provisions of Section 194R applicable to whom?

Does the payer need to examine as to whether Recipient of Benefits or Perquisite is subject to tax under the provisions of the Income Tax Act 1961 ?

If the value of benefits or perquisite provided or to be provided is less than 20K as per records maintained for each recipients, whether TDS needs to be deducted u/s 194R?

Taxpayer who is providing benefits and/or perquisites or any proper officer in charge of deducting such TDS as per the provisions of the Income Tax Act 1961 ?

If Recipient is not having PAN Number, then, Taxpayer needs to deduct TDS @ 20%. No surcharge and cess is to be recovered.

No, if it is not claimed as business expenditure, then, TDS provisions u/s 194R shall not apply as per my understanding.

Provisions of Section 194R are applicable to the assessees who are carrying on business or profession subject to some exceptions. (Please check non applicability slide to examine as to when such provisions are not applicable.

Payer need not examine whether recipient is liable to tax or not. Payer is just required to deduct the TDS as applicable @ 10% or as per Chapter XVII-B of the Act.

If the value of benefits or perquisite provided or to be provided is less than 20K as per records maintained for each recipient, then, TDS u/s 194R need not be reported?

–

Questions

Suggested Answers

External Recipients or Vendors

External Recipients or Vendors

If the value of benefits or perquisite provided or to be provided is more than 20K as per records maintained for each recipients, whether TDS needs to be deducted u/s 194R?

Yes, if the value of benefits or perquisite provided or to be provided is more than 20K as per records maintained for each recipients, then, TDS u/s 194R needs to be deducted.

In house employees

In house employees

If the value of benefits or perquisite provided or to be provided is less/more than 20K as per records maintained for each of the employees of the company then, whether TDS needs to be deducted u/s 194R?

When TDS deducted u/s 194R needs to be deposited with Govt. Treasury?

How TDS deducted u/s 194R would be reported by the Taxpayer in the TDS Returns?

Whether Taxpayer is required to issue TDS certificate in Form 16A to the recipient who has received such benefits or perquisite on which TDS u/s 194R is deducted?

Whether such TDS would reflected in Form 26AS/AIS of the recipient?

If TDS is not deposited by the Taxpayer within time limits prescribed, then whether interest u/s 201(1A) would be applicable?

If TDS is not deducted by the Taxpayer for providing benefits and/or perquisites, then whether such expenses would be disallowed u/s 40(a)(ii) of the Income Tax Act, 1961.

Does the Tax Auditor need to report such TDS deducted in clause 34 of the Tax Audit Report in Form 3CD?

If TDS is deducted & not deposited or not deducted but not reported in TDS Returns by the Taxpayer for providing benefits and/or perquisites, then whether such non reporting needs to be reported in clause 34 of the Tax Audit Report in Form 3CD?

If TDS is deducted and not deposited or not deducted, then whether Recovery proceedings under Chapter XVII-B can be initiated by the ITD?

Whether due to defaults in respect of the above, then whether penalty & prosecution proceedings under Chapter XVII-B can be initiated by the ITD?

If Recipients of benefits and/or perquisites, if they raise Bills/Tax Invoices/Debit Notes & if Taxpayers deduct TDS under any other sections of the Act, say 194C/194J- then whether Taxpayer needs to deduct u/s 194R of the Income Tax Act 1961?

If Recipients of benefits and/or perquisites, raise Bills/Tax Invoices/Debit Notes with GST, then whether Taxpayers can claim the same as input tax credit u/s 16 of CGST Act, 2017?

Is it mandatory for the Recipients to report such benefits and/or perquisites in his Income Tax Returns if TDS is deducted u/s 194R?, If Yes, whether as business income or as Income from Other sources?

Whether TDS deducted u/s 194R of the Income Tax Act , 1961 would be treated as prepaid tax in the hands of Recipient and it can off set against regular tax payable by the Taxpayer in his regular Income Tax Return under the provisions of the Income Tax Act, 1961 ?

Is it mandatory for the Recipients to pay advance tax in respect of such benefits and/perquisites to be received by him in view of TDS deducted u/s 194R?

Does the Taxpayer need to collect Advance Tax challan?

If advance tax challan is not provided by the Recipient, does the Taxpayer deduct the TDS at maximum marginal rate?

If the value of benefits or perquisite provided or to be provided is less/more than 20K as per records maintained for each of the employees of the company then & if TDS is deducted u/s 192B then, TDS u/s 194R need not be deducted.

TDS deducted u/s 194R should be deposited on or before 7th day of succeeding month in respect of preceding month.

Such TDS would be reported by the Taxpayer by filing quarterly TDS Returns in Form 26Q.

Yes, TDS certificate needs to be issued in Form 16A as per time limits specified under the provisions of Chapter XVII-B of the Income Tax Act 1961.

Yes, it would be reflected in Form 26AS/AIS of the recipients after the filing of TDS Returns as well as on the processing of the data by ITD.

If TDS is not deposited by the Taxpayer within time limits prescribed, then interest u/s 201(1A) would be payable. Interest payable is mandatory.

If TDS is not deducted by the Taxpayer for providing benefits and/or perquisites, then such expenses would be disallowed u/s 40(a)(ia) of the Income Tax Act, 1961 @ 30% of value of such benefits and/or perquisite if it is provided to Resident persons as defined u/s 6 of the Act.

Please note section 194R doesn’t apply to Non Resident recipient at all.

Yes, Tax Auditor needs to report such TDS deducted in clause 34 of the Tax Audit Report in Form 3CD.

Yes, if TDS is deducted or deposited or not deducted but not reported in TDS Returns by the Taxpayer for providing benefits and/or perquisites, then Tax Auditor needs to report such transaction in clause 34 of the Tax Audit Report in Form 3CD.

Yes, if TDS is deducted and not deposited or not deducted, then, Recovery proceedings under Chapter XVII-B can be initiated by the ITD.

Yes, due to defaults in respect of the above, then penalty & prosecution proceedings under Chapter XVII-B can be initiated by the ITD.

If Recipients of benefits and/or perquisites, have raised Bills/Tax Invoices/Debit Notes & if Taxpayers has deducted TDS under any other sections of the Act say 194C/194J, then Taxpayer is not required to deduct TDS once again u/s 194R of the Income Tax Act 1961.

If Recipients of benefits and/or perquisites, have raised Bills/Tax Invoices/Debit Notes with GST, then Taxpayers can claim the same as input tax credit u/s 16 of CGST Act, 2017 if all the relevant conditions and stipulations are satisfied & if not, then ITC cannot be claimed by the Taxpayer. TDS should not be deducted on GST levied on such bills if any.

It is not mandatory for the Recipients to report such benefits and/or perquisites in his Income Tax Returns even TDS is deducted u/s 194R if in his opinion it is not his income. He should ensure that he should claim the benefit of TDS in his income Tax Return without offering to such income to tax as per the provisions of Section 199 of the Income Tax Act 1961. If he decides to claim TDS, then he offer such income as business income or Income from Other sources as per his choice.

In view of the above as per his discretion, TDS can be claimed as off set against Regular tax payable while filing his income tax returns as per the provisions of the Income Tax Act 1961.

Yes, Recipients, need to pay advance tax in respect of such income arising due to benefits and/or perquisites received by them. If Advance Tax is not paid then, he may liable to pay the interest u/s 234A, 234B & 234C as applicable.

Taxpayer needs to collect the copyof advance tax from such recipient. ??????

Alternatively if such challan is not provided, does Taxpayer need to deduct TDS at maximum marginal rate i.e. 30% plus surcharge plus Cess ??????

TDS applicability u/s 194R – Specific Business Transactions

Questions

Suggested Answers

Whether TDS u/s 194R would be applicable if Trade Discounts, Cash Discounts, Rebates & Quantitative Discounts are provided to the customers or the recipients of the business activities of sales?

Whether TDS u/s 194R would be applicable if dealer conference is organised by the Taxpayer about the products of the company?

Whether TDS u/s 194R would be applicable if benefits and/or perquisites are provided to the customers or the recipients of the business activities either in cash or kind or partly in cash or partly in kind ? E.g. Incentives or Overseas Trip or Cash Price or Gold or Silver Jewellery or Free Ticket etc.

Whether TDS u/s 194R would be applicable if benefits and/or perquisites are provided to the customers or the recipients of the business activities in the form of Capital Asset? Illustrative examples

E.g. Car, Land, Immovable Property, Air Conditioner, Fridge, Mobile Phones, Laptops, Printers, Electronic Equipment’s , Free Samples given to medical Practioners ???? etc.

Whether TDS u/s 194R needs to be deducted in the hands of Recipient only or it can deducted in the hands of end user also?. For E.g. Company or alternatively its employees, directors or any other person.

Whether TDS u/s 194R needs to be deducted if any goods are provided to Social Media Influencers?

If such product is returnable?

If such product is not returnable but it is to be retained by such recipient?

If such product is to be discarded after use?

Whether TDS u/s 194R needs to be deducted if any goods are provided to Recipient for Sales or business promotions only ?

If such product is to be discarded after its use or considering prevalent trade practices of the industry in which they operate?

Whether TDS u/s 194R needs to be deducted in case of reimbursement of expenses?

In the nature of Pure agent expenses

In any other case

If Benefits and/or Perquisites as envisaged u/s 194R are provided to the Govt. Authorities, will such provisions would trigger deduction of TDS u/s 194R ?

If Benefits and/or Perquisites as envisaged u/s 194R are provided by the Govt. Authorities to the taxpayers, will such provisions would trigger deduction of TDS u/s 194R in the hands of Govt. ?

Illustrative expenses incurred by Taxpayers for the purpose of business or profession:

1. Travelling Expenses

2. Common office Expenses like Printing & Stationery, Postage & Telegram, Courier, Repairs and Maintenance, Canteen facilities, In house recreational facilities etc.

3. Staff Benefits schemes like, PF, ESIC, Super annuation, Common Healthcare & Insurance etc.

Illustrative expenses incurred by Taxpayers for the purpose of business or profession in the form of business and sales promotions:

Is Taxpayer required to deduct u/s 194R as well as u/s 194S (Virtual Digital Asset) if provided in the form of benefits and/or perquisites to the recipients ?

E.g. Credit Card Spends Points, Digital Points accumulated as POS & Salons etc.

TDS u/s 194R won’t apply if Trade Discounts, Cash Discounts, Rebates & Quantitative Discounts are provided to the customers or the recipients of the business activities properly reflected in Tax invoices issued by Taxpayer in the ordinary course of business activities of sales.

TDS u/s 194R won’t apply if such conferences are organised for Product launches, Product Training, Generating Sales Orders from the dealers/ customers, Sales Training to the dealers/customers, Addressing Queries of the dealers/ customers & reconciliation of accounts with dealers/ customers. E.g. CME meetings of Pharma Industries

Exclusions:- Conferences in the nature of benefits and/or perquisites, Leisure trips, expenses of family members of dealers/ customers, expenses incurred before and after the conferences ????, Sight seeing costs, social functions costs etc.

TDS u/s 194R would be applicable if benefits and/or perquisites are provided to the customers or the recipients of the business activities either in cash or kind or partly in cash or partly in kind. TDS should be deducted @ 10% usually on or before providing such benefits or perquisites. E.g. Incentives or Overseas Trip or Cash Price or Gold or Silver Jewellery or Free Ticket etc.

Yes, TDS u/s 194R would be applicable if benefits and/or perquisites are provided to the customers or the recipients of the business activities in the form of Capital Asset. Illustrative examples E.g. Car, Land, Immovable Property, Air Conditioner, Fridge, Mobile Phones, Laptops, Printers, Electronic Equipment’s Free Samples given to medical Practioners ???? (discussed in GST slides in detail) etc.

Yes, TDS u/s 194R can be deducted in the hands of Recipient or alternatively it can deducted in the hands of end user also based on the choice exercised by the recipient. For E.g. Company or alternatively its employees, directors or any other person (Direct or Indirect provision of Benefits and/or perquisites)

Supply of goods provided to Social Media Influencers for business promotions.

If such product is returnable, then no TDS.

E.g. Clothes, Jewellery, Footwear etc.

If such product is not returnable but it is to be retained by such recipient, then TDS needs to be deducted u/s 194R. E.g. Clothes, Jewellery, Footwear etc.

If such product is to be discarded after use, no TDS to be deducted but it may be considered as scrap sales in normal course of business. E.g. Lipsticks, perfumes, daily use items etc.

If any goods are provided to Recipient for Sales or business promotions only considering prevalent trade practices even though such product costs may be extremely high.

TDS u/s 194R need not be deducted if such product needs to be discarded after its use. For E.g. Catalogues printed by Laminate/Paints /Ready Made Garments, Wine, Liquor & Perfume Manufacturers etc.

In the case of reimbursement of expenses,

If in the nature of Pure agent expenses, then TDS need not be deducted.

In any others case, TDS needs to be deducted if not deducted under any other sections.

No, if Benefits and/or Perquisites as envisaged u/s 194R are provided to the Govt. Authorities, then, TDS provisions u/s 194R would not trigger.

No, if Benefits and/or Perquisites as envisaged u/s 194R are provided by the Govt. Authorities to the taxpayers, then also TDS provisions u/s 194R won’t trigger too.

TDS provisions u/s 194R won’t trigger as all such expenses are incurred wholly and exclusively for the purpose of business and element of personal expenditure is not present and the element of capital expenditure is absent in such expenses incurred..

TDS provisions u/s 194R won’t trigger as all such expenses are incurred wholly and exclusively for the purpose of business and element of personal expenditure is not present and the element of capital expenditure is absent in such expenses incurred.

Yes, TDS provisions u/s 194R & 194S would trigger simultaneously in such cases. For e.g.

(i) Gift card or vouchers, being a record that may be used to obtain goods or services or a discount on goods or services;

(ii) Mileage points, reward points or loyalty card, being a record given without direct monetary consideration under an award, reward, benefit, loyalty, incentive, rebate or promotional program that may be used or redeemed only to obtain goods or services or a discount on goods or services;

(iii) Subscription to websites or platforms or application.

Ref: Notification No 74 issued on June 30,2022.

Note: Exception Legally enforceable NFTs resulting into acquisition of underlying tangible asset – Notification No 75 issued on June 30,2022.

TDS default Implications for the Taxpayer

Disallowance u/s 40(a)(ia) of the Income Tax Act, 1961- 30% of such expenses to be considered as disallowable while determining Total Income u/s 28 of the Income Tax Act 1961.

Taxpayer would be termed as Assessee in Default as contemplated under Chapter XVII-B of the Income Tax Act,1961.

Demand and Recovery Proceedings can be initiated by ITD as provided under Chapter XVII-B of the Income Tax Act,1961.

Penalty and Prosecution proceedings as provided under the provisions of the Income Tax Act, 1961.

Any other provisions as may be applicable.

Compiled and Presented by CA Nitin Bhuta Mumbai 52

Implication of TDS deducted at source – Recipients

If considered as income by Recipients, liable to pay the income tax on such benefits and/or perquisites received either under PGBP or IOS, they claim TDS deducted u/s 194R as prepaid tax and pay advance tax accordingly.

If considered as income by Recipients may be liable to be covered under Tax Audit provisions u/s 44AB due to such deeming income received by them and need to comply with the provisions of the Act, accordingly.

If not considered as income by Recipients by claiming that they have not received any such benefits and/or perquisites, then they should not claim such TDS in their Return of Income. However, due to such reporting ,Tax monitoring notices and inquiries may be initiated under the provisions of the Income Tax Act, 1961 like unexplained sections provisions, scrutiny assessment, reassessment , penalties or any other proceedings as provided under the Act.

Penalty provisions under section 270A of the Income Tax Act, 1961 may trigger if such income arising due to receipts of benefits or perquisites is not offered to tax by the recipients.

Any other possible implications.

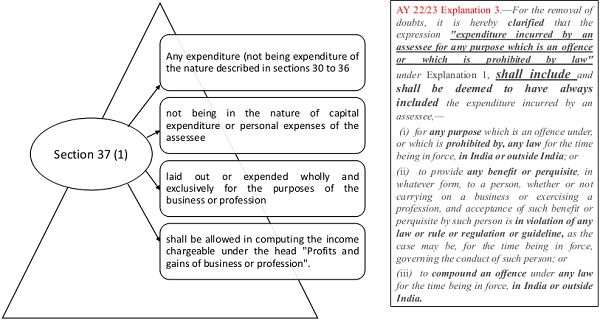

Correlations with Section 37(1) – General deduction under PGBP

TDS applicability u/s 194R vis-à-vis u/s 37(1)

Questions

Suggested Answers

If Taxpayer has violated the provisions of Section 37(1) by providing any benefits or perquisite as contemplated u/s 194R of the Income Tax Act, 1961 under any other law applicable to business enterprise & such Taxpayer has deducted TDS, deposited TDS and complied with all the applicable provisions as envisaged, whether still the disallowance u/s 37 would survive?

If Taxpayer has provided any benefit or perquisite as contemplated u/s 194R to any of its customers or stakeholders in general which is not violation of provisions of Section 37(1), then whether disallowance u/s 37 would trigger?

Disallowance u/s 37 would survive if any such benefit or perquisite is given contrary to any provisions applicable under any law even though Taxpayer has deducted TDS u/s 194R and compiled with all the applicable provisions.

Such disallowance would be detrimental to ease of doing business as Taxpayer needs to disallow such expenses while determining total income u/s 28 of the Income Tax Act 1961 and deduct TDS also. Such situation can be termed as double whammy viz. payment of tax due to disallowance & payment of TDS due to providing of such benefit or perquisite.

If Taxpayer has provided any benefit or perquisite as contemplated u/s 194R to any of its customers or stakeholders in general which is not violation of provisions of Section 37(1), then in my understanding disallowance u/s 37 would not trigger. Only time will prove that whether such view sustains by as waters gets tested, probably involving litigations For e.g.

In case of Pharma companies, if such benefit or perquisites provided to doctors or group of hospitals which do not contravene the provisions as formulated by MCI considering regulatory contours of medical practice, then such provision of benefits or perquisite may not trigger the disallowance u/s 37.

Conclusions

With the ever expanding scope of TDS and TCS provisions under the provisions of the Act, whether TDS and TCS would emerge as separate tax compliance & code by itself when compared to Income Tax Act provisions as a whole???? ( Set Theory)

Whether such provisions would ease the compliance, reduce the burden of Taxpayers and it would promote the atmosphere of ease of doing business ????

Whether such provisions would reduce the tax litigations in general ????

Whether such regulatory initiatives satisfy the tenets of taxation to be in line with international taxation systems? Whether they will catalyze or impede the pace of development of our economy which has the “ease of doing business” as a foundational pillar????

Last but least, is there urgent need to provide more suitable clarifications and/or provide guidance for valuation mechanism in the overall interests of all the stakeholders???? Or whether such provisions needs to be deferred further for smooth and effective implementations by couple of months????

I have just tried to share my views as novice on the vital subject which concerns all the stakeholders in general on 74th Chartered Accountants Day as well as Doctors day on July 1,2022 as all professionals are also doctors for their clients, friends and associates in general.

***

Disclaimer: All views stated are my personal views, they are not binding on ICAI/Study Circle. My personal views may be correct/incorrect as they are expressed based on my understanding of the subject. All members/listeners are requested to go through tax law provisions on their own and advise their clients accordingly as each situation is peculiar in itself. All Illustrations provided are imaginary and any resemblance to any situation/s is purely co-incidental and without any intentions to disclose private and confidential information.