What is short stay exemption?

As the name suggests, short stay exemption is leeway given to resident individuals staying for short term in overseas country. Short stay exemption is available to an individual being resident of a country, staying in overseas country for less than 183/90 days during a tax year. Such an exemption is subject to fulfillment of certain other conditions and has to be considered with possible corporate tax implications arising on the Indian employer. The exemption can be claimed by Inbound expats in India and Outbound expats in Host country. Needless to say that such exemption can be claimed by the expats on short term assignment only (short term duration depends on treaty between countries under question, generally upto 183 days for employed individual and 90 days for contractual individuals)

Since short stay exemption is captured in Double tax treaty between countries, we shall consider the DTAA between India and UK for purpose of understanding the same.

Need for Short stay exemption

Having understood the meaning of exemption, one may face question as to its importance.

Consider a situation where Mr. John an individual resident of UK has come to India on employment contract and stays for period of 150 days in FY 2021-22. Following are the notable points in this regard.

- His stay in India is less than 183 days thus he shall become Non-Resident in India for the taxation purposes for FY 2021-22.

- Now as per section 9(1)(ii), salary income earned in India is taxable for all residential status. Thus the same is taxable in India for Mr. John.

- Since Mr. John is resident in UK, his Indian sourced income would also become taxable in UK. This would lead to situation of double taxation for him.

Here arises need for providing relief to such person paying taxes in 2 different jurisdictions for same income.

In this situation there are 2 possible solutions offered by DTAA

- Article 16/17

- Article 24

Article 16 (Dependent personal service) of India-UK DTAA provide relief to Mr. John staying in India for a short period. As per the DTAA short period is defined as 183 days for employment (Dependent personal service) and 90 days for contractual services (Independent personal service). Where the stay of employee is not exceeding 183/90 days in FY, Article 16/17 play into picture and exempts such salary from being taxed in India provided other conditions of articles are complied with. While if the stay exceeds 183/90 days then article 24 comes into play and provides tax credit in UK (residence country) for the taxes paid in India (source country). One may note an important difference that Article 16/17 allows the income to not to be taxed in Source country while Article 24 allows credit of taxes to be claimed later in Residence country.

Legal Statute

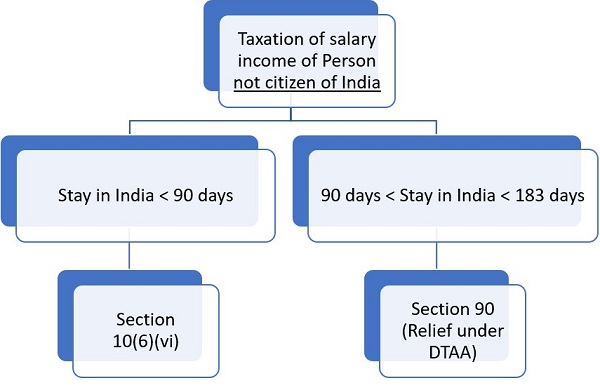

Income Tax Act 1961 – Such short stay exemption is available under the Act through Section 10(6)(vi) for the individual who is not a citizen of India. The remuneration received by him/ her as an employee of a host country entity, for services rendered by him/ her during his/ her stay in India is exempt from tax subject to fulfillment of all the following conditions:

1. The foreign enterprise is not engaged in any trade or business in India;

2. His/her stay in India does not exceed in the aggregate a period of 90 days in such previous year; and

3. Such remuneration is not deductible from the income of the employer chargeable under the Act

DTAA – As per the DTAA, the exemption gets power from Article 16 Dependent Personal Services. The short stay exemption can be claimed for individual resident of a country derives remuneration from employment exercised in other country if:

1. The recipient is present in the source country for a period or periods not exceeding in the aggregate 183 days in the relevant fiscal year;

2. The remuneration is paid by, or on behalf of, an employer who is not a resident of the other state;

3. The remuneration is not borne by a permanent establishment or a fixed base or a trade or business which the employer has in the other State.

It is imperative to note that the exemption can be claimed only if stay of employee in India is less than 183 days, his remuneration is paid by the entity who is non-resident of Host country and remuneration paid to such employee is not deductible while computing business profits chargeable to tax in Host country.

While deliberating the short stay exemption one may also note judgement of Madras High court in CIT Vs R Rajgopal that if salary is paid directly by Host country subsidiary company to employee then exemption cannot be claimed by employee even though the salary of employees is charged by host country company to home country. Point 2 above ensures income is being taxed in home country to claim short stay exemption in India. Thus if salary is paid directly by Host country subsidiary company to employee then exemption cannot be claimed by employee, rather complete income shall be subject to tax in India.

Example- Mr. John is UK based Geologist (resident of UK) and derives salary income in India for imparting geological services. He stays in India every year for 100 days, in year 2021-22 he stays in India for a period 12 Aug 2021 to 15 Nov 2021. Remuneration for the said period is $ 15000.

Taxability: Since Mr. John is resident in UK, his Indian income will be taxable in UK based on his residential status. The income becomes taxable in India as it is source country for the income, leading income to be doubly taxed in India and in UK.

One must note that since Mr. John stays in India for more than 60 days in current year and 365 days in last 4 years, he shall become resident in India.

Relief for such double taxation can be found in DTAA between India and UK u/s 90. Article 16 of the DTAA – Dependent Personal service clause, states that the income earned by resident of UK and derived from India may be taxed in India if employment is exercised in India. However, it shall not be taxed in India if all of the following conditions are fulfilled:

1. He is present in India of period less than 183 days- in instant case, Mr. John is present in India for less than 183 days in FY 2021-22

2. Remuneration is paid by employer who is not resident in India.

3. Remuneration paid to John is not deduction while computing income under the Act in India.

If all the above conditions are fulfilled, Mr. John may claim short stay exemption under section 90 of the Act. It is always advisable to obtain Tax Residency Certificate of the employee claiming short stay exemption benefit

Point to ponder – Whether person claiming benefit of short stay exemption is required to file tax Return?

Opinion- Yes. As per sec 139, total income of assessee exceeding threshold limit needs to file tax return. When a person claims the benefit of a DTAA, that person is invoking section 90(2) to do so. In other words, a person, earning an income that is chargeable to tax under the Act, has to make a claim by invoking section 90(2) for getting the benefit of a DTAA. So, even if he would be entitled to seek relief under the DTAA, he has to seek it and that would be during the consideration of his return of income or at best while filing his return. If so, the obligation under section 139 cannot simply disappear merely because a person may be entitled to claim the benefit of a DTAA. Thus obligation to file tax return cannot be negated in such case.

The Author of this article is a Chartered Accountant with M/s. Venu & Vinay and can be reached at navodita@vnv.ca

Author Bio

Madam,

I am reading your articles which helps me enhance my knowledge. Request if you can keep sharing on my email

Deepakasopa @westcoastpaper.com

deepak.asopa @gmail.com

Sure, will keep you updated