What are per diems?

Per diems are daily allowance provided to employees on business trips. They can be provided for meeting personal or official expenses while on business trip. As a business practice, companies available globally generally send their local employees overseas for project based work (short term or long term)

The salaries of employees are determined on basis of laws of local land and the inflationary factors. Generally the employees sent on overseas assignment but are on payroll of home country (short term deputation), while if the project is long term then company may decide for shifting of payroll from home country to host country. Usually per diems are provided when payroll is maintained in home country while employee is performing duty from host country, to meet the cost of living.

Types of per diems

As a business practice across the globe, there are 2 types of per diems provided to employees;

- Allowance granted to meet the official expenses. These allowance are provided by employer for employee to meet the expenses in performance of official duty.

- Allowance to meet personal expense while on overseas assignment. These allowances are provided by employer to meet the cost of living of employees according to foreign land.

Taxability of per diems

The taxability of per diem would of course depend on basic parameters of taxation of Residential status. As per Section 14, the incomes under section 2(24)(iiia) are divided in 5 heads. Any income earned due to the employee-employer relationship is considered as income under the salary. Thus per diems provided by employer to employee as part of employment, will become part of Income under the head Salary.

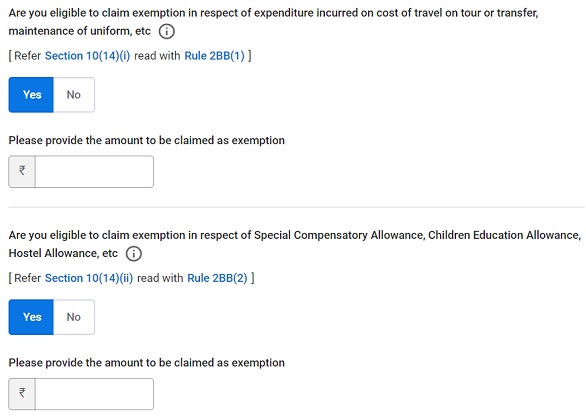

The Allowances provided to employee for meeting the official expenses are completely exempt if expended [u/s 10(14)(i) read with Rule 2BB(1)]. The intent of law is to tax genuine income of taxpayer, if some allowance are being provided by the employer to employee and they are spent then usually they are exempted from tax subject to reasonableness of the allowance. Since these allowance are expended by the employee for accommodating in place different from regular place of duty, they shall not form part of total income. These allowances are generally provided for meeting cost of tour or travel, daily charges, conveyance expenses, helper allowance, research allowance and uniform allowance.

Per diems provided by employer to meet the personal expenses are exempt to the extent of amount received or amount prescribed under Rule 2BB(2) whichever is lower.

It must be noted that allowance provided for performance of official duty are completely exempt if expended, while allowance provided to meet personal expense are completely exempt if within the limit prescribed under Rule 2BB(2).

In certain cases, the per diems are not completely spent but are saved. Such saved amount shall be taxed as Salary income and be declared to Tax authorities.

How to avail the exemption?

The per diems allowed (paid) by employer needs to be added in gross salary as part of Salary under Section 17(1) as shown in screen below:

1. Amount needs to be entered while answering the Salary Exemption questions (Under Salary head) (Pls see the attachment)

2. Since part or complete amount is to be claimed exempt under section 10(14)(i)/ 10(14)(ii). Per diems amount received from employer (whether exempt or not) needs to be added as part of Salary under section 17(1) and then reduced by entering the same under exemptions u/s 10. This can be explained with help of an example.

Let us understand this with an example.

Mr. Ram is an Indian Citizen, going to UK on short term assignment of 2 months. His payroll is maintained by Indian company, i.e. Home country company while he will be rendering services to UK subsidiary of the Indian company. Salary in India comprises of:

| Basic pay @ ₹ 90,000 per month (90,000 x 12) | 10,80,000 |

| HRA (50% of basic) | 5,40,000 |

On deputation to UK, he is in receipt of GBP 50 daily as per diems for meeting cost of living (also known as Cost of Living Allowance- COLA) and GBP 4000 monthly conveyance allowance.

Mr. Ram on completion of his assignment utilizes completely conveyance allowance. While he brings back GBP 2460 India at the end of assignment.

In above case, the amount of conveyance allowance since spent thus exempt u/s 10(14)(i) read with Rule 2BB(1). The daily allowance for meeting cost of living received by employee is (GBP 50 x 60 days) GBP 3000 out of which GBP 2460 is brought back by him to India. The amount to be included in his income u/s 17(1) shall be GBP 3000 converted at SBI TTBR last day of the month immediately preceding the month in which the salary is due, or is paid in advance or in arrears as per Rule 115. And the amount GBP 580 (spent per diems) are to be reduced, effectively GBP 2460 will become part of income.

Frequently Asked Questions

Q1. Is there separate ITR form for claiming benefit of Section 10?

No, the ITR forms available for salaried individuals are ITR-1 and ITR-2 generally. In the same form once can claim the benefit.

Q2. Is Section 10(14)(i)/(ii) benefit available to Residents only?

No, the benefit is available to all irrespective of residential status.

Q3. How can one claim benefit of exemption u/s 10?

The benefit of exemption can be claimed while filing the return. In case income of individual falls below the basic exemption limit after claiming exemption u/s 10, the assess may still chose to file the return. It is always advisable to file the income tax rerun if income exceeds basic exemption limit.

Q4. Can the benefit be claimed if payroll is maintained in host country?

The allowance is provided to employee to compensate the locational challenges. In case payroll is shifted to host country then the same would be updated to meet the locational requirement thus one may not find Per diems component in payroll which is host based.

The Author of this article is a Chartered Accountant with M/s. Venu & Vinay and can be reached at navodita@vnv.ca

Author Bio

if an employee denies submitting the breakup of expenses incurred with supporting for the per-diem allowance availed from the company and will it be ok if an employee shares the self-declaration to the employer stating what amount spent and what amount brought back to India. will it be ok for the employer to consider as per the declaration?

Whether a employee getting per diem needs to submit bills

If perdiem is paid for local travel in the country of residence. What are the rules for the applicability of taxation.

In the example given what would be the position on taxability if the balance amount of GBP 2640 is spent outside india for personal purpose & money is not brought back to india.

Generally an employee needs to report to employer what all amount is spent along with supporting proofs. If the amount is spent for the purpose for which it was granted and employer approves of bill then the the same is exempted u/s 10(14). If GBP 2640 is spent outside India and bills are submitted to employer which are approved by him, the same is not taxable.

The thumb rule should be that if amount is brought back to India, then the same would become taxable