Sheetal Clothing Company Pvt. Ltd. Vs DCIT (ITAT Mumbai)

For AY 2017-18, the Assessing Officer issued notice under section 148 on 29.07.2022 after passing an order under section 148A(d) on the same date, alleging unexplained unsecured loans of about ₹72.97 lakh. This was clearly more than three years after the end of the assessment year (which ended on 31.03.2018, so the three-year period expired on 31.03.2021).

Under the post-2021 reassessment regime, where notice is issued after three years and the alleged escaped income exceeds ₹50 lakh, prior sanction must be obtained from the higher authority specified in section 151(ii), i.e., the Principal Chief Commissioner/Chief Commissioner (Pr. CCIT/CCIT). However, in this case approval was taken only from the Principal Commissioner of Income-tax (Pr. CIT-5, Mumbai).

Relying heavily on the Supreme Court decisions in Ashish Agarwal and especially Rajeev Bansal, the Tribunal held that after 01.04.2021 approvals must strictly comply with section 151 of the new regime, and TOLA only extends time limits, not the level of approving authority. Thus, once three years had elapsed, sanction by Pr. CIT was insufficient and jurisdictionally defective.

Following these binding principles and also the Bombay High Court rulings in Ramesh Bachulal Mehta and Alag Property on identical facts, the Tribunal held that absence of approval from the correct specified authority under section 151(ii) rendered the notice under section 148 void ab initio.

Consequently, the entire reopening and the reassessment order were quashed on this pure jurisdictional defect, and since the reassessment itself failed, issues on merits were left unexamined.

The assessee’s appeal was allowed in full.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

This appeal filed by the assessee is against the order of National Faceless Appeal Centre (NFAC), Delhi, vide order no. ITBA/NFAC/S/250/2025-26/1079774938(1), dated 20.08.2025, passed against the assessment order by Assessment Unit Income Tax Department, u/s. 147 r.w.s 144B of the Income-tax Act (hereinafter referred to as the “Act”), dated 27.05.2023 for Assessment Year 2017-18.

2. Grounds taken by the assessee are reproduced as under:

1. On the facts and circumstances of the case and in law, the Ld. CIT(A) has erred by dismissing the appeal filed by the appellant and upholding the assessment order passed by the Ld. A.O. u/s 147 r.w.s 144B of the I. T. Act 1961 since the same is grossly incorrect, invalid and bad in law

2. On the facts and circumstances of the case and in law, the Ld. A.O. has erred in obtaining the approval for issuance of notice u/s 148 of the Income Tax Act, 1961 from the Hon’ble Pr. CIT-5, Mumbai, u/s 151(i) of the Act. whereas, as per the statutory requirement, the approval ought to have been obtained from Honorable Pr. CCIT under section 151(ii) of the Act. The failure to obtain valid and proper sanction renders the reassessment proceedings and the notice issued under section 148 as invalid, bad in law, and liable to be quashed. Reliance is placed on the decision of Honorable SC in case of UOI vs. Rajeev Bansal, [2024] 167 taxmann.com70 (SC).

| Sr. No. | Particulars | Remarks |

| 1 | AY under consideration | AY 2017-18 |

| 2 | Whether TOLA Applicable | Yes (Since 1st notice u/s 148 was issued on 26/06/2021 and subsequently treated as 148A (b) as per decision of UOI vs. Ashish Agarwal) |

| 4 | Amount of Income Escaping Assessment | Rs. 72,97,080/- |

| 5 | Last date to issue notice u/s 148 as per decision of Hon’ble SC in case of UOI vs Rajeev Bansal | 10/06/2022 ( As per case of UOI vs. Rajeev Bansal and extended time given as per fourth Proviso to section 149(1) |

| 6 | Notice u/s 148 issued on | 29/07/2022 (after a period of 3 years) |

| 7 | Approval taken u/s 151 for issuing notice u/s 148 | Pr. CIT-5, Mumbai |

| 8 | Approval required u/s 151 for issuing notice u/s 148 | Pr. CCIT |

The appellant also relies on the following judicial decisions.

-

- Lalit Garg vs. DCIT CC, 6(2), Mumbai, ITA 6125 & 6126/MUM/2024 (Mumbai Trib.)

- Ramlal Suthar vs. ITO, ITA-3224/MUM/2024 (Mumbai Trib.)

- ACIT vs. Surya Ferrous Alloys Pvt Ltd, ITA 1406/MUM/2024 (Mumbai Trib.)

- Ashok Amratlal Shah vs ITO, ITA 4287 & 4288/MUM/2024 (Mumbai Trib.)

- ACIT vs. Ramchand Thakurdas Jhamtani, ITA 3551/MUM/2024 (Mumbai Trib.)

3. On the facts and circumstances of the case and in law, the Ld. J.A.O. has erred by initiating the Inquiry Proceedings u/s 148A of the I. T. Act, 1961 since the same was to be conducted in faceless manner and therefore, the notice issued u/s 148 of the I. T. Act, 1961 is bad in law. The appellant relies on the decision of Hon’ble Bombay High Court in case of M/s Hexaware Technologies Ltd vs. ACIT, Circle 15(1)(2).

4. On the facts and circumstances of the case and in law, the issuance of notice u/s 148 of the Act and making reassessment u/s 147 of the Act is bad in law, invalid and void ab initio, as there is no income escaped in case of the appellant and disturbing the finding of completed assessment is purely a case of change of opinion and against the principals propounded by the Hon’ble Apex Court in the matter of Kelvinator of India (320 ITR 561), since already detailed scrutiny was done and an assessment order was passed-u/s 143(3) of the IT Act. 1961 in case of the appellant on 28/12/2018.

5. On the facts and circumstances of the case and in law, the L.d. A.O. has erred by making addition of Rs. 72,97.080/- u/s 68 of the IT Act, 1961 treating the same as unexplained money bought into balance sheet in the form of unsecured loans without considering the facts and circumstances of the case and with a preset mind of making addition on assumption and presumption basis.

6. On the facts and circumstances of the case and in law. the Ld. A.O. has erred by not providing cross-examination to the assessee before passing the reassessment order u/s 147 r.w.s 144B of the I. T. Act, 1961.

7. The appellant craves leave to add, alter, amend or modify any or all grounds till the disposal of the Appeal.

3. Ground No.1, 2 and 3 are in regard to jurisdictional issues raised by the assessee for the reassessment proceeding initiated u/s. 148 and reassessment order passed thereafter.

4. Brief facts of the case are that assessee filed its return of income originally u/s.139(1) on 27.10.2017, reporting total income at Rs.7,37,520/-. Scrutiny assessment was completed u/s. 153A r.w.s. 144 with assessed total income at Rs.3,76,39,220/-. The information which led to investigation proceedings u/s. 148 as noted by ld. Assessing Officer are that assessee had borrowed a sum of Rs.2,34,47,080/- during the year under consideration. On going through the case records, it was noted that reply to notices u/s. 133(6) were received from only two borrowers i.e., Mangal Credit and Zapata Fashions for an amount of Rs.36,50,000/- out of Rs.2,34,47,080/-. According to the ld. Assessing Officer, assessee had not proved the identity and creditworthiness of the loan creditors and genuineness of the loan transactions in respect of the balance amount of Rs. 1,97,97,080/- which was thus, required to be added u/s.68 as against original addition of Rs.85,47,080/- only.

4.1. Reasons to believe were recorded for initiating the reopening of proceedings and issuance of notice u/s.148, which was issued on 26.06.2021, placed in the paper book at page 1. Since this notice was issued under the erstwhile regime of re-assessment as provided u/s.148 r.w.s. 147 which has undergone total revamp by the Finance Act, 2021, the amendments brought in by the Finance Act 2021 led to several jurisdictional issues in respect of reassessment proceeding for which the matter travelled up to the Hon’ble Supreme Court with the lead case of Union of India vs. Ashish Agarwal [2022] 130 taxmann.com 64 (SC) followed by the decision in the case of Union of India vs. Rajeev Bansal [2024] 167 taxmann.com 70 (SC). As a fall out of the directions given in the case of Ashish Agarwal (supra), ld. Assessing Officer in the present case complied with the same, after which an order u/s.148A(d) was passed dated 29.07.2022 recommending the reopening of the case u/s.148. Subsequent to this, notice u/s.148 was issued, dated 29.07.2022.

4.2. Chronology of events which took place in the present case for which the relevant material is on record is tabulated below for ready reference:

| Sr. No. | Particulars | Remarks |

| 1 | AY under consideration | AY 2017-18 |

| 2 | Whether TOLA Applicable | Yes (Since 1st notice u/s 148 was issued on 26/06/2021 and subsequently treated as 148A (b) as per decision of UOI vs. Ashish Agarwal) |

| 4 | Amount of Income Escaping Assessment | Rs. 72,97,080/- |

| 5 | Last date to issue notice u/s 148 as per decision of Hon’ble SC in case of UOI vs Rajeev Bansal | 10/06/2022 ( As per case of

UOI vs. Rajeev Bansal and |

| 6 | Notice u/s 148 issued on | 29/07/2022 (after a period of 3 years) |

| 7 | Approval taken u/s 151 for issuing notice u/s 148 | Pr. CIT-5, Mumbai |

| 8 | Approval required u/s 151 for issuing notice u/s 148 | Pr. CCIT |

5. We have heard both the parties on their submissions relating to legal ground. We have also perused the judicial precedents relied upon for which relevant judicial orders are placed on record. Merits of the case have not been argued upon by either party, nor any submission made to that effect. An order u/s. 148A(d) was passed by Income Tax Officer, Ward-5(3)(1), Mumbai, dated 29.07.2022 recommending the re-opening of the case u/s. 148. Subsequent to this, a notice u/s.148 was issued on 29.07.2022 wherein, in para-3, it is noted that prior approval of PCIT-5, Mumbai, vide letter No.Pr.CIT-5(HQ)/Approval-148A(d)/2022-23, dated 27.07.2022 was obtained.

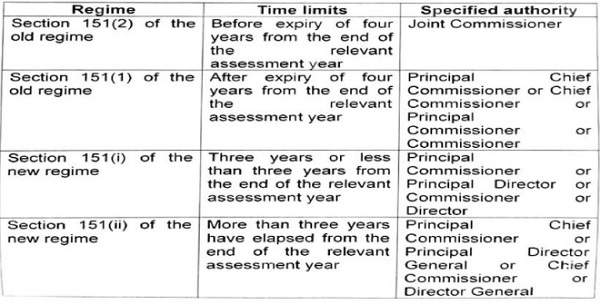

6. On these set of facts, submission of the ld. Counsel is that in the provisions for re-opening of assessment upon amendment by Finance Act, 2021, the first proviso to section 148 refers to approval by specified authority which is to be obtained before issuing notice u/s. 148. Section 151 describes specified authority for the purpose of section 148 and 148A, based upon the time limits within which the reopening proceedings are to be initiated i.e.,

i. By Principal Commissioner of Income Tax or Principal Director or Commissioner or Director, if three years or less than three years have lapsed from the end of the Assessment Year.

ii. By Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General, if more than three years have been lapsed from the end of the relevant Assessment Year.

7. Admitted position of fact in this case is that income chargeable to tax which escaped assessment is more than Rs.50,00,000/-, since ld. Assessing Officer has alleged that the income chargeable to tax of Rs. 72,97,080/- has escaped assessment. Also, it is undisputed that notice u/s.148 has been issued after the expiry of three years from the end of the relevant Assessment Year. Three years from the end of the Assessment Year 2017-18 lapsed on 31.03.2021. As per section 149(1)(b) of the Act (new regime), re-assessment proceedings could have been initiated after the expiry of three years from the end of the relevant Assessment Year only if the income chargeable to tax which escaped assessment is more than Rs.50,00,000/-. These admitted facts are relevant on the legal aspect relating to obtaining prior approval from the specified authority which are undisputed and nothing has been brought on record by the Revenue to controvert the same.

7.1. We find that in the decision by the Hon’ble Supreme Court in the case of Union of India v. Rajeev Bansal (supra), Hon’ble Court after the fall out of its own decision in the case of Ashish Agarwal (supra) had dealt with the issue in respect of sanction of the specified authority and concluded that TOLA will extend the time limit for the grant of sanction by the authority specified u/s.151. According to the Hon’ble Court, the test to determine whether TOLA will apply to section 151 of the new regime is that if the time limit of three years from the end of the Assessment Year falls between 20.03.2020 and 31.03.2021 then, the specified authority u/s.151(i) has extended time till 30.06.2021 to grant the approval. According to the Hon’ble Court, Assessing Officers were required to issue the re-assessment notice u/s.148 of the new regime within the time limit surviving under the Act read with TOLA. All notices issued beyond the surviving period are time barred and liable to be set aside. Hon’ble Court had elaborately dealt with this issue in Part E of its decision in para 73 to 78 which are extracted below:

73. Section 151 imposes a check upon the power of the Revenue to reopen assessments. The provision imposes a responsibility on the Revenue to ensure that it obtains the sanction of the specified authority before issuing a notice under Section 148. The purpose behind this procedural check is to save the assesses from harassment resulting from the mechanical reopening of assessments. 128 A table representing the prescription under the old and new regime is set out below:

74. The above table indicates that the specified authority is directly co-related to the time when the notice is issued. This plays out as follows under the old regime:

(i) If income escaping assessment was less than Rupees one lakh: (a) a reassessment notice could be issued under Section 148 within four years after obtaining the approval of the Joint Commissioner, and (b) no notice could be issued after the expiry of four years; and

(ii) If income escaping was more than Rupees one lakh: (a) a reassessment notice could be issued within four years after obtaining the approval of the Joint Commissioner; and (b) after four years but within six years after obtaining the approval of the Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner.

75. After 1 April 2021, the new regime has specified different authorities for granting sanctions under Section 151. The new regime is beneficial to the assessee because it specifies a higher level of authority for the grant of sanctions in comparison to the old regime. Therefore, in terms of Ashish Agarwal (supra), after 1 April 2021, the prior approval must be obtained from the appropriate authorities specified under Section 151 of the new regime. The effect of Section 151 of the new regime is thus:

(i) If income escaping assessment is less than Rupees fifty lakhs: (a) a reassessment notice could be issued within three years after obtaining the prior approval of the Principal Commissioner, or Principal Director or Commissioner or Director; and (b) no notice could be issued after the expiry of three years; and

(ii) If income escaping assessment is more than Rupees fifty lakhs: (a) a reassessment notice could be issued within three years after obtaining the prior approval of the Principal Commissioner, or Principal Director or Commissioner or Director; and (b) after three years after obtaining the prior approval of the Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General.

76. Grant of sanction by the appropriate authority is a precondition for the assessing officer to assume jurisdiction under Section 148 to issue a reassessment notice. Section 151 of the new regime does not prescribe a time limit within which a specified authority has to grant sanction. Rather, it links up the time limits with the jurisdiction of the authority to grant sanction. Section 151(ii) of the new regime prescribes a higher level of authority if more than three years have elapsed from the end of the relevant assessment year. Thus, non-compliance by the assessing officer with the strict time limits prescribed under Section 151 affects their jurisdiction to issue a notice under Section 148.

77. Parliament enacted TOLA to ensure that the interests of the Revenue are not defeated because the assessing officer could not comply with the pre- conditions due to the difficulties that arose during the COVID-19 pandemic. Section 3(1) of TOLA relaxes the time limit for compliance with actions that fall for completion from 20 March 2020 to 31 March 2021. TOLA will accordingly extend the time limit for the grant of sanction by the authority specified under Section 151. The test to determine whether TOLA will apply to Section 151 of the new regime is this: if the time limit of three years from the end of an assessment year falls between 20 March 2020 and 31 March 2021, then the specified authority under Section 151(i) has an extended time till 30 June 2021 to grant approval. In the case of Section 151 of the old regime, the test is: if the time limit of four years from the end of an assessment year falls between 20 March 2020 and 31 March 2021, then the specified authority under Section 151(2) has time till 31 March 2021 to grant approval. The time limit for Section 151 of the old regime expires on 31 March 2021 because the new regime comes into effect on 1 April 2021.

78. For example, the three years time limit for assessment year 2017-2018 falls for completion on 31 March 2021. It falls during the time period of 20 March 2020 and 31 March 2021, contemplated under Section 3(1) of TOLA.

Resultantly, the authority specified under Section 151(i) of the new regime can grant sanction till 30 June 2021…

81. This quote in Ashish Agrawal (supra) directed the Assessing Officers to “pass orders in terms of Section 148-A(d) in respect of each of the assessee concerned.” Further, it directed the Assessing Officers to issue a notice u/s.148 of the new regime “after following the procedure as required u/s.148-A.” Although this quote waived off the requirement of obtaining prior approval u/s.148A(a) and section 148A(b), it did not waive the requirement for section 148A(d) and section 148. Therefore, the Assessing Officer was required to obtain prior approval of the specified authority according to section 151 of the new regime before passing an order u/s. 148A(d) or issuing a notice u/s.148. These notices ought to have been issued following the time limits specified u/s.151 of the new regime r. w. TOLA, where applicable….

114.

.…d. TOLA will extend the time limit for the grant of sanction by the authority specified u/s.151. The test to determine whether TOLA will apply to section 151 of the new regime is this: if the time limit of three years from the end of an Assessment Year falls between 20 March 2020 and 31 March 2021, then the specified authority u/s.151(i) has extended time till 30 June 2021 to grant approval; …”

7.2. From the above, we note that in para 73, in the table last two rows relate to provisions of Section 151(i) and (ii) of the new regime prescribing the time limit as well as the specified authority. In para 75, it is very categorically mentioned by the Hon’ble Court that after 01.04.2021, in terms of Ashish Agrawal (supra) the prior approval must be obtained from the appropriate authorities specified u/s.151 of the new regime. This abundantly brings clarity on the aspect of obtaining approval for issue of notice u/s.148 which are fall out of the decision in Ashish Agrawal (supra). In para 77, objective of section 3(1) of TOLA is mentioned which is to relax the time limit for compliance with actions that fall for completion from 20.03.2020 to 31.03.2021. Thus, the objective is specific for providing temporal flexibility. In para 78, the same has been explained by an example taking Assessment Year 2017-18 which also in specific terms mentions that the authority specified u/s.151(i) of the new regime can grant sanction till 30.06.2021. Thus, while concluding in para 81 on the issue obtaining approval, Hon’ble Court has specifically stated that the Assessing Officer is required to obtain prior approval of the specified authority according to section 151 of the new regime before passing an order u/s.148A(d) or issuing a notice u/s.148. According to the Hon’ble Court, though it had waived off the requirement obtaining prior approval u/s.148A(a) and Section 148Ab, it did not waive the requirement for section 148A(d) and Section 148.

7.3. Taking into consideration the submissions made by both the sides and findings of the Hon’ble Court, we note that the issue we are presently addressing raised before us is not on the aspect of “when” for the procedural compliance for issuance of notice u/s.148 but on the aspect of “by whom” it ought to have been issued. Ld. DR has contended that there is hierarchical escalation vis-à-vis obtaining approval for issuing notice u/s.148. In this respect, Hon’ble Court has very categorically held in para 75 that the prior approval must be obtained from the appropriate authorities specified u/s.151 of the new regime for the notices issued in terms of Ashish Agrawal (supra) after 01.04.2021. Reference by ld. DR to Section 149(1)(a) deals with time limit for issuing notice u/s.148. Contention of the ld. Sr. DR that there is no hierarchical escalation for obtaining prior approval for issuing notice u/s.148 is not in coherence with the guidelines mandated by the Hon’ble Apex Court as enunciated above. Repeatedly, Hon’ble Court has stated including by way of illustration that TOLA extends time line from the old regime which survives making the notice validly issued subject to the approval requirements of Section 151 under the new regime. Accordingly, the prior approval requirement is mandated under the section 151 of new regime.

7.4. Thus, on the above stated facts and law, in the present case, three years had lapsed from the end of the Assessment Year when the order u/s.148A(d) and notice u/s.148 were issued on 29.07.2022. In the present case, since the notice u/s. 148 and order u/s. 148A(d) have been issued beyond the period of three years from the end of the relevant Assessment Year, case of the assessee falls within the provisions of section 151(ii) of the amended law whereby the specified authority for grant of approval is specified as Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General. Contrary to this requirement, the approval obtained is by Principal Commissioner of Income Tax-5, Mumbai. Accordingly, since a proper sanction by the specified authority had not been obtained for issue of notice u/s.148 under the applicable provisions of law, said notice is invalid and bad in law.

7.5. Keeping in juxtaposition the undisputed and the uncontroverted facts as stated above and the judicial precedent of the Hon’ble Supreme Court in the case of Ashish Agarwal and Rajiv Bansal (supra), we hold that sanction by specified authority has not been obtained by the ld. Assessing Officer in accordance with the provisions contained in section 151 of the Act under the new regime, since notice u/s.148 has been issued beyond three years from the end of the relevant Assessment Year. Accordingly, the said notice issued is invalid and thus quashed. Resultantly, the impugned re-opening proceedings so initiated and the impugned re-assessment order passed thereafter are also quashed.

7.6. We also find our force from the decision of Hon’ble Jurisdictional High Court of Bombay in the case of Ramesh Bachulal Mehta vs. Income Tax Officer [2025] 177 taxmann.com 606 (Bom) which dealt with similar issue on an identical fact pattern. Hon’ble Court held that “where re- assessment proceedings for Assessment Year 2016-17 were initiated after expiry of three years, from end of relevant year, approval u/s.151(ii) was mandatorily required from higher authority, i.e., Pr. Chief Commissioner/Chief Commissioner and sanction by Pr. Commissioner was not valid”. It thus, held that “order passed u/s.148A(d) and consequential notice issued u/s.148, dated 15.07.2022 were bad in law for being violative of provisions of section 151(ii).” Hon’ble Court gave similar findings in its decision in the case of Alag Property [2025] 179 taxmann.com 578 (Bom), dated 08.09.2025.

7.7. Since legal issue raised by the assessee is held in favour of the assessee, grounds raised on the merits of the case needs no separate adjudication.

8. In the result, appeal filed by the assessee is allowed.

Order is pronounced in the open court on 29 January, 2026