The Marwar GST Appellate Tribunal Bar Association submitted a detailed representation to the Hon’ble President of the Goods and Services Tax Appellate Tribunal highlighting practical difficulties faced by taxpayers and professionals in filing appeals on the newly launched GSTAT portal and concerns arising from the GSTAT (Procedure) Rules, 2025. While welcoming the commencement of tribunal operations and the initial six-month relaxation limiting scrutiny to substantive defects, the representation points out multiple procedural hurdles, including rigid portal declarations, mandatory selection of sections and rules even when absent in orders, duplication of information already available on the GST portal, and restrictions linked to payment before completing filings. It also questions high fees for interlocutory applications, mandatory certified copies despite digital availability, multiple overlapping certification requirements, compulsory English translations, restrictive rules on additional evidence, stringent procedures for changing authorised representatives, and ambiguity on matters involving place of supply being heard by the Principal Bench. The Association seeks clarifications, rationalisation, and alignment with CGST Rules to ensure ease of access, natural justice, and efficient dispute resolution.

MARWAR GST APPELLATE TRIBUNAL BAR ASSOCIATION

First Floor, Angira Bhawan, opp. Bombay Motor Service Station, Bombay Motor, Jodhpur— 342003 (Raj)

Email : marwargstat@gmail.com

Before the Hon’ble President,

Goods and Services Tax Appellate Tribunal,

New Delhi.

Sub: Representation on issues faced while filing of Appeal on GSTAT Portal and certain provisions under GSTAT (Procedure) Rules, 2025

Respected Sir,

Introduction of GST was a landmark in the process of reshaping of our country’s tax system, and the GST Appellate Tribunal now stands as a vital institution to ensure fairness and consistency in its implementation. The Tribunal will give taxpayers a trusted forum to resolve disputes and strengthen confidence in the GST framework.

With filing of appeal already begun and hearings about to begin, this moment marks an important step forward, and it is fitting to acknowledge the significance of this commencement with optimism and respect.

The notification of the Goods and Services Tax Appellate Tribunal (Procedure) Rules, 2025 (hereinafter referred as “GSTAT (Procedure) Rules, 2025) has laid the foundation for a structured appellate process under GST.

To ease the transition in this initial phase, as a first step, it has been directed vide Office Order No. F.No. GSTAT/Pr. Bench/Porta1/125/25-26/2711-15/20/01/26 Dated: 20th January, 2026 (hereinafter referred as “office order”) that only substantive defects be raised for six months, ensuring appellants are not burdened by minor procedural issues. In addition, documents generated digitally through the GSTN system have been exempted from certification requirements, further simplifying compliance and reinforcing the Tribunal’s commitment to accessibility and fairness.

This representation of our intends to bring before your goodself various issues which are being faced while filing of Appeal on GSTAT Portal and also various issues relating to GSTAT (Procedure) Rules, 2025.

Representation about filing process on GSTAT Portal

1. Clarification regarding the filing process on the Portal-

The filing process is new and appropriate clarifications at this stage would allow correct filing and avoid notices later on. The intent of raising the issues is that although office order has been issued for first six months to consider only substantial defects but then clarifications issued initially will only help in ironing out the issues from the start.

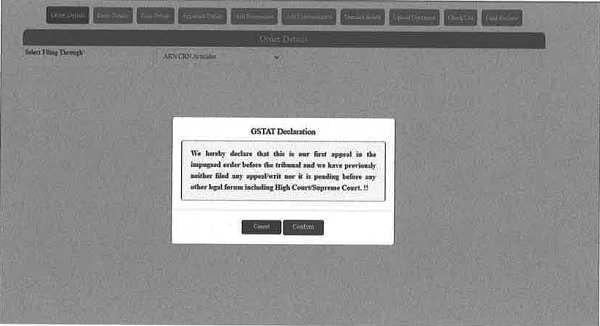

1.1. Undertaking about appeal before GSTAT being first appeal in the impugned order before the tribunal and previously appellant has neither filed any appeal/writ nor it is pending before any other legal forum including High Court/Supreme Court.

While ARN/CRN of the order is entered, portal does not allows to move further unless and undertaking is given on the portal that

“We hereby declare that this is our first appeal in the impugned order before the tribunal and we have previously neither filed any appeallwrit nor it is pending before any other legal forum including High Court/Supreme Court.”

The screenshot of the same is as follows-

It would not always be possible to give this undertaking and without giving the undertaking, the portal does not allows the appellant to move forward.

Supposedly, a taxpayer in absence of the tribunal had filed a writ petition before the High Court against the order of the Appellate authority and post constitution of tribunal, the matter is sent back by the high court, then in such case, it would not be possible for the appellant to give this undertaking.

Again, this undertaking in many cases would be acting as an hinderance and would either be resulting in appellant not able to file the appeal or giving incorrect declaration for the sake of filing of appeal.

Therefore, it is requested that the undertaking be suitably amended so that not only it achieves the objective it seeks to achieve but taxpayer is also not required to give an incorrect undertaking.

1.2. Clarifications for “Case Details” Tab on the portal for APL-05

1.2.1. Clarification about the scope of details to be provided in the tab relating to “Grounds of appeal in brief”, “Brief issue of the case under dispute” and “Prayer”

The portal requires the appellant to provide details of

a. Grounds of appeal in brief,

b. Brief issue of the case under dispute and

c. Prayer

These are mandatory fields on the portal. The appellant while preparing and submitting the appeal would also be providing these details as part of his appeal. The portal restricts the limit to 2000 characters but the portal also provides that “elaborate “grounds of appeal, prayer and brief issue of the case under dispute” can be uploaded as a document.

However, it is not coming out clear that

a. If all the details as required in the tab are available in the appeal being filed then can the appellant write and refer the relevant part of the appeal draft as “As per Para No….” of the Appeal Draft or statement of facts on the portal; or

b. If the details are not directly filled on the portal, then whether separate document other than the Appeal draft would invariably be required to be uploaded containing these details.

1.2.2. Clarification about the details to be provided in “Category of Case”

The portal requires that following details are required to be filled while filing the details

a. Category of case under dispute*

b. Select Gst Section*

c. Select Gst Rule*

d. Amount involved( In actuals)

There are about 38 drop downs from which the specific details are required to be filled. Out of the above, three details are mandatory i.e. Category of case under dispute, Select GST Section, Select GST Rules. There are multiple issues arising out the same which are as follows-

1.2.2.1. In case the relevant section or relevant rule has not been mentioned in the order-

It happens that against orders being passed, the primary ground in the appeal is that no relevant section is mentioned in the order or for that matter rule is rarely mentioned in the order.

For example, order has denied the credit of Input Tax Credit on account of the reason that incorrect place of supply is reflected in GSTR-2A and only mentions Section 16 of CGST Act, 2017 and does not mentions any rule. So how would the appellant be knowing that which is the relevant rule and in absence of the same how would the appellant mention the same. Further if any incorrect rule is mentioned by the appellant since the field is mandatory and primary ground of the appellant himself is the relevant rule being absent, isn’t the appeal itself be contrary to the details filled on the portal. It appears that the portal is asking the appellant to fill in the gaps which exist in the order passed and try to find out details which may never exist in the order itself.

Therefore, request you to kindly remove the requirement of mentioning the details as mandatory from the portal.

1.2.2.2. Certain fields of APL-05 on the portal are different from the form prescribed in the Rules

The form as prescribed in APL-05 in Annexure-B provides for

a. “Mention HSN” against Misclassification of any goods or services or both;

b. “Mention notification no. and date” in case of Wrong applicability of a notification issued under the provisions of this Act.

However, the form on the portal provides only for Select GST Section and Rule. There cannot be any GST Section and Rule for incorrect HSN or incorrect Notification No.

Therefore, we request your kind attention to not only this issue but if there any deviations from the prescribed form, the form on the portal may kindly be aligned in line with the same.

1.2.2.3. Clarification regarding cases wherein there are multiple issues arising out of the same ground then whether all such issues are required to be mentioned

This tab requires the appellant to mention the category of case under dispute and relevant sections and rule. The clarification is required in case where there are multiple issues arising out of an order and how the same have to be mentioned in this ground.

For the ease of simplicity, there is a case wherein appellant had treated the supplies as exempt under Entry No. 3 of Notification No. 12/2017 CT Rate Dated 28-06-2017 under HSN 99. The department alleges that the supplies were taxable at the rate of 18% under HSN 9954 and N. No. 11/2017 CT Rate Dated 28-06-2017. Department alleges Section 74 and also levies penalty under Section 122. There are multiple drop downs applicable on the same i.e.

a. Misclassification of any goods or services or both

b. Wrong applicability of a notification issued under the provisions of this Act

c. Incorrect determination of the liability to pay tax on any goods or services or both

d. Determination of tax not paid or short paid on outward supply u/s 73

e. Fraud or wilful suppression of fact leading to non-payment/short payment of tax determined u/s 74

f. Order imposing penalty

Now although these would be part of the appeal being filed, whether all these would still require to be filed on the portal respectively and what would be the relevant GST section and Rule in case where incorrect HSN and Rate is sought to be levied. There is a similar requirement while filing the appeal before Commissioner Appeals but then it only require the issue in dispute and not the relevant section and rule. Therefore, it is requested to kindly issue an appropriate clarification regarding this.

1.2.2.4. Clarification for “Case Summary Tab” about the mode of reporting and about details to be filled “As per stand of appellant before Tribunal” and “As declared/ claimed by present Appellant”.

In the “Case Summary” Tab on the portal following details are required to be provided

a. Issue related To*

b. As per order of adjudicating authority*

c. As determined by Appellate/Revisional authority*

d. As per stand of appellant before Tribunal*

e. As declared/ claimed by present Appellant*

At the outset, it is submitted that all these details would invariably be part of the appeal being filed. The portal restricts the limit to 2000 characters and however the portal provides that “elaborate “case summary” can be uploaded as a document. The issue is not pretty clear that

a. if all the details as required in the tab are available in the appeal being filed then can the appellant write and refer the relevant part of the appeal draft as “As per Para No….” of the Appeal Draft or statement of facts, or

b. If reference is to be made to the appeal being filed, then whether overall appeal form would be sufficient or the appeal has to contain specific tab for these details to be referred, or

c. If the details cannot be filled in the characters limit provided, then whether separate document would be required to be uploaded containing these details.

Further, supposedly there is levy of penalty under Section 122 of CGST Act, 2017 and the appellant challenges the same on account of multiple grounds i.e. lack of jurisdiction, power not being conferred by way of Circular No. 3/3/2017 Dated 5th July 2017, amount incorrectly quantified. Then in such case

a. whether these three grounds are required to be mentioned separately in these tabs as there separate case summary or one single mention would be sufficient,

b. whether the summary has to mention each of the relevant paragraph of the order of the adjudicating authority, appellate authority and appeal before the tribunal and

c. what if there is no discussion in the order of the adjudicating authority or appellate authority.

It is also requested to clarify the scope of “As per stand of appellant before Tribunal” and “As declared/ claimed by present Appellant”.

An early clarification in this regard would be helpful and avoid any confusion at the initial stages.

1.2.2.5. Details to be mentioned in “About Appellant” and all these being mandatory fields It is submitted that the following tab requires the appellant to mention as follows-

a. Constitution/Identification Number*

b. Constitution of Business*

c. Statute under which incorporated*

d. Date of Commencement of business*

e. Address*

f. Nature of Business*

g. Any other relevant fact*

All this information is ideally available with the department on GST Portal and can be fetched from the portal and could have been imported from the GST Portal. Requiring the same would be resulting in duplicity of the information.

It is requested to kindly allow the portal to auto-populate the same from the GST Portal and in case any person intends to change the same, then he may be allowed to so the same.

1.2.2.6. Details to be mentioned in case history

The case history tab requires the appellant to provide following details

The scope of the Statement of Fact case history isn’t very clear i.e. whether this tab only requires filing the details of only online generated documents or say supposedly summon has been issued and statements have been recorded then these documents are also required to be updated as recording of statement document does not have an acknowledgement no. There are replies filed manually which do not have any reference no., then what would be updated in the given case.

Further, since all these are already provided in the appeal being submitted, can this be referred as from the appeal document being submitted and uploaded as an attachment.

Request to provide a clarification about the same that so that not only appeals can be filed in a manner as deemed complete by the GSTAT (Procedure) Rules but also at the same time, it may not result in duplicity of information being filed by the taxpayer.

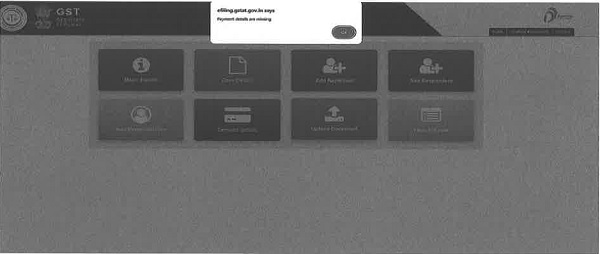

1.3. Portal does not allow the appellant to access the “Upload Document”, “Checklist” and “Final Preview” without the payment details being updated

At present, if the appellant intends to move to the tabs of “Upload Document”, “Checklist” and “Final Preview” without the payment details being updated, then the portal does not allows to do so. It appears that there is a restriction that unless payment tab is updated, next tabs would not be allowed to be filled.

The appellant shall be allowed to access the tabs post the payment details, even if the payment details are pending. By this way, portal is restricting the access. It might happen many times that taxpayer would not be available for making the payment and authorized representative of the taxpayer would prefers to finish everything else and keep the appeal pending for payment. This restriction only creates unintended hardship in filing of the appeal.

The checklist on the portal as required to be filled in itself is a very detailed one and allowing the same to be filled only when the payment has been made is a restriction which needs reconsideration.

There are many attachments which are to be uploaded with the Appeal and if those would only be allowed when the payment is made, this would not help in any manner in ease of filing of Appeal.

The final preview, if allowed to be generated even before making the payment will only allow filing of appeal in an error free manner because the same can be checked for errors well before filing.

Therefore, it appears that linking all these things to payment needs reconsideration and the ultimate check can be put at the time of uploading that whether due payment has been made.

Representation about GSTAT (Procedure) Rules, 2025

2. Request to reconsider fee of Rs 5000/- for filing of application for stay, rectification in order, condonation of delay, early hearing or extension of time prayed for in pending matters

2.1. Issue regarding fees being prescribed for filing of application for stay, rectification in order, condonation of delay, early hearing or extension of time prayed for in pending matters Rule 29 of the GSTAT (Procedure) Rules, 2025 states that every interlocutory application for stay, direction, rectification in order, condonation of delay, early hearing, exemption from production of copy of order appealed against or extension of time prayed for in pending matters shall include all the information as per the prescribed GSTAT FORM-01 and the requirements prescribed in that behalf shall be complied with by the applicant, besides filing an affidavit supporting the application.

As per Rule 119(2) of the GSTAT (Procedure) Rules, 2025, it has been provided in respect of every interlocutory application, there shall be paid fees as prescribed in Schedule of Fees of these rules.

Even an early hearing application or extension of time prayed for in pending matters is covered as “interlocutory application, therefore , it would have to be accompanied with a fees of Rs 5000. The present fees of Rs 5000/- per application may kindly be reconsidered. On the contrary, no fee is payable on a petition or application filed or reference made by any departmental authority connected with a matter in question before the Appellate Tribunal.

2.2. Fees being prescribed going beyond the provisions of CGST Rules which provide that there shall be no fees for rectification of orders

That as per Proviso to Rule 110(5) of CGST Rules, 2017, there shall be no fee for application made before the Appellate Tribunal for rectification of errors referred to in sub-section (10) of section 112. However as per Rule 29 of the GSTAT (Procedure) Rules, 2025 every interlocutory application for rectification in order needs to be accompanied with the fees prescribed of Rs 5000.

2.3 Inspection Fees being prescribed by GSTAT (Procedure) Rules, 2025 wherein there was no such fees for Inspection before CESTAT (Procedure) Rules, 1982

In addition to the above, as per CESTAT (Procedure) Rules, 1982, there was no fees charged for inspecting the records of a pending appeal or application by a party thereto. However, as per Rule 67 of the GSTAT (Procedure) Rules, 2025, fees for inspection of record has been provided at Rs 5000.

2.4.Request for reconsideration

It appears that the provision needs to be considered on some of the applications i.e. application for extension of time in pending matters appears to be and, in some cases, appears to be too high if at all it has to be levied.

3. Rule 21(1) and (2) of GSTAT (Procedure) Rules, 2025 goes beyond Rule 110(4) of CGST Rules 2017 and lays down a separate (Procedure) for filing of certified copy (that too excluding self-certified copy) irrespective of order being uploaded on portal or not

3.1. Date of issuance of Final Acknowledgement as per Rule 110 of CGST Rules, 2017 The relevant extract of the Rule is as follows-

(4) Where the order appealed against is uploaded on the common portal, a final acknowledgement, indicating appeal number, shall be issued in Part B of FORM GST APL-02A on removal ofdefects, f any, and the date of issue of the provisional acknowledgement shall be considered as the date of filing of appeal under sub-rule (1):

Provided that where the order appealed against is not uploaded on the common portal, the appellant shall submit or upload, as the case may be, a self-certified copy of the said order within a period of seven days from the date of filing of FORM GST APL-05 and a final acknowledgement, indicating appeal number, shall be issued in Part B of FORM GST APL- 02A on removal of defects, if any, and the date of issue of the provisional acknowledgment shall be considered as the date qffiling of appeal:

a. Date of filing of appeal in cases wherein order has been uploaded online-As per Rule 110(4) of CGST Rules, 2017, it has been provided that where the order appealed against is uploaded on the common portal, a fmal acknowledgement, indicating appeal number, shall be issued in Part B of FORM GST APL-02A on removal of defects, if any, and the date of issue of the provisional acknowledgement shall be considered as the date of filing of appeal under sub-rule (1).

b. Date of filing of Appeal when order is not uploaded online– As per Proviso to Rule

110(4) of CGST Rules, 2017, it has been provided that where the order appealed against is not uploaded on the common portal, the appellant shall submit or upload, as the case may be, a self-certified copy of the said order within a period of 7 days from date of filing of GST APL-05 and a fmal acknowledgement, indicating appeal number, shall be issued in Part B of FORM GST APL-02A on removal of defects, if any, and the date of issue of the provisional acknowledgment shall be considered as the date of filing of appeal.

3.2. Rule 21 of GSTAT (Procedure) Rules, 2025

Rule 21(1) of the GSTAT (Procedure) Rules, 2025 provides that every form of appeal shall be accompanied by a certified copy of the order appealed against in the case of an appeal against the original order passed by the adjudicating authority and where such an order has been passed in appeal or revision, there shall be a certified copy of the order passed in appeal or in revision. There is no consideration to the fact that whether the order appealed against is uploaded on the common portal or not.

Further, in case wherein order is not uploaded online, Rule 110(4) provides for self-certified copy of the order being submitted whereas Rule 21(1) provides for certified copy to be uploaded that too either original copy of the order, or a copy thereof duly authenticated by the concerned department, or by the ‘authorised ‘representative’ of the appellant or respondent and does not considers the self-certified copy of the order as certified copy.

Rule 21(2) of GSTAT (Procedure) Rules, 2025 provides that as and when a certified copy of the decision or order appealed against is submitted online, then only a fmal acknowledgement, shall be issued by the GSTAT Portal whereas Rule 110(4) provides that date of issue of the provisional acknowledgement shall be considered as the date of filing of appeal in cases wherein order is uploaded online.

3.3.Office Order provides partial relief for the documents generated digitally through GSTN System Relief has been provided by way of office order wherein it has been clarified that the documents generated digitally through GSTN System are not required to be certified, whereas, scanned copies of the physical documents attached with the appeal shall be signed. Therefore, summary generated in DRC-07, DRC-01 or ASMT-10 is not required to be certified.

3.4. Request to reconsider

It is humbly submitted that why this issue becomes important because there were number of cases which reached before the high court for non-furnishing of certified copy and post this, there was amendment in the CGST Rules and it appears that present provisions are taking us again back to those days.

We would like to bring to your kind attention that in Vishwa Enterprise v. State of Gujarat [2025] 173 taxmann.com 530 (Gujarat)/(2025:GUJHC:18982 DB), decided on 20 March 2025, the Gujarat High Court dealt with the contention that an impugned order uploaded on the GSTN portal was invalid because it was not physically signed by the concerned authority. The Court rejected this argument, holding that once an order is uploaded on the GSTN portal, such uploading can only occur after verification and approval by the State Tax Officer. The abovesaid decision was followed in Aditya Madaan vs. Commissioner CGST GST Commissionerate Delhi [2025] 175 taxmann.com 109 (Delhi)[23-05-2025] and it was held that the act of uploading itself carries the presumption of authenticity and validity, and the absence of a physical signature does not render the order invalid.

Therefore, it is humbly submitted that the orders and notices accompanying the summary are not generated through the portal, therefore the requirement it appears remain to upload the certified copies although they are uploaded on GST Portal. It is requested to kindly reconsider the same and if at all these are covered by the presidential order, then the same may kindly be clarified.

4. Multiple certifications, attestations and verifications under different rules and requirement that foot of every appeal or pleading along with all the relevant documents including relied upon documents to have the name and signature of the authorised representative.

4.1. Present applicable Rules for certification, attestation and verification

GSTAT (Procedure) Rules, 2025 provide for multiple certifications, attestations and verifications on the same set of documents under different rules. A brief reference to the same are as follows-

Rule 22-Every appeal or pleadings- To be signed and verified by the party concerned in the manner provided by these rules.

Rule 20(3)-Every Form of appeal or application or cross-objection- To be signed and verified by the appellant or applicant or respondent or the authorised representative

Rule 20(3)-Documents produced before the Appellate Tribunal- Appellant or applicant or respondent or the authorised representative shall certify as true copy the documents produced before the Appellate Tribunal

Rule 21(1)-Every form of appeal to be accompanied by certified copy of the order- To be verified by authorised representative

Rule 22-Foot of every appeal or pleading along with all the relevant documents including relied upon documents— There shall appear the name and signature of the authorised representative. All this is in addition to what has been provided in Rule 110(4) of CGST Rules, 2017 which provides that if the order has not been uploaded on common portal then self-certified copy of the order has to be submitted or uploaded within the prescribed time.

It would be worth noting that Rule 22 at one point requires on the part of authorised representative that that at foot of every appeal or pleading along with all the relevant documents including relied upon documents, there shall appear the name and signature of the authorised representative but surprisingly only requires on the part of the party concerned that every appeal or pleadings shall be signed in the manner provided by these Rules. The next question is what happens if during the midst of proceedings, the authorised representative is changed.

4.2. Request to reconsider

Relying upon the principle what has been stated by us hereinabove, since everything is digitized and being uploaded from the User ID of the taxpayer, process can be simplified looking to the intent of formation of tribunals i.e. speedy justice and simplification of the process would be a welcome step. A single step process of verification by the appellant of all documents can be away ahead since all details are being uploaded from the User ID of the taxpayer on the portal.

5. Document other than English language to be accompanied by a translated copy in English even for the states wherein as per Official Languages Act, 1963, communication to be issued by a Central Government Office can either be in Hindi or in English.

5.1. Present provisions of GSTAT (Procedure) Rules, 2025

As per Rule 23(1) of GSTAT (Procedure) Rules, 2025, any order which is passed in a language other than in English, it shall be received by the registry accompanied by a translated copy in English mandatorily and similarly for any other document also, if it is in a language other than in English, it would also have to be translated in English. Such translated copy should be such copy as is agreed to by both the parties or certified to be a true translated copy by the authorised representative engaged on behalf of parties in the case.

5.2. Provisions of CESTAT (Procedure) Rules, 1982

As per Rule 5 of CESTAT (Procedure) Rules, 1982 language of the Tribunal was in English but at the same time, parties to a proceeding may file documents drawn up in Hindi, if they so desire.

5.3 Reference to Official Languages Act, 1963

It would be apt to highlight that as per Official Languages Act, 1963 and the Official Languages (Use for official purposes of the Union) Rules, 1976 (As amended in 1987), “Region A” means the States of Bihar, Chhattisgarh, Jharkhand, Haryana, Himachal Pradesh, Madhya Pradesh, Rajasthan, Uttaranchal and Uttar Pradesh and UT of Delhi and Andaman and Nicobar Islands. For the purpose of “Region A”, it has been provided that Communications from a Central Government office to a person in such State or Union Territory shall, save in exceptional cases, be in Hindi, and if any communication is issued to any of them in English it shall be accompanied by a Hindi translation thereof.

Further, “Region B” means the States of Gujarat, Maharashtra and Punjab and the UT of Chandigarh wherein it has been provided that Communications from a Central Government office to any person in a State or Union Territory of Region “B” may be either in Hindi or English.

5.4. Reference to the decision in the matter of Subodh Enterprises vs. Union of India [2024] 166 taxmann.com 363 (Andhra Pradesh) [05-08-2024] where an appellate authority in Category C state passed an order in Hindi Language

It would be apt to decision in the matter of Subodh Enterprises vs. Union of India [2024] 166 taxmann.com 363 (Andhra Pradesh) [05-08-2024] wherein it was held as per Official Language Act, 1963, there is a clear guideline to officers working in Central Government offices, in region of State of Andhra Pradesh, that all communications to persons residing in such a region, should normally be in English. Therefore, service of order passed by Commissioner (Appeals) only in Hindi language was held to be not permissible and accordingly, writ petitions were disposed of with a direction to Commissioner (Appeals), to furnish copies of orders passed by him in these three writ petitions, in English, to petitioners.

5.5. Request to reconsider

It is humbly submitted that when the communication language for a Central Government Office to a person which shall include an order passed in CGST as well, in such States is Hindi, asking them to mandatorily provide the document in English needs to be considered. Further relaxation in this regard would help the appellants in timely filing of the appeal, particularly in areas wherein orders are being passed by the authorities in language other than English.

It is further submitted that the appellant approaching the tribunal would not be so conversant first to get the same translated or the cost involving the same would only make it more difficult them to approach the tribunal, therefore rather than making it a mandatory part, the same may be left at the discretion of the bench.

6. Rule 45 of GSTAT (Procedure) Rules, 2025 for production of additional evidence before the tribunal is restrictive than the provisions provided in Rule 112 of CGST Rules, 2017 on the same issue of production of additional evidence before the tribunal

6.1. Present provisions of Rule 45 of GSTAT Procedure Rules, 2025

Rule 45(1) of GSTAT (Procedure) Rules puts a complete embargo over the right to produce additional evidences and provides that the parties to the appeal shall not be entitled to produce any additional evidence, either oral or documentary, before the Appellate Tribunal except for the situation provided by way of proviso. The proviso states that if the Appellate Tribunal is of opinion that

a. any documents shall be produced or any witness shall be examined or any affidavit shall be filed to enable it to pass orders or for any sufficient cause, or

b. if adjudicating authority or the appellate or revisional authority has decided the case without giving sufficient opportunity to any party to adduce evidence on the points specified by them or not specified by them,

the Appellate Tribunal may, for reasons to be recorded, allow such documents to be produced or witnesses to be examined or affidavits to be filed or such evidence to be adduced.

6.2. Rule 112 of CGST Rules, 2017 for additional evidence

Rule 45 of GSTAT (Procedure) Rules, 2025 is narrower in scope than Rule 112 of CGST Rules, 2017 which is also for the same issue and the additional situation given in the rule as compared to Rule 45 of GSTAT (Procedure) Rules, 2025 are as follows:-

a. where the adjudicating authority or, as the case may be, the Appellate Authority has refused to admit evidence which ought to have been admitted; or

b. where the appellant was prevented by sufficient cause from producing the evidence which he was called upon to produce by the adjudicating authority or, as the case may be, the Appellate Authority; or

c. where the appellant was prevented by sufficient cause from producing before the adjudicating authority or, as the case may be, the Appellate Authority any evidence which is relevant to any ground of appeal.

Only situation which matched with Rule 45 in Rule 112 is where the adjudicating authority or, as the case may be, the Appellate Authority has made the order appealed against without giving sufficient opportunity to the appellant to adduce evidence relevant to any ground of appeal.

6.3. Reconsideration of Rule 45 of GSTAT (Procedure) Rules, 2025

That in view of the above, the procedure for providing additional evidence may kindly be broadened and brought in line with Rule 112 of CGST Rules, 2017 to further promote the cause of principle of natural justice. Also, GSTAT (Procedure) Rules, 2025, are never the less subject to the provisions of CGST Act and rules made thereunder.

Therefore, it is submitted that provision might be reconsidered not only for the purpose of furthering the cause of natural justice but also to remove the contradiction between the two rules.

7. Request to rationalise the provisions relating to authorised representative i.e. Procedures about change, attestation and right to be heard of the respective party

7.1. Process for change of authorised representative

Rule 73 of the GSTAT (Procedure) Rule, 2025 regulates the process for change and provides that authorised representative (hereinafter referred as A/R) proposing to file a Vakalatnama in which there is already authorised representative on record, shall do so only with the written consent of authorised representative on record or when such consent is refused, with the permission of the Appellate Tribunal after revocation of Vakalatnama or Memorandum of Appearance, as the case may be, on an application filed in this behalf, which shall receive cons ideratioli only after service of such application on the counsel already on record.

Therefore, in case previous A/R on record does not give the consent, then process requires that such change should receive the consideration only when proof of service of such application on previous A/R is already on record.

7.2. Requirement that at the foot of every appeal along with all the relevant documents including relied upon documents, there shall appear the name and signature of the authorised representative

It is further submitted that as per Rule 22 of the GSTAT (Procedure) Rules, 2025 it is provided that at the foot of every appeal or pleading along with all the relevant documents including relied upon documents, there shall appear the name and signature of the authorised representative.

The respective appellant who is filing the appeal may be asked to put the signature but requirement of the authorised representative to do so needs reconsideration.

7.3. Restriction for the party who has engaged authorised representative for making presentation before the tribunal

As per Rule 75 of the GSTAT (Procedure) Rules, 2025, party who has engaged authorised representative to appear for him before the Appellate Tribunal may be restricted by the Appellate Tribunal in making presentation before it.

7.4. Provisions under CESTAT (Procedure) Rules 1982

On the contrary, for change in authorised representative Customs, Excise and Service Tax Appellate Tribunal (procedure) Rules, 1982, Rule 28B provided that in case an appellant/respondent changes the person authorised to represent him after the filing of the appeal or application then

a. the fact of such a change may be indicated by way of a memorandum addressed to the tribunal or an endorsement or Vakalatanama or document of authorisation and

b. upon such communication or endorsement the bench may not insist on filing of a no-objection certificate from the previous authorised representative except where in the opinion of the bench it was called for in a given case.

Further it is humbly submitted that regarding change of authorized representative, it should be at the discretion of petitioner/respondent because the consequences of the judgement in any appeal/proceedings are to be borne by the litigant and stringent procedure may lead to delays and involvement of tribunal in matters unconnected to the issue in hand.

7.5. Request to reconsider

We request you to reconsider the rules related to respective party to be heard, in case change of authorised representative & certification by the authorisation representative at the foot of every appeal. We would also like to bring to your attention that there was no such requirement as provided in Rule 22 and restriction as provided in Rule 75 of the GSTAT (Procedure) Rules, 2025.

8. Matters to be referred before the Principal Bench in case of issue involving place of supply

As per the provisions of Section 109 of the CGST Act, 2017, it has been provided that the cases in which any one of the issues involved relates to the place of supply, it shall be heard only by the Principal Bench.

Supposedly, while the adjudicating authority passed the order-in-original for tax short paid (i.e. to be paid @ 18% instead of 5%), there was an incorrect determination of place of supply for such tax short paid and out of 12 issues in the order say having an amount involving aggregate to Rs. 5 crore, and that issue was for an amount involving Rs. 50 thousand. While challenging the levy itself, an alternative ground was raised that the order by the adjudicating authority was illegal since it classified all supplies of IGST with place of supply of one single state whereas it should have been for different states. Another example can be where the goods were detained in the course of inter-state movement but penalty under Section 129 is levied under CGST and SGST and the petitioner challenges the very levy in CGST and SGST instead of IGST.

It is requested to clarify that

a. What constitutes the issue involving place of supply i.e. whether it would only when inter- state supply has been classified as intra-state supply or vice versa or it would also include when an incorrect state has been mentioned in an inter-state supply.

b. Whether if any ground in an appeal relates to place of supply, be in the alternative and for any amount, then whether all such appeals would be before the Principal Bench.

We humbly request that our representation may kindly be considered, and a convenient time be granted so that we may appear and place our submissions in person too before your goodself.

With Kind Regards

For MARWAR GST APPELLATE TRIBUNAL BAR ASSOCIATION

(CA Pradeep Jain)

President

(Adv.CA Dr. Arpit Haldia)

Secretary