Presumptive Taxation Scheme for Assessees Engaged in Eligible Profession [Section 44ADA]

(1) Introduction:- Scheme for presumptive taxation was introduced under section 44ADA from the F.Y.2016-17. Section 44ADA provides a simple method of taxation for Specified Small professionals. Earlier, the presumptive scheme of tax was applicable only for small business. The presumptive scheme of taxation reduces compliance burden on small professions and facilitates ease of doing business.

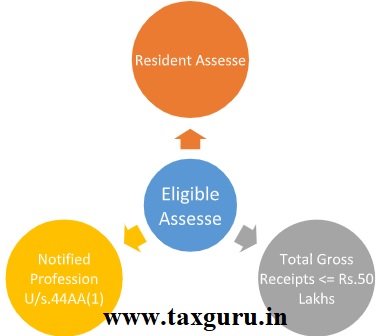

(2) Eligible business:-Presumptive taxation scheme under section 44ADA for estimating the income of an assesse:-

(i) who is engaged in any profession referred to in section 44AA(1) such as legal, medical, engineering or architectural profession or the profession of accountancy or technical consultancy or interior decoration or any other profession as is notified by the Board in the Official Gazette; and

(ii) Whose total gross receipts does not exceed Rs. 50 lakhs in a previous year.

(3) Presumptive Income: –Presumptive income would be a sum equal to 50% of the total gross receipts, or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the assesse.

(4) Eligible Assesse:-

Resident Assesse: –Resident Individual; Resident HUF and Resident Partnership Firm (Not Including Limited Liability Partnership Firm).

(5) Sec. 44ADA with regards to Allowances and Disallowances: –

(i) Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section (1), be deemed to have been already given full effect to and no further deduction under those sections shall be allowed.

(ii) In case the Assesse is a firm of Professional’s, salary and interest paid to partners is not deductible even though it is within the limit specified under section 40(b).

(6) Written down value of the asset:-Written down value of any asset used for the purpose of the profession of the assesse will be deemed to have been calculated as if the assesse had claimed and had actually been allowed the deduction in respect of depreciation for the relevant assessment years.

(7) Relaxation from maintenance of books of Accounts and audit:- Eligible assesse opting for presumptive taxation scheme will not be required to maintain books of account under section 44AA (1) and get the accounts audited under section 44AB in respect of such income.

(8) Option to claim lower profits: –An assesse may claim that his profits and gains from the aforesaid profession are lower than the profits and gains deemed to be his income under section 44ADA (1); and if such total income exceeds the maximum amount which is not chargeable to income-tax, he has to maintain books of account under section 44AA and get them audited and furnish a report of such audit under section 44AB.

(9) Advance Tax: –Eligible assesse is required to pay advance tax by 15th March of the financial year.

(10) Opting IN and OUT of Sec. 44ADA:- Assesse can opt in and opt out of Sec.44ADA at any time without any restriction. Unlike Sec.44AD for business, a professional can opt in and opt out at any time without 5 year restriction.

Author Bio