Tax Audit Meaning

-A Tax Audit is an audit, made compulsory by the Income Tax Act, if the annual gross turnover/receipts of the assesse exceed the specified limit. Tax audit is conducted in Sec 44AB of the Income Tax Act,1961 by a Chartered Accountant.

-Simply Tax Audit means, an audit of matters related to tax.

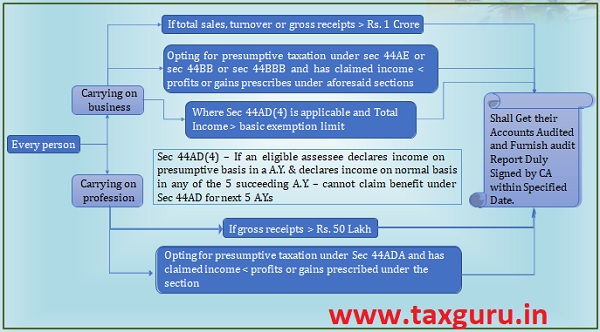

Tax Audit Applicability

- The Following persons need to be liable for tax audit U/s 44AB

- Business: Rs. 1 Crore

- It means an assesse need to be audited under Sec.44AB if his annual gross turnover/receipts in business exceeds Rs. 1 Crore.

- Profession: Rs. 50 Lakh

- It means an assesse need to be audited under Sec 44AB if his annual gross receipts in profession exceeds Rs. 50 Lakh.

Presumptive Taxation Scheme – Sec 44AD

- Businesses, whose annual gross turnover/receipt does not exceeds Rs. 2 Crore are eligible for this scheme.

- U/s 44AD need not maintain books of Accounts.

- Net income is estimated to be @ 8% of your gross receipt/turnover.

- If Gross receipts are received through digital mode of payments,

- Net income can be calculated as @ 6% and @ 8% of gross receipts are received through cash.

- If Assesse opt for Presumptive taxation u/s 44AD, then he should be follow same section of audit for next 5 Financial years.

- You need to file ITR 4 (previously ITR4S) to avail these scheme

Presumptive Taxation Scheme – Sec 44ADA

- Professions, whose annual gross receipt does not exceeds Rs. 50 Lakhs are eligible for this scheme.

- U/s 44ADA need not maintain books of Accounts.

- Net income is estimated to be @ 50% of your gross receipt.

- If Assesse opt for Presumptive taxation u/s 44ADA, then he should be follow same section of audit for next 5 Financial years.

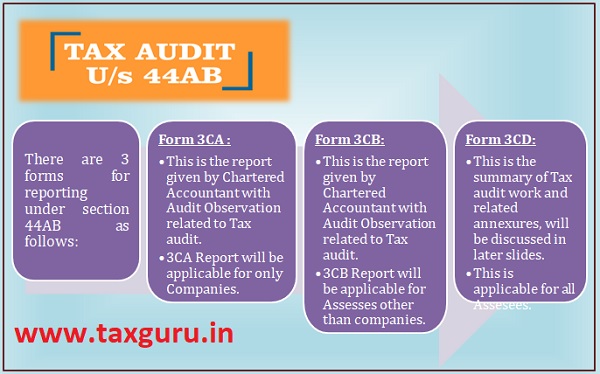

Sec 44AB – Audit of Accounts

Tax Audit Report Forms U/s 44AB

Form 3CA: Applicable for Companies

Form 3CB: Applicable for other than Companies

Form 3CD: Parts

Form 3CD: Clauses 1 to 4

> Form 3CD report has 44 clauses which are discussed as follows:

| Clauses | Particulars | Auditor’s requirements | |

| Part-A | |||

| 1.

2. 3. |

Name of Assesse

Address Permanent Account Number (PAN) Branch should be mentioned along with the name of the assesse. |

|

|

| 4. | Whether the assessee is liable to pay indirect tax like excise duty, service tax, sales tax, goods and services tax, customs duty, etc. if yes, please furnish the registration number or GST number or any other identification number allotted for the same. |

|

|

Form 3CD: Clauses 5 to 8

| Clauses | Particulars | Auditor’s requirements |

| 5.

6. 7. 8. |

Status

Previous Year Assessment Year Indicate the relevant clause of section 44AB under which the audit has been Conducted |

|

–

| Relevant Clause of 44AB | Description |

| Clause (a) | In case the assessee is carrying on business and his total sales, turnover or gross receipts as the case may be, exceeds one crore in the relevant previous year. |

| Clause (b) | If the assessee is carrying on profession and his gross receipts exceed twenty five lakh rupees in the relevant previous year. |

| Clause (c) | If the audit under section 44AB is being conducted by virtue of provisions of section 44AE, 44BB and 44BBB |

| Clause (d) | For audit being conducted by virtue of provisions of section 44ADA |

| Clause (e) | For audit being conducted by virtue of provisions of section 44AD |

Form 3CD: Clause 9

| Clauses | Particulars | Auditor’s requirements |

| Part-B | ||

| 9 (a) | If firm or Association of Persons, indicate names of partners/ members and their profit sharing ratios. | Obtain a schedule indicating the names of partners/members and their profit sharing ratios.

Please note that details of partners or members during the entire previous year will have to be furnished. |

| 9 (b) | If there is any change in the partners/members or their profit sharing ratios, the particulars of such change. |

|

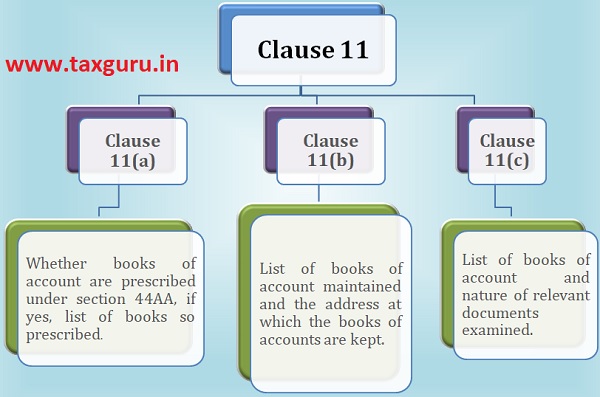

Form 3CD: Clause 11

Form 3CD: Clause 12

| Clause | Particulars | Auditor’s requirements |

| 12 | Whether the profit and loss account includes any profits and gains assessable on presumptive basis, if yes, indicate the amount and the relevant section (44AD, 44AE, 44AF, 44B, 44BB, 44BBA, 44BBB, Chapter XIIG, First Schedule or any other relevant section.) | Obtain an analysis of revenues and ascertain whether the profits and gains arising from such revenues are assessable on a presumptive basis for the following :

Other relevant sections e.g. section 172 shipping business of non- residents. Review assessments completed/ prior year tax returns to examine the basis adopted in earlier years for assessing such profits/gains. It may be noted that the income assessable under these sections is not required to be disclosed, but as the Assesse may carry on other businesses, profits included in the profit and loss account arising from the business covered by these sections is to be disclosed. |

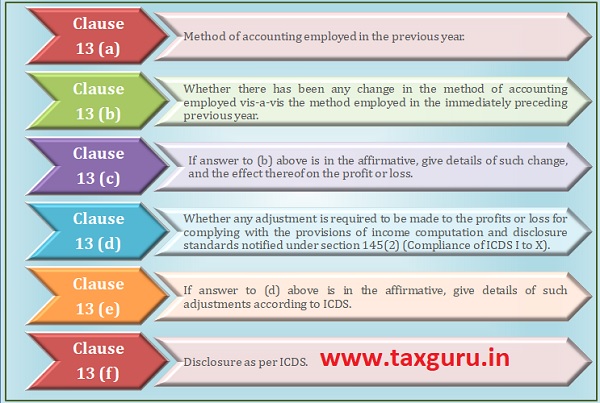

Form 3CD: Clause 13

Form 3CD: Clause 14

Clause 14 (a)

Method of valuation of closing stock employed in the previous year.

- Obtain a schedule indicating the method of valuation of closing stock employed during the year.

- Change in the method of valuation of opening and closing stock, including effect of change.

- Review the method of accounting prescribed under section 145A.

Clause 14 (b)

Details of deviation, if any, from the method of valuation prescribed under section 145A, and the effect thereof on the profit or loss.

- Ensure that any deviation from the method of valuation prescribed under section 145A is appropriately disclosed and the effect thereof on the profit/loss is also indicated.

Form 3CD: Clause 15

| Clause | Particulars | Auditor’s requirements |

| 15 | Give the following particulars of the capital asset converted into stock-in-trade:—

a) Description of capital asset b) Date of acquisition c) Cost of acquisition d) Amount at which the asset is converted into stock-in-trade. |

|

Form 3CD: Clause 16

Amounts not credited to the profit and loss account

Form 3CD: Clauses 17 & 18

| Clauses | Particulars | Auditor’s requirements |

| 17 | Where any land or building or both is transferred during the previous year for a consideration less than value adopted or assessed or assessable by any authority of a State Government referred to in section 43CA or 50C, please furnish:

|

|

| 18 | Particulars of depreciation allowable as per the Income-tax Act,1961 in respect of each asset or block of assets, as the case may be, in the following form :-

|

|

Form 3CD: Clause 20

Form 3CD: Clause 21(a)

Please furnish the details of amounts debited to the profit and loss account:-

- Capital expenditure

- Personal expenditure

- Advertisement expenditure in any souvenir, brochure, pamphlet etc published by a political party

- Club entrance fees and subscriptions

- Cost for club services and facilities used

- Penalty or fine for violation of any law for the time being force

- Any other penalty or fine not covered above

- Expenditure incurred for any purpose which is an offence or which is prohibited by law e.g. Bribes, Smuggling expenses etc.

Form 3CD: Clause 21(b)

Form 3CD: Clause 21(c) to 21(i)

Form 3CD: Clauses 22 to 25

Form 3CD: Clause 26

Form 3CD: Clauses 27 & 28

Form 3CD: Clauses 29 to 29B

Form 3CD: Clauses 30 to 30A

Form 3CD: Clauses 30B to 30C

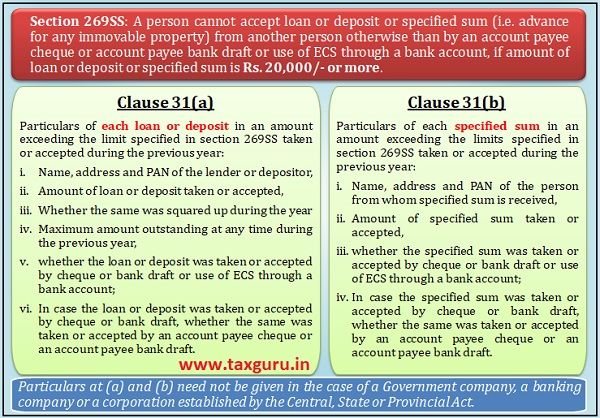

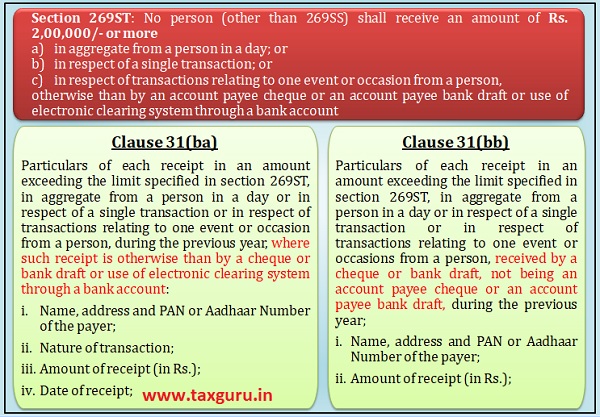

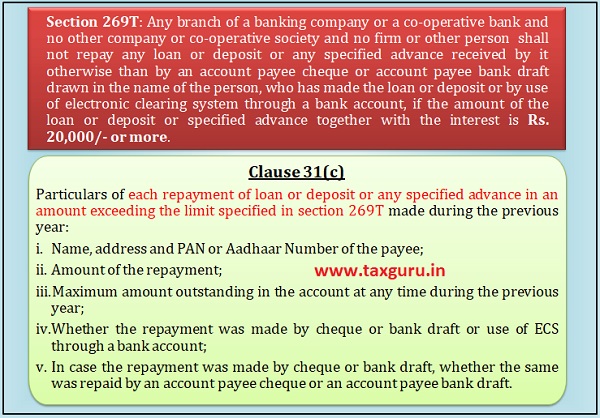

Form 3CD: Clause 31

–

–

–

Form 3CD: Clause 32

Form 3CD: Clauses 33 & 34

Form 3CD: Clause 35

Form 3CD: Clauses 36 to 38

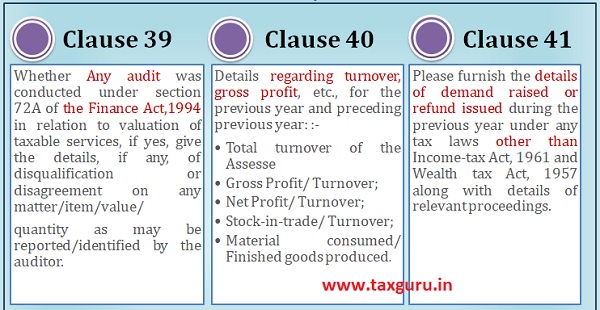

Form 3CD: Clauses 39 to 41

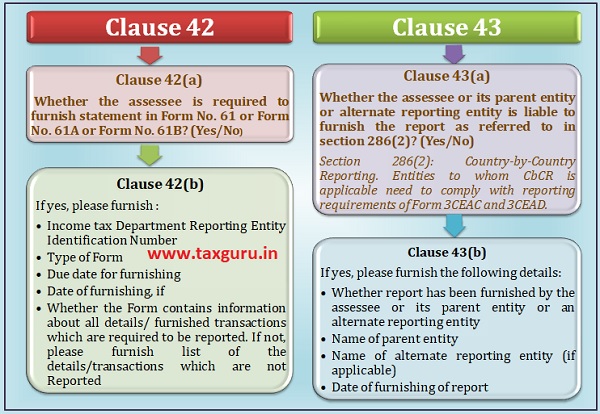

Form 3CD: Clauses 42 & 43

Form 3CD: Clause 44

UDIN – Unique Document Identification Number

Tax Audit Filling Procedure

Author Bio

Hi Komalji

If an assesse, being a small business man had business loss of Rs 1.5 lakhs on turn over of Rs 10 lakhs in Fy 20-21 which is his first year of business and not opted for PRESUMPTION scheme of taxation in any preceding years of Fy 20-21, will he has to maintain books of accounts and get tax audited for Ay 2021-22 (since he declared less than specified 6% of income on turnove) ,while he has taxable income from other sources say interest ,house property. As the amendment of Sec 54 Ad after the finance bill 2016 where it was specifically mentioned in subsection of 5 of sec 44AD that only the assesse to WHOOM SUBSECTION(4) IS APPLICABLE ( he has opted for presumptive scheme and declared income 6% on his turnover of earlier FY 2019-20) ,Tax audit is must when his total income form other sources exceeds taxable limit and is SILENT in cases where the asssesse has no business income previously ,not opted for the presumptive taxation and turnover is less than Rs 25 lakhs, the limit prescribed u/s 44AA and he has got taxable income from OTHER SOURCES during Fy 20-21.

Will you please clarify on Tax Audit of business turnover of Rs 10 lakhs in Fy 20-21 ?

can we file ITR 3 i.e regular return for income from profession showing profit less than 50% of gross receipt.if turnover not exceeded Rs. 50 Lakh.

PARTNERSHIP FIRM TURNOVER APPROX 15 LACS . WHAT THAT FIRM IS REQUIRED AUDIT.

In relevant clauses of 44AB and description table , which is under heading FORM 3CD : 5 to 8 , u mentioned 25 Lakh under clause (b).

Please correct the same….

Great presentation 👍 only point which I have found doubtful that is 40% part rest good. It will be more better if writer can add FY 20-21 tax audit changes as per. Budget so that can be made easily

The heading of your topic “Audit for FY 19-20” and your article content doesnt match. May be u forgot to throw light on the topic which is need of the hour.

Very Good Article with complete detailing information ..

Thanks a lot.

VERY KNOWLEDGEABLE ARTICLE BUT HOW TO DOWNLOAD I DON’T KNOW

Dear all,

Sorry for the inconvenience, you all are requested to ignore “If Gross receipts are received through digital mode of payments,Net income can be calculated as @ 40% and @ 50% of gross receipts are received through cash” point as it was just a misunderstanding.

Presumptive Taxation rate is only 50% u/s 44ADA.

Sorry again!!

Timely article helpful for CA/CMA students.

You have mentioned tax on 40% income u/a 44ADA if receipts through digital mode..

Can you pls recheck or send a link of amendment from 50% to 40% in this regard.

Hello,

Can you please give reference for provision u/s 44ADA wrt income to be consider @ 40% if received through digital mode of Payment.

Cz there is no provision in Income tax act till Finance Act, 2019 and there is no amendment in the said provision in Finance Act, 2020.

Thank you in advance.

In Section 44ADA – declaration of profit is allowed at 50% only. 40% provision not exist i think. Kindly update the same.

FORM 3CA IS NOT OLY FOR COMPANIES BUT FOR THEM WHO HAS TO GET THEIR ACCOUNTS AUDITED AS PER OTHER ACTS OTHER THAN INCOME TAX ACT LIKE LLP IF THE TURNOVER CROSSES RS. 40 LAKH.

Hi Komal,

I could not found this reduced rate of tax for professionals @40% for digital payments as mentioned by you in your article in following words. Pls. through light.

If Gross receipts are received through digital mode of payments,

Net income can be calculated as @ 40% and @ 50% of gross receipts are received through cash.