CA Paras Mehra

Currency Ban: How penalty CANNOT be imposed on cash deposits in bank account under Income Tax Act, 1961

Introduction

We are going through a very unusual phase of Indian economy where people are rushing nowhere carrying cash in hand. I have experience it first time when people are ready to pay the full amount of tax or they are ready to even forego 50% of the amount still they are not able to buy peace of mind thanks to the Modi government. I really appreciate this brave and very bold step of Indian government.

However, things are now turning little ugly on ground with regard to tax terrorism. I support tax friendly measure, honest tax scrutiny but as a responsible citizen of this country, I nowhere in favor of tax terrorism.

Further, in this article I would also discuss about the penal provisions and related aspects where government is claiming to levy 200% penalty on cash deposit with regard to currency ban in India.

How it all started?

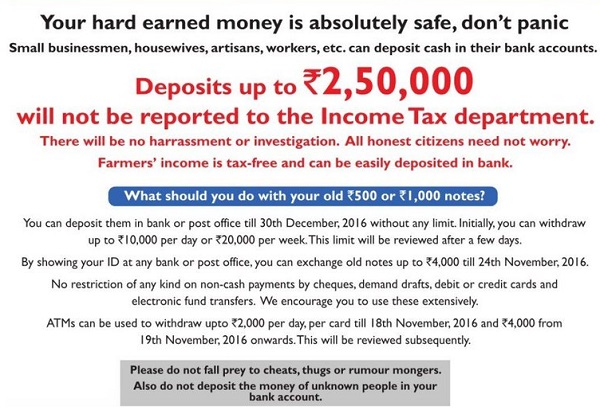

On 8th November, 2016 Prime Minister Modi announced that Rs.500/1000 note shall not be a legal tender and asked people to submit/exchange all the Rs.500/1000 currency notes till 30th December, 2016. Since then, things have become ugly;

- There are raids conducted by Income tax and sales tax department which is also bothering the honest person.

- Environment of fear and anxiety all around.

- Everyone is scared of income tax levying penalty of 200%

- Ministers adding to tax terrorism by giving unnecessary speeches.

I suppose this must not be the intention of PM Modi as well. Further, people from legislature (e.g. Ministers) are guiding or I should say influencing the work of the executives which are powered independently under constitution of India. Furthermore, the electronic media, social media is only making things worse by making information viral which is most of the time is fake.

All the people of India are under panic and they are actually scared in depositing cash into bank because of Income tax notices and harassment.

The reality of 200% penalty

The penalty of 200% is a reality and levied under section 270A of the income tax act, 1961 in cases of under-reporting of income or misreporting of income. Some of the points are outlined:

1. Cash Deposited more than returned income: Here I am not talking about the deposits up to Rs.10 lakh. If you want to read about deposits of less than 10 Lakh, kindly read my previous article.

I am talking about the deposits in lakh, crores. Now in case you have deposited huge cash into your account and you are not able to justify then you are under trouble. You will have to pay tax, penalty @ 200% or interest if any.

2. Changing money through illicit practice: Since people understand the point no.1, so they are looking for different options in order to safeguard themselves. However, they should understand that these measures are temporary and will only making the things worst afterwards.

3. Buying gold: People are rushing towards buying gold and jewelry. However, here are the following reasons which may prove detrimental:

- Jewelers are now covered under excise law, which means that they have to maintain records for inputs and output made during the year.

- Since everybody will be rushing to jewellers to covert cash into gold, this would surge up the price for gold and ultimately, people will buy it at a higher price. Since it will be a temporary surge, the prices of gold will come down soon. This would lead to fall in value of wealth.

- Jewelers are raided by the authorities and vigilance is also after them. Hence, government will get all the information about the buy/sell of gold.

Under which situation penalty can’t be levied

Suppose, a professional have some 10 crore with him and he deposited the entire amount in bank and paid the income tax and service tax on the amount. So he conducts the following calculation:

| PENALTY | SUB TOTAL | AMOUNT |

| Total Amount Deposited (A) | 10 Crore | |

| Service tax included in above (Reverse Calculation) (B) | 1.30 Crore | |

| Revenue Amount (A-B) | 8.70 Crore | |

| Tax on above amount (assume 30%) (C) | 2.60 Crore | |

| In Total he paid (B+C) | 3.90 Crore | 39% of total amount |

He paid the entire amount of Rs.3.90 Crore and filed the Income tax Return for FY 2016-17.

Assessment Proceedings

As expected, AO shall issue the notice under section 143(2) to open the scrutiny against the assessee. Further, AO shall ask for justification of the amount credited.

Suppose Assessee not able to justify the AO. AO shall impose section 68 and mark it as cash credits. Further, he shall revoke section 115BBE which will tax the cash credit at the maximum rate possible.

In our case, assessee has already paid the required tax to the government of India. Hence, there will not be any balance tax to be collected.

Now, AO shall also try to impose the section 270A to levy the penalty at 200%. So, let us now discuss the section 270A.

- Section 270A has been introduced in finance act, 2016.

- This section is applicable in case of under-reporting of income.

- The minimum penalty of 50% and maximum of 200% (only in case of misreporting) is prescribed in this section.

Analysis:

On the plain reading of this section, it is very clear that it is applicable in case of under reporting of income. Under-reporting of income means where assessed income is more than returned income.

In our case, assessed income shall be equal to returned income. As assessee has voluntary disclosed all the facts and information about the income. Since, the basic condition of this section is not triggered and hence, section 270A cannot be imposed.

Other possible options

- The other possible option for AO is the recourse of section 148. One may think that he may open the scrutiny proceeding of previous years. However, in that case, AO will have to record reasons to believe to open scrutiny under section 148. In our case, Assessee already declaring and disclosing all the income and paying the required taxes. Hence, this option may remain feasible for AO until he record reasons to believe.

- Income tax Raid: Income tax department may initiate IT raid as soon as they get to know about the deposits. However, this may only harass assessee because he has already disclosed all the income and paid all the tax on the cash deposited hence IT raid may become useless in this regard.

Conclusion

In the end, we observe that there is lack of income tax machinery under which penalty can be levied in the aforesaid case. However, these are my personal views. One can always differ. If you have any contrary view against my views, I would love to have them from you. You can send your views or queries at paras.mehra18@gmail.com.

Appeal from all professionals

I would also like to appeal to all the professionals in the industry about not too carried away by the media and the trends. This is the opportunity where we can prove our brain and ability. We are here to resolve the queries of our clients and general public not by unfair practices but through our own capability.

Let us unite together once again and lead the path of honesty, contribute to the society and to the great nation.

About the author

CA Paras Mehra is a practicing Chartered Accountant having a vast experience in this field of Taxation.

The question and answer furnished are very useful. However you some illustration with working sheets are easily understand by the ordinary lay men. Overall it is good

Iam doing a trading business,suppose any amount i.e.my 45/55

lac are yet to be received from my coustums.they are bringing only 500/1000 notes, if I do not accept it from them they say OK, will give running currency after 6months or may be 1year also.

If I do not accept it what & how will I pay to my suppliers as they are not ready to wait,some suppliers are ready to accept the old notes of 500/1000. Please give me proper guideline as I have no other option.. pls reply.

Thnx.

I TOOK A personal loan 11 laks 4 months back drawn the amount but not used again deposited in bank after nov 10th is it allowed

Honestly speaking a person deposit money into his account is now honestly is suffering on account of somebody mistake and not able catch hold of criminals and on the other hand a innocent and honest person is suffering in this situation . Now presently suffering honest citizens and innocent persons on account criminals not punished criminals by the Government.

sir

I am accountant and i am deposit cash in my a/c and pay tax (sales Tax & Income Tax) in my a/c continuously is any problem or not to me and party is given to cash to me

we are running a industry with a turn over of 30 plus crores and have a cash in hand of about 70 lacs. if we deposit the whole cash will the AO or ITO raid the unit and harass or any other problem to be faces by us

Dear Mr. Paras

Good analysis and presentation… What I am unable understand as a lay man and as a honest/ prompt tax payer of this country is….

That means, Do you want to say that the whole exercise or the purpose of Modi’s demonitising policy is forefieted???

The real culprits who have black money or ill gotten wealth, can escape by depositing any amount of cash into by paying 39% towards ST & IT can enjoy the balance of 61% of their ill gotten wealth???

This is still cheaper deal compared to Voluntary Disclosure Scheme, where one had to pay 45% as IT !!!

If so, It is ridiculous!!!

I am a lay man and I do not fully understand your IT Acts etc., Pls. explain…

I agree with Mr Ganesan that the onus is on assessee to prove that its current income . In such situation can AO reopen earlier years

Pl also refer to Section 197(c) of the Finance Act 2016, which provides that where any income has accrued prior to commencement of the Income Declaration Scheme , in respect of which the declaration under the Scheme was not made, such income shall be deemed to have accrued in the year in which notice under Section 142 /143(2)/148/153A/153C is issued by the Assessing Officer, giving sweeping power to tax ,even beyond the time limits of reopening the assessment and this provision has been explained in reply to question 4 of the Circular dated 27-06-2016 issued on IDIS in relation to undisclosed income prior to AY 2016-17.Being so, onus to prove that the income represented by the cash deposits, accrued only in 2016-17 has to be supported by evidence.

Very nice article – but, in the example above – the professional needs to deposit all the old notes worth Rs. 10 Crores and needs to show cash service provision of Rs. 10 crores in the month of November 2016 only — since, the service tax till October must have already been paid by the Professional.

So much cash business from 1st. November till 8th November midnight!! (Since, he is not legally bound to accept older notes post November 8th, 2016).

Can you please clarify this point?

Can any professional justified that he had received this amount before 8th of November or after 8th of November and what excuse with him/her about Service Tax Number for which he applied after 8th November. Finally what about he told regarding accounts book and can give the name of clients from he received fees in cash.

I feel the Government will have parliament amend Section 270A and some other sections to recover tax + penalty at 45% to bring this deposit to tax on par with what would have happened under IDS. They will let a large majority of small depositors to use this method to come clean and still save a little more than half of their undisclosed wealth. Some more will have to be sacrificed by such people to service tax / VAT authorities. For some really big depositors, reopening of assessments of past years can’t be ruled out.

Respected Sir,

Good article by CA Paras Mehra.

Thank you.

Apart from these things,I have one clarification with Paras Mehra Sir.

Even though the Jeweller record the sales and remit the cash in bank after November 8,2016,Whether it is legal to accept the cash of Rs.500 and Rs.1000 notes after 08.11.2016 Which are announced by Union Govt as invalid.

I am awaiting for your valuable Clarification.

Yours

P.R.Rajendran B.Com.,MBA

Tax Consultant and VAT Practitioner

I fully agree with you Mr. Paras. No penalty under section 270A can apply if we pay the full tax on the cash deposits and there is no difference between the returned and assessed income because there will not be any under-reporting. However, my apprehension is that if the source is not declared, then the AO may refer case to ED under the PMLA and the assessee may face harassment from ED.

This is how black money is generated in our country. The main three culprits are Lawyers, CA’s and doctors apart from politicians, burecrauts and businessman. These three profession is spoiling our country giving opinions how to cheat the govt and also escape from judiciary by suitably bribing the judiciary. These type of opinion makes common man think that they can escape. So people have to be careful

It is not so simple as explained by you….

Any depositor of Bulk Cash can save to the extent he/she can explain and substantiate the source of Income…

Dear Sir,

Well analyze and explained!! However, I have following reservation.

1. if any professional disclose unusually high receipt (Income) in particular year i.e. AY 2017-18 then ITO may ask list of client to whom services provided? which kind of services provided? if services provided to business entity of more than 20,000/- why they paid in cash? if services provided to any other for more than 2 lacs, PAN quoted on all documents etc.

2. if one can not answer above question ITO can legally presume that these income is of previous years and tax has been escaped in those year and can levy penalty.

3. as suggested in point 2 on same ground ITO may open previous years assessment with recording reason in writing, in any case he has valid reason to open it.

4. ITO can also conduct search / survey / raid, if they do it, then there are possibility that person who possessed unaccounted money also possessed unaccounted gold, property as well. I guess everyone will agree that on unaccounted properties (other than cash) income tax officer levy 200% penalty and may initiate prosecution.

If one can explain is anything of above is beyond the legal limit of IT department ?

Dear Mr. CA Paras Mehra,

Please check grammar before you write an article for the public benefit. Please revisit the para: Suppose Assessee does not able to justify the AO. AO shall impose section 68 and marked it as cash credits. Further, he shall revoke section 115BBE which will tax the cash credit at the maximum rate possible” The villains are the verbs ‘impose’ and ‘revoke’.

I do 100% agree with the view of Paras Mehra in this article. The Income can he show in the return as ” Income from other sources”. The assessing officer can’t do any thing.

I’m a government servant. I have played tax from last 30yrs. and my monthly income is Rs.60000 .Now ,can u please tell me ,how much can I deposit in my salary account without Income Tax notice and Tax levy

If it was so simple to pay tax @ 30% & get away with unaccounted money, Govt would not have introduced VDIS with 45% tax rate.

Second, the Assessing Officer will seek to levy 200% Penalty on the Old Notes deposited in cash. Not to mention prosecution options available as well.

Govt also has the option of retro respective amendment of Tax laws, to plug lacunae in tax laws.

Further, possible action under PMLA as well as by ED

So one needs to be very careful, before advising clients to deposit any Old Notes in Bank [ esp large amounts ], unless source thereof can be properly proved with evidence.

Mr. Ram is of 70 yrs. Has interest on FDs Rs.3,50,000 /- after deduction of amount u/s 80 C during F.Y. 16-17 Asst yr 17-18. He has no other income i.e current taxable income is 3,50,000/- He has deposited Rs.3,00,000/- in old currency is known as past income. What will be income-tax and penalty for the Asst,year 2017- 2018 ?

Some village fellow never believe in banking system and their whole life income money around 10 lakes cash in handhand now have to deposite in bank . And my point is that the income is divided by 10 years it’s means 1 lakes perror year, is they have to pay tax on their 10 lakhs whisky is by force deposit in bank, kind give valuable suggestions sir

if a business man can deposit the money in his current account wthin december 30, 2016 and how much – please give me clarification –

Very nicely analysed. Only problem is AO may probe this further. What is the law, if assessee declines any further information ? Is AO empowered to refer to other government and statutory authorities for further investigation ? This could cause the real problems

Well explained

Hi, very informative article.

I am a prospective investor and was looking for profitable options to invest. I wanted your views about Peer to peer lending and is it a viable option to invest?

If an ordinance is passed to start criminal proceedings if there is no justification of deposit or symetrical with other assessment years…I.T. Act cannot be a safe guard for those miscreants and disturbs very essence of demonitisation…What is your opinion Professionals?

500/100- rs old notes -no more valid after 8th November 16- 20 pm

——————————————————–

date 12 November 16

cash deposit up to rs 2.5 lakh, is common for all, normal person up to age 60 years, senior citizens, and super senior citizens,

it would have been better if this limit differs with category, male, female ( up to 60 years,), senior citizens,up to 80 years age, & super senior citizens ( above 80 years age ), as per their IT eligibility limit.

Beautifully explained.

If there is no under reporting i.e. assessed income is equal to returned income , then there would not be any penalty u/s 270A . Neither for under -reporting ( ie. 50%) nor for misreporting ( i.e. 200%). As sub clause 9 of section 270A read with sub clause 8 of section 270A , could be imposed ( i.e. case would fall under the misreporting ) if there is under -reporting of income.

It is not only unreporting but also misreporting. IT will be well within the right to ask your source of cash money. ED will be well within right to ask source of money. is it drug or terror money? If the depositor does not explain satisfactorily, even after depositing money and paying tax, it will be a case of MISREPORTING and that attracts Section 270A. it will certainly attract penalty.

Bakul Gandhi Practising Company Secretary

I can deposit Rs 25000 in my bank account?

As of now this will be the correct position. However if the taxpayer did not substantiate the nature of income the Govt may bring amendment w.e.f 9.11.2016 to treat such cash deposits as misreporting in books consequent to ban on currency of 1000 or 500. This aspect is to be protected while bringing such income in books

One questiin,……using IT return info, can an action under Money Laundering Act ,or Benami Transactions be initiated against such person?

When the AO ask for details, you can say you don’t have any details. Then the only option for him is to assess the amount u/s 68 as unexplained credits. Nothing else

Sir,

This is for a professional. You are asking him to cover the service tax aspect also.

What about a Businessman. Can he deposit Rs 1 cr, and pay 30 % tax and show this income under the head ” Income from Other Sources”

During Scrutiny how will he explain the source.

Regards,

Shyam

Well explained CA Paras. I fully agree with you.

Sir ,

The dept may ask you to produce the list of persons form whom the fees have been collected . Since we say that it is regular income . The dept may cross verify .

Sir,

This is for a professional. What about a business man. Can he just deposit his cash and pay 30 % tax thereon. The Income can he show in the return as ” Income from other sources”

During scrutiny can he just say I offered income without any details.

Regards,

Shyam

Sir,

Good suggestion. For the above eg of a professional, AO may ask list of clients to cross verify and why no tds. Will this not pose a bigger problem.