Article explains Registration Procedure Taxation of Partnership Firms /LLP which includes Income Tax Rate applicable and Provisions related to

-Interest and Remuneration to Partners/Designated Partners, Conditions for assessment as a firm, Partners’ assessments, Losses of the firm.

-Due dates for filing return of firm, Allowability of remuneration and interest vis-a-vis presumptive .

-ITR Filing For Partnership Firm

-Compliance Each Year

Page Contents

- I. Rate of Income tax applicable to Partnership Firm / LLP

- II.Method OF Calculating PGBP income Of Partnership Firm

- III.Remuneration To Partners/Designated Partners

- IV.Interest To Partners/Designated Partners

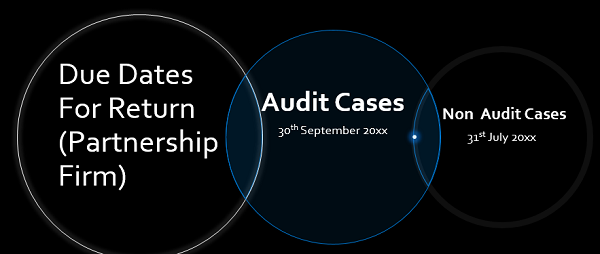

- V.DUE DATES OF RETURN OF PARTNERSHIP FIRM

- VI. Timeline : Every Year to Year Action Plan

- VII. Overall General Timeline For Partnership Firm Compliance WRT To Income Tax Act , 1961 for Partnership Firm

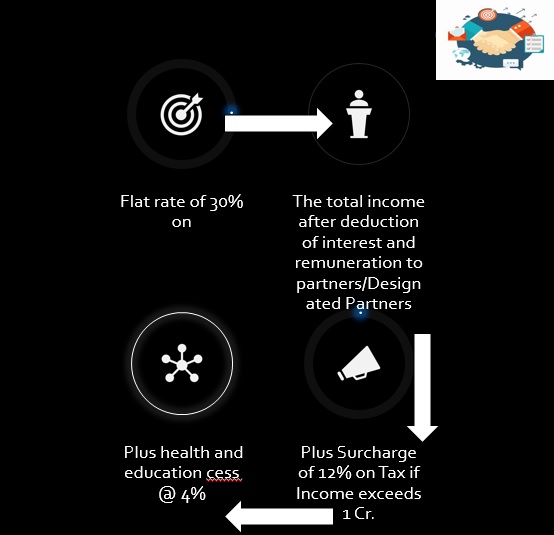

I. Rate of Income tax applicable to Partnership Firm / LLP

I. Rate of Income tax applicable to Partnership Firm / LLP

- The Partnership Firm ( State of Punjab) can be registered online at http://pbindustries.gov.in/static

II.Method OF Calculating PGBP income Of Partnership Firm

| Particulars | Amount |

| Net Profit as Profit & Loss Account Year ending 31.03.20xx | XXX |

| Add/(Less): Income Assessable under Other Heads of Income | XXX/(XXX) |

| Add: Expenses Admissible but not Debited to Profit & Loss Account | XXX |

| Less: Expenses Inadmissible but Debited to Profit & Loss Account | XXX |

| Add/(Less) : Adjustments as per Income Computation & Disclosure Standards | XXX/(XXX) |

| Profit As per Income Tax Act 1961 | XXX |

The PGBP computation of Income of partnership firm is alike to Computation of PGBP income for Individuals Subject to Maximum capping in case of few expenses. Some of which are as follows.

III.Remuneration To Partners/Designated Partners

Major Things to Be Taken Care of

1.Payment of Remuneration to a non-working partner will not be allowed as a deduction.

2.. A ‘working partner’ is an individual who is actively engaged in conducting the affairs of the business or profession of the firm.

Maximum Salary Allowed :

a. On the first 3,00,000 of book profits or in case of a loss

a. Rs. 1,50,000 or

b. at the rate of 90% of the book profit

c. (whichever is higher).

b. On the balance of book profits at the rate of 60%

IV.Interest To Partners/Designated Partners

V.DUE DATES OF RETURN OF PARTNERSHIP FIRM

VI. Timeline : Every Year to Year Action Plan

1. Advance Deposit Of Taxes During The Year

| Due Date | Advance Tax Payable |

| On or before 15th June | 15% of advance tax |

| On or before 15th September | 45% of advance tax |

| On or before 15th December | 75% of advance tax |

| On or before 15th March | 100% of advance tax |

2. Prepare Final Accounts Year Ending 31/03/20xx

- Closing of Year End accounts

- Includes Preparation of

- Balance Sheet

- Profit And Loss Account

- Separation of Personal Expense from Business Expenses

- Finalization of Records kept as an evidence of Existence of each transaction.

3.Filling of ITR Form And Creation of XML File

- After First two steps being done , most important step is to create the XML file Ready to be upload.

- As per Nature of Business and Types of Assessess the ITR Forms are differentiated .For Partnership Firms

- ITR – V

VII. Overall General Timeline For Partnership Firm Compliance WRT To Income Tax Act , 1961 for Partnership Firm

Author Bio