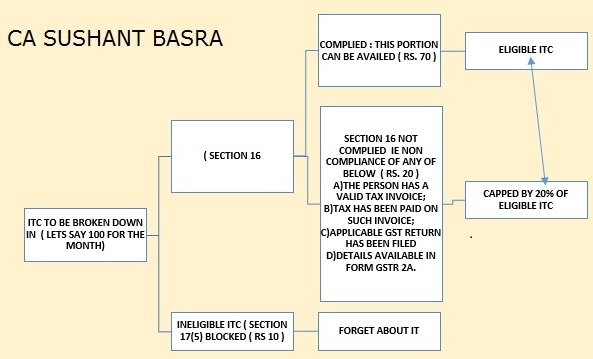

ANALYSIS ITC CAPPED BY 20% OF ELIGIBLE ITC OF GSTR 2A

CBIC by Notification No. 49/2019 – Central tax – dated 09 October, 2019 it has placed a cap on availment of Input Tax Credit (‘ITC’) to the extent to 20% of eligible input invoices or debit notes.

TABLE FOR ABOVE UNDERSTANDING

| Sr. No | Particulars | Amount |

| A | TOTAL GST INPUT PAID ( BOOKS INCLUDING BLOCKED) | 100 |

| B | BLOCKED CREDIT | 10 |

| C | SECTION 16 NOT COMPLIED | 20 |

| D | ELIGIBLE ITC | 70 |

| E | MAXIMUM CAPPING ( 20% OF ELIGIBLE ( D ) IE RS. 14 ) IE EXTRA INPUT AVAILABLE |

14 |

| F | BLOCKAGE OF FUNDS ( C – E ) | 6 |

| HENCE BUSINESSMEN AND THEIR CONSULTANTS HAVE TO TAKE CARE THAT THERE WILL SERIOUS BLOCKAGE OF FUNDS ON ACCOUNT OF NON COMPLIANCE BY VENDOR THEREFORE CHOOSE YOUR VENDORS WISELY AND THERE HAVE TO BE CONSTANT CHECK WITH REGARD TO ITC RECONCILIATION OF BOOKS WITH PORTAL | ||

Always sharing Knowledge to the best .

Warm Regards

CA Sushant Basra

B.COM , ACA , DISA ( ICAI )

Email : cabasrasushant@gmail.com

My fellow members kindly correct me if wrong.

Kindly Refer to

Privacy Policy &

Complete Terms of Use and Disclaimer.

Author Bio

Dear Sir,

My company is “X”, Pur goods from “Y” with ITC in Jan-19. We have exported the same to “Z” company to Dubai in Jan-19 without paid tax (LUT bond). We have filed GSTR 3b & 1 respectively. But we forgot to mention export Inv details in GSTR1/6A. Now we are going to file RFD01 for ITC refund. will be there any problem? Plz advise me in priority. Thank you in advance.