Introduction

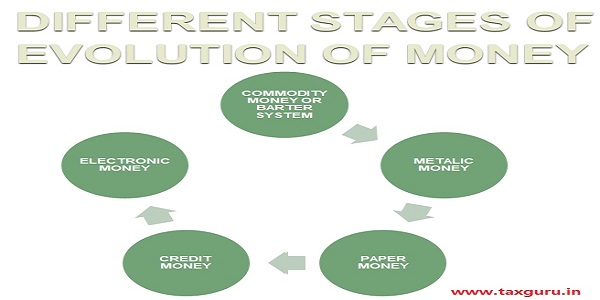

We were told by history that before advent of cash there was concept of barter system though barter system where there was no currency ‘no cash’ and things were exchanged according to needs and sooner society realized that barter system having its own series of advantages and disadvantages need to be left behind with time and later on various personalities, kings and governments introduced new coins and currency made from time to time making impressions of their choice on such coins.

Page Contents

- I. Analysis of Section 40A(3) and 40A(3A)

- II. Disallowance of Depreciation section 43(1))

- III. Applicabilty of disallowance u/s 40A of the Act in case assessee opts for presumptive taxation u/s 44AD

- IV. Restrictions on Loans, Deposits & Advances

- V. Restrictions on Cash Transactions in Real Estate

- VI. Restrictions on Income Tax Deductions in case of Cash Payment

- VII. Restrictions on Cash Transactions of Rs. 2 Lacs or More

- VIII. Disallowance u/s 40A(3) vs Restrictions on cash u/s 269ST

I. Analysis of Section 40A(3) and 40A(3A)

(a)Analysis of sec 40A(3) of the Act.

Where payment is made in the year the expenditure is incurred: 100% disallowance of payment if in excess of Rs. 10,000 and not by a/c payee cheque/draft/ECS. [Sec 40A(3)] There are following two conditions for the applicability of this section. If both of these two conditions are satisfied, then the provisions of this section will be applicable.

Condition 1.

The assessee incurs any expenditure exceeding Rs.10000/- which is allowable for computing income under the head business or profession.

Condition 2.

The assessee has made payment or aggregate of payments in a day exceeding Rs.10000/- in cash.

If the above two conditions are satisfied, then whole of the expenditure shall be disallowed under this section. In case where payment is made to the transporters for plying, hiring or leasing goods carriages, then amount of Rs.10000/- shall be increased to Rs.35000/ in the above two conditions.

Example: Where expenditure of shop expenses for Bill raised on 11/11/2019 is made on 03/03/2020 by cash amounting to Rs. 30,000, then the payment of Rs. 30,000 will not be allowed as a deduction for the PY 2019-20

Payments made on a single day: where the payment or the aggregate of payments made to a single person on a single day against one bill exceeds Rs 10,000 then the disallowance of such expenditure will be covered by Sec 40A. Thus for disallowance u/s 40A(3) the amount of the bill raised and the payment or payment(s) made to the person on a single day both exceed Rs 10,000.

Illustrations for Sec 40A(3)

(i) An expenditure of Rs. 40,000 is incurred for purchase of stationary against Bill no 2 from M/s XYZ Ltd on 01/01/20. The assessee makes separate payments of Rs. 15,000, 16,000 and Rs. 9,000 all by cash, to the person concerned in a single day. Since the aggregate amount of payment made to a person in a day, in this case, is Rs. 40,000. Since, the aggregate payment by cash exceeds Rs. 10,000, Rs. 40,000 will not be allowed as a deduction in computing the total income of the taxpayer in accordance with the provisions of the Act.

(ii) An expenditure of Rs. 30,000 is incurred for purchase of stationary against Bill No 1, 2 & 3from M/s XYZ Ltd on 01/01/20, 28/01/20 & 01/02/20 for Rs 10,000 each. The assessee makes separate payments of Rs. 10,000, Rs. 6,000, Rs 5,000 and Rs. 9,000 all by cash at different times, to the person concerned on a single day. Since the aggregate amount of payment made to a person in a day, in this case, is Rs. 30,000 however since the payment is on account of three bills, none of which is in excess of Rs 10,000, thus the entire payment will be allowed

(iii) An expenditure of Rs. 37,000 is incurred for purchase of stationary against Bill No 1 & 2 from M/s XYZ Ltd on 01/01/20 and 01/02/20 for Rs 28,000 and Rs 9,000 respectively. The assessee makes separate payments of Rs. 15,000, Rs. 13,000 and Rs. 9,000 all by cash, to the person concerned in a single day. Since the aggregate amount of payment made to a person in a day, in this case, is Rs. 37,000 however since the payment is on account of two bills, one of which exceeds Rs 10,000, thus only Rs 28,000 will be disallowed

Example: An expenditure of Rs. 60,000 is incurred freight against Bill no 2 from M/s NITCO Roadways on 01/05/19.The assessee makes separate payments of Rs. 24,000, Rs. 36,000 on 01/09/19 and 01/10/19 respectively. In this case since the payment made is not in excess of the limit of Rs 35,000 thus it will not be disallowed, however the payment made on 01/10/19 shall be disallowed as it exceeds the limit of 35,000. Thus out of expenditure of Rs 60,000 only Rs 24,000 will be allowed as a deduction

(b) Analysis of sec 40A(3A) of the Act.

Where payment is made in the subsequent years (after deduction has been claimed in an earlier year): where an expenditure has been allowed as a deduction in an earlier year(on due basis) and if in any subsequent year the payment in respect of such expenditure is in excess of Rs 10,000 and not by an account payee cheque, account payee bank draft or ECS – then the payment shall be deemed to be income under the head business & profession for the previous year in which payment is made.

There are following two conditions for the applicability of this section. If both of these two conditions are satisfied ,then the provisions of this section will be applicable.

Condition 1.

The assessee had claimed deduction in respect of an expenditure exceeding Rs.10000/- in any of the earlier years.

Condition 2.

The assessee has made payment of the liability(condition no.1)in cash in subsequent year and payment is exceeding Rs.1 0000/-in a day

Plan to apply flat rate of profit to avoid disallowance.- As observed in New Narayan Builder v. ITO (1992) 43 TTJ (Ahd-Trib) 508, the restriction contained in section 40A(3) relating to allowability of any expenditure would come into play and when such expenditure is otherwise treated as allowable under section 30 to 37. If the income of the assessee is determined by applying flat profit rate, the question of considering the allowability of different items expenses claimed by the assessee does not arise at all. This also affirmed by Ahmedabad Bench of Tribunal in Hynop Food & Oil Industries (P) Ltd v. CIT (1994) 48 ITD 202(Ahd-Trib). But in ITO v, D.D hazare (1994) 48 ITD 595 (Bom-Trib), it was held that where profit are estimated rejecting books of account, it does not bar disallowance under section 40A(3). According to CIT v. Padam Chand Bhansali (2004) 85 TTJ (Jod-Trib) 215, no addition can be made where income has to be computed by applying net profit rate

Advance payment is not out of ambit of expenditure.- According to Vijay Kumar Ajit Kumar v. CIT (1991) 55 Taxman 388 (All), merely because a payment in excess of prescribed limit is made prior to delivery of goods, it cannot be argued that it constitutes an advance and not expenditure so as to invoke provisions of section 40A(3). X has given an advance to Mr. Y of Rs. 2,50,000 in cash on 15.03.2020 for supply of goods. The goods are supplied on 29.05.2020 for Rs. 2,50,000, and the advance is adjusted. Section 40A (3) will be attracted and Rs. 2,50,000 will be disallowed is Assessment Year 2021-22. Further, it is to be noted that in A.Y. 2020-21 Mr. Y has received Rs. 2,50,000 in cash in contravention of Sec 269ST. He shall be subject to penalty u/s 271 DA of the Act.

Illustration: A Ltd. purchases goods on credit from a relative of a director on June 20, 2018 for Rs. 50,000(market value: Rs 42,000). The amount is paid by a crossed cheque on June 25, 2018.

Out of the payment of Rs. 50,000 Rs. 8,000 (being the excess payment to a relative) shall be disallowed under section 40A (2). As the payment is made by a crossed cheque and the remaining amount exceeds Rs. 10,000, 100% of the balance (i.e., Rs. 42,000) shall be disallowed under section 40A(3).

1. Purchase of stock-in-trade, whether expenditure to be covered by section 40A(3).- In Attar Singh Gurumukh Singh, etc. v. ITO(1991) 191 ITR 667(SC), Supreme Court held that the word ‘expenditure‘ has got its wide import. The expenditure for purchasing stock-in-trade is one of the outgoings. The value of the stock-in-trade has to be taken into account while determining the gross profit under section 28 as per the principles of commercial accounting. The payment made for purchasing stock-in-trade would also be covered by the word expenditure and such payment can be disallowed if they are made in cash in a sum exceeding the amount specified in section 40A(3). Rule 6DD also contemplates payments made for stock-in-trade and raw material.

2. Disallowance under section 40A(3) not attracted where books of accounts are rejected.- In ITO v. Sadhwani Brothers (2012) 44 (II) ITCL 371 (Jp ‘B‘- Trib) : (2011) 142 TTJ (Jp ‘B‘- Trib) 26, it was held that since the books of accounts were rejected therefore, provisions of section 40A(3) were not applicable.

Plan to avoid purchase of fish or fish product from any middleman.-

a. The expression ‘fish or fish products used in rule 6DD(e)(iii) would include other marine products such as shrimp, prawn, cuttlefish, squid, crab, lobster etc..

b. The producers’ of ‘fish or fish products for the purpose of rule 6DD(e) would include, besides the fishermen, any headman of fishermen, who sorts the catch of fish brought by fishermen from the sea, at the sea shore itself and then sells the fish or fish products to traders, exporters etc.

It is further clarified that the above exception will not be available on the payment for the purchase of fish or fish products from a person who is not proved to be a ‘producer‘ of these goods and is only a trader, broker or any other middleman, by whatever name called

In Orchid Marine v. ITO 2014 TaxPub(DTI 4022 (Coch-Trib), on facts of the case, since the fish was admittedly purchased from a person other than fisherman or producer, the exact role of that middle man has to be examined in view of Circular No. 10/2008, dt. 5- 12-2008

Where assessee purchased fish from fishermen or headman of fishermen which fell under exceptional circumstances as prescribed in rule 6DD(e), Tribunal was justified in holding that section 40A(3) was not attracted to facts of the case.- Vide CIT v. Blue Water Foods & Exports (P.) Ltd. 2015 TaxPub(DT) 1630 (Karn-HC).

Thus one should plan to purchase fish or fish product from producer himself instead of any middleman.

During the year ended 31/03/20, Geojit Marine Products Ltd. has made payment in cash to the tune of Rs. 60,000 on a single day to local fishermen, who regularly supply to them lobsters and crabs. Will such cash payments be hit by the provisions of section 40A(3) of the Income -tax Act, 1961? Will your answer be different, if such cash payments are made to a hawker who supplies lobsters and crabs?

CIRCULAR NO. 10/2008 fish or fish products‘ would include ‘other marine products such as shrimp, prawn, cuttlefish, squid, crab, lobster, etc.‘.

The ‘producers‘ of ‘fish or fish products‘ would include, besides the fishermen, any headman of fishermen, who sorts the catch of fish brought by fishermen from the sea, and then sells to traders, exporters, etc.

Circular No 6/2006: dt 06/10/2006 –exemption will not be given if (recipient) is not a producer of the goods.

Section 40A(3) will not hit if purchase from single person and value of each invoice is less than Rs 10000

If purchase is effected from a single person by way of several bills/invoices and if value of each bill/invoice is less than Rs. 10,000 then payments made to settle each bill/invoice would not be hit by provisions of section 40A(3), as each bill/invoice has to be considered as a separate contract Sec 40A(3) or 40A(3A) is in nature of permanent disallowance and it applies qua each expenditure. Therefore, for each expenditure one has to look at the payment or aggregate payment made in a day. For two different expenditure, if the payment is made to same person and if the payment is made in cash does not exceed the limit as prescribed qua each expenditure though cumulatively it exceeds, then no disallowance can be made. IN THE ITAT COCHIN BENCH Raja & Co. v. Deputy Commissioner of Income-tax, Central Circle, Trichur IT APPEAL NO. 534 (COCH.) OF 2011

Example: Mr. A purchases certain goods from Y Ltd. on credit on June 11, 2018 for Rs. 8,000, on June 29, 2018 for Rs. 7,000 and on July 10 2018 for Rs 9,000. The total payment of Rs. 24,000 is made by a crossed cheque on August 1, 2018.

Though the amount of payment exceeds Rs. 10,000, nothing shall be disallowed. To attract disallowance, the amount of bill as well as the amount of payment should be more than Rs. 10,000.

II. Disallowance of Depreciation section 43(1))

Disallowance of Depreciation where cash payment exceeding Rs. 10,000 is made for purchase of asset (Amendment to section 43(1))

Clause (1) of section 43 defines “actual cost” for the purposes of claiming depreciation

The cost in acquisition of any asset or part thereof in respect of which a payment or aggregate of payments made to a person in a day, otherwise than by an account payee cheque drawn on a bank or an account payee bank draft or use of electronic clearing system through a bank account, exceeds ten thousand rupees, such expenditure shall be ignored for the purposes of determination of actual cost

Certain Consequences because of amendment:

1.Asset or part thereof: Part may be in the nature of

2. Land is Non Depreciable asset hence this amendment will not trigger whatsoever.

3. What if the depreciable asset which was purchased in cash enters the block of the asset and only this asset remains and others are sold then, will Depreciation still be available on WDV of asset sold as asset bought in Cash still exists in block as per sec 50 of Act ?

~ The value of the block will be Nil

For Example: Mr.Joel has bought a Machinery from Mr.Jack worth Rs.30,000 by making cash payment on 20th Nov 2017.

EXAMPLE 1: Assessee purchases plant and machinery of Rs. 3,50,000 on 1.04.2020 and pays the entire amount in cash.

Since payment of Rs. 3,50,000/- is made by cash, it shall not be considered as part of actual cost of plant and machinery. The actual cost of plant and machinery shall be taken to be NIL and NIL shall be added to WDV of Block of assets. Note: As per section 269ST, the seller of machinery is liable to pay penalty of Rs. 3,50,000 for accepting cash of Rs.2,00,000 or more. The Penalty shall be under section 271DA.

EXAMPLE 2: Suppose in Example 1, assessee makes payments as under:

Therefore Rs. 3,25,000/- shall be considered as actual cost and Rs. 3,25,000/- shall be added to WDV of Block of assets.

Note: S. 43(1) defines original cost to mean actual cost of asset as reduced by portion of cost as met directly or indirectly by any other person or authority. FA, 2017 has inserted a second proviso to exclude expenditure incurred in acquisition of any asset or part thereof from actual cost of asset, if the payment in respect of such expenditure is made to a person in a day, exceeding Rs. 10,000 otherwise than by a specified mode.

Whether payments in respect of past expenditure to be included in cost?

The language of the second proviso is “where the assessee incurs any expenditure in respect of which payments or aggregate payments made to a person in a day exceed ten thousand rupees, such expenditure shall be ignored for the purposes of determination of actual cost.”

As stated above, the language employed in the amendment is “incurs”, signifying present tense and implying that it would apply to any expenditure which is incurred after the amendment is made effective, as per one view. As per the other view, it may also mean that both the event of incurring the expenditure and the payment thereof should be after the date on which the amendment is made effective. As per yet another review, it may mean that the expenditure may be incurred in past, that is, prior to the effective date of amendment, but, if the payment is made after the effective date of amendment, the provision would apply. Having regard to the provision, its language and the desire to be prospective, it appears that the first view or second view is preferable. The other view would require reworking of the actual cost in respect of the past and to what extent it should be done or not may be difficult as well as impractical.

Actual cost of asset in case of withdrawal of deduction in terms of section 35AD(7B) r/w 43(1):

Disallowance of Cash Payments under Section 35AD & Restrictions on Claim of Depreciation of Disallowed Capital Expenditure

As per the provisions of section 35AD investment linked deduction is available in respect of capital expenditure laid out for certain specified businesses. An amendment is has been made to curb the incurring of any expenditure in cash on such expenditure which is eligible for deduction under section 35AD and accordingly an expenditure of above Rs. 10,000/- in aggregate made to a person in a day shall not qualify for deduction under the provisions of the said section. It is to be noted that under the existing provisions of the Act revenue expenditure incurred in cash exceeding Rs. 10,000 is disallowed under section 40(A)(3) except in specific circumstances referred in Rule 6DD of Income Tax Rules, 1962. In order to discourage cash transactions even for capital expenditure ,the Act has been amended to clause (f) of Section 35AD(8) of Act whereby any capital expenditure in respect of which aggregate payment made to a person in a day otherwise then by account payee cheque, draft or ECS through bank account exceeding Rs. 10,000/- , same shall be disallowed.

Furthermore, as per the provisions of section 35AD(7B) if any asset, in respect of which deduction has been allowed earlier, is put to use for the purpose other than the specified business, then the expenditure allowed as reduced by depreciation calculated in terms of section 32, shall be added back to the income of the assessee in the year in which the asset is so used for purpose other than specified business. There was no clarity as to what would be the actual cost of such asset for the purpose of section 43. Accordingly, a proviso is being sought to be inserted toExplanation 13 in the section 43 in lines with the provisions of section 35AD(7B)which will provide that the actual cost of such asset shall be the actual cost to the assessee, as reduced by depreciation that would have been allowable if the asset had been used for such purpose (i.e for other than the specified business) since the date of its acquisition.

The above provisions can be summarized in the following manner:

- Capital Expenditure is required to be incurred in respect of which aggregate payment made to a person in a day otherwise then by account payee cheque, draft or ECS through bank account exceeding Rs. 10,000

- It is now provided that the Actual cost where deduction was allowed under section 35AD This proviso will revive the actual cost if section 35AD(7B) is revoked and thereby previous deduction are withdrawn.

- Capital asset in respect of which deduction allowed under 35AD is deemed to be the income of the assessee as per 35AD(7B)

- The actual Cost of the asset to the assessee shall be the actual cost as reduced by an amount equal to the amount of depreciation calculated at the rate in force that would have been allowable had the asset been used for the purpose of business.

III. Applicabilty of disallowance u/s 40A of the Act in case assessee opts for presumptive taxation u/s 44AD

Sec 40A relates to disallowance related to excess payment of related party, cash payment to a person in excess of Rs. 10,000 in a day, payment to unapproved fund, mark to market losses etc. The comparison of sec 44AD and 40A is very interesting and different from sec 43B and sec 40. Sec 40A overrides all the other provisions of PGBP.

The section begins with ―The provisions of this section shall have effect notwithstanding anything to the contrary contained in any other provisions of this Act relating to the computation of income under the head ―Profits and gains of business or profession‖. The non-obstante clause of this section seems to override provisions of sec 44AD. However, the Panaji Tribunal in case of Good Luck Kinetic v. ITO (2015) 58 relating to disallowance u/s 43B have considered two points:

i. Amplitude of non-obstante clause

ii. Payment to crown i.e statutory dues

The provisions of sec 40A are not related to statutory dues and such other dues. It just imposes restrictions on payments and disallows amount which is not paid as per the provisions of the Act. It is also to be noted that provisions of sec 40A of the Act are with regard to allowability of expenditure which has been actually incurred and claimed by the assessee from sec 30 to 38 of the Act. Therefore, if the assessee declares income as per the provisions of sec 44AD of the Act, no disallowance shall be made u/s 40A of the Act.

Example : If any person opting for sec 44AD has made cash purchases worth Rs. 15,000 no disallowance can be made u/s 40A(3), even if the cash payment to a person exceeds Rs. 10,000 in a day. Cash payment to transporter in excess of Rs. 35,000 in a day shall not be disallowed.

Similarly, disallowance u/s 40A for excess payment to relatives cannot be made. No addition u/s 41 can be made.

Incentives to encourage cashless business transactions

A. Presumptive Rate of Income:

The presumptive rate of income would be 8% of total turnover or gross receipts.

However, Proviso to sub-section (1) provides that the presumptive rate of 6% of total turnover or gross receipts will be applicable in respect of amount which is received

By and account payee cheque or

By an account payee bank draft

By use of electronic clearing system through a bank account OR through such other electronic mode as may be prescribed.

During the previous year or before the due date of filing of return under section 139(1) in respect of the previous year.

However the assessee can declare in his return an amount higher than presumptive income so calculated, claimed to have been actually earned by him.

√ Other Electronic Prescribed by CBDT: The Central Board of Direct Taxes has prescribed other electronic modes to provide for the followings as an acceptable electronic mode of payments-

(a) Credit Card;

(b) Debit Card;

(c) Net Banking;

(d) IMPS (Immediate Payment Service);

(e) UPI (Unified Payment Interface);

(f) RTGS (Real Time Gross Settlement);

(g) NEFT (National Electronic Funds Transfer), and

(h) BHIM (Bharat Interface for Money) Aadhaar Pay‖

Example: Mr. Arshdeep Singh, an individual carrying business of laptops has a Turnover of Rs. 80 Lakhs during the F.Y. 19-20. He has received the payments as

Rs.60 Lakh in cash

Rs.10 Lakh by account payee cheque during the previous year Rs. 4 Lakh by ECS through bank account upto 31st July 2019 Rs. 6 Lakh has not been received yet.

Now, since the TO is below Rs.2 Cr, he has the option of availing benefits of section 44AD. Mr. Arshdeep Singh can exercise this option and declare income as

8% of Rs.66,00,000 (60 Lakh + 6 Lakh) – 5,28,000

6% of Rs. 14 Lakh (10 Lakh + 4 Lakh) – 84,000

Total income from PGBP = 6,12,000

B. Combined Study of Section 44AB with Section 44AD’

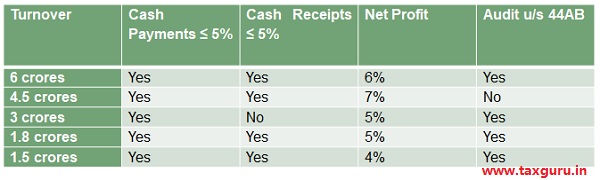

Currently, businesses having turnover of more than one crore rupees are required to get their books of accounts audited by an accountant. In order to reduce the compliance burden on small retailers, traders, shopkeepers who comprise the MSME sector, the Finance Act 2020 has raised the limit of audit by five times the turnover threshold for audit from the existing Rs. 1 crore to Rs. 5 crores. It is also to be noted that this amendment is applicable for F.Y. 2019-20 i.e for the A.Y. 2020-21

Further, in order to boost less cash economy, it has been provided that the increased limit for mandatory tax audit shall apply only to those businesses which carry out less than 5% of their business transactions in cash. But in this connection, following points are to be noted

1. This threshold limit for the applicability of mandatory tax audits is applicable to business entity only and limit for a professional assessee shall continue to be at Rs. 50 lacs even if he receives entire consideration in non-cash mode.

2. It is not provided that who will certify the margin of transactions in cash mode of 5 It appears that the assessee is himself requiring declaring the percentage of receipt in cash mode and non-cash mode.

3. The provision to increase the turnover limit for a mandatory tax audit is amended to benefit the MSME sector.

4. The amendment is carried out only in section 44AB. No amendment is made in section 44AD and thus the turnover limit of Rs. 2 crores shall continue. Suppose an assessee is having a turnover of 180 lacs for the financial year 2020-21 and all the transactions of business are by non-cash modes. The net profit of the assessee is Rs.7 lacs which is less than 6% of turnover of the assessee. Now as per the provisions of sec 44AD, the assessee is required to maintain books of account and get them audited u/s 44AB of the Act.

5. The term ‘aggregate of all receipts and aggregate of all payments‘ is very wide and covers not only the receipts and payments on account of turnover or sales but all other business transactions. Capital introduction, receipt and repayment of a loan, etc., partners‘ drawings, payment of freights, etc. Even payment of taxes made in cash will come within the purview of cash transactions. It can be better understood with the help of following table.

IV. Restrictions on Loans, Deposits & Advances

IV. Restrictions on Loans, Deposits & Advances

Analysis of Sec.269SS of the Act

This section was introduced in the Act with the objective that Unaccounted cash found in the course of searches carried out by the Income-tax Department is often explained by taxpayers as representing loans taken from or deposits made by various persons. Unaccounted income is also brought into the books of account in the form of such loans and deposits and taxpayers are also able to get confirmatory letters from such persons in support of their explanation. With a view to countering this device, which enables taxpayers to explain away unaccounted cash or unaccounted deposits, the Finance Act has inserted a new section 269SS.

Provision:

No person shall take or accept from any other person, any loan or deposit or any specified sum1 , otherwise than by an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account, if

the amount of such loan or deposit2or specified sum or the aggregate of the loan or deposit or specified sum is twenty thousand rupees or more or

On the date of taking or accepting such loan or deposit or specified sum, any loan or deposit or specified sum accepted earlier by such person from the depositor is remaining unpaid (whether repayment has fallen due or not) is Rs.20,000/- or more or

The aggregate amount of loan or deposit or sum specified along with the amount loan or deposit or sum specified taken earlier which is outstanding on the date on which loan or deposit is to be taken is Rs. 20,000/- or more.

Exemption from Sec 269SS:

This section applies to all the persons i.e. individual, HUF, Company, Partnership firm, AOP/BOI, Local authority, Co-operative society, Trust, AJP.

The provisions of this section are not applicable in cases

1. Where the following persons are either recipient or payer:

a) Government ;

b) any banking company, post office savings bank or co-operative bank ;

c) any corporation established by a Central, State or Provincial Act ;

d) any Government company as defined in section 617 of the Companies Act, 1956 (1 of 1956) ; e)such other institution, association or body or class of institutions, associations or bodies which the Central Government may, for reasons to be recorded in writing, notify in this behalf in the Official Gazette : {Notified by F. No.414/104/84-IT (INV)- Housing Development Finance Corporation Limited, Bombay, in respect of its Home Savings Plan Scheme, Loan Linked Deposit Scheme and Certificate of Deposit Scheme, including Cumulative Interest Scheme}

2. Where the payer of loan or deposit and the recipient are both having agricultural income and neither of them has any income chargeable to tax under the Act.

Example (a) Where X had accepted a loan from XYZ on 1st of June 19 by crossed cheque for Rs 19,000. on 15th April 2020 X takes another loan from XYZ for Rs 2000 in cash (the earlier loan remaining unpaid on the date)

Then since the combined loan outstanding (20,000 + 2,000) = 21,000 is more than or equal to 20,000 the provisions of Sec 269SS will be attracted if the new loan on 15th April is taken in cash.

Example (b) Where X had accepted a loan from XYZ on 1st of June 19 by crossed cheque for Rs 19,000. He had repaid 3,000 in cash on 3rd Aug 2019. On 15th April 2020 X takes another loan from XYZ for Rs 2000 in cash (the earlier loan remaining unpaid on the date)

Then since the combined loan outstanding(19,000 – 3,000 + 2,000) = 18,000 is not more than or equal to 20,000 the provisions of Sec 269SS will not be attracted even if the new loan on 15th April is taken in cash

Example (c) If X accepts a loan of Rs 10,000 in cash from Y and a deposit of Rs 15,000 in cash from Z ...then there is no violation of the provisions of Sec 269SS as the amount does not more than or equal to 20,000 from one person

Example (d) if X takes a loan of Rs 12,000 in cash from Y on 12th of Dec 2019 and accepts a further loan of Rs 9,000 from Y by Account payee cheque, Since the new loan is by a mode of prescribed there is no violation of the provisions of Sec 269SS

Example:

Mr. Rohit had borrowed a loan of Rs. 14,000 from Mr. X as on 01 .09.2018 in form of account payee cheque and the same is still payable as on 20.12.2019 amounting to Rs 18,000 (Including interest). Also he has borrowed Rs. 7,000 as Deposit in cash as on 20.12.2019, whether there is any contravention to section 269SS?

As per Section 269SS (b), as on the date of taking or accepting loan or deposit or specified sum, if there is any loan or deposit or specified sum accepted earlier is remaining unpaid then the same should be considered for Rs 20,000/- limit. In the instant case, as the amount exceeds 20,000/- (18000 + 7,000 = 25,000/-) there is a contravention

Penalty for failure to comply with section 269SS:

As per Section 271 D of the Income tax act, 1961 if a person fails to comply with Section 269SS then the Joint Commissioner shall charge a sum by way of penalty equal to the amount of the loan or deposit or specified sumso taken or accepted.

Meaning of specified sum

The term ‘Specified sum‘ was added by Finance Act, 2015 w.e.f 01.06.2015 by amending the provisions of section 269SS and 269T of the Act, which means any sum of money receivable, whether as advance or otherwise in relation to transfer of immovable property irrespective of whether or not the transfer has taken place. It is without any doubt that the applicability of Section 269SS of the Act is not limited to only cash transactions relating to immovable properties which have been held as capital asset but also to those immovable properties which are not capital asset, thus, definition of ‘transfer‘ as specified in Section 2(47) cannot be said to be considered for the purposes of Section 269SS. Here, the expression ‘transfer‘ will have to be understood as under the Transfer of Property Act, 1882. Also, the term ‘Immovable Property‘ has not been defined anywhere. It does not matter whether immovable property is capital asset or stock in trade or whether it is rural agricultural land or urban land. It could be any land or any property. However, as per the second proviso to Section 269SS, where both the depositor as well as the receiver are having agricultural income and are not in receipt of any other taxable income, Section 269SS will have no application.

Normally, as per the provisions of Section 269SS, a person cannot receive advances for sale of immovable property of Rs. 20,000 or more in cash. Any person who is found to have received advance cash of Rs. 20,000 or more in respect of consideration for sale of property would be liable to penalty under section 271 D of the Act. However, the question that arises here is whether this position would continue to apply even where the sale consideration paid as cash advance has been subjected to TDS under Section194-IA of the Act.

The proviso to sec provides ―Provided further that the provisions of this section shall not apply to any loan or deposit or specified sum, where the person from whom the loan or deposit or specified sum is taken or accepted and the person by whom the loan or deposit or specified sum is taken or accepted, are both having agricultural income and neither of them has any income chargeable to tax under this Act.‖ It specifies that acceptance of deposit/ loan /specified sum shall not attract provisions of sec 269SS where both the parties are agriculturists and both have income below basic exemption limit

Example: Mr. Lal Singh purchased an agriculture land for Rs. 1,80,000 in cash from Mr. Nijjar Singh. Both of them are agriculturists and none of them have income exceeding the basic exemption limit. Whether sec 269SS be applicable on them and whether penalty u/s 271 D will be imposed on them?

Whether the answer will remain same if the land is other than agriculture land? Whether the answer will remain same if land is purchased for Rs. 5,00,000?

Answer: Sec 269SS deals with receipt of specified sum. Explanation to the section provides the meaning of specified sum” means any sum of money receivable, whether as advance or otherwise, in relation to transfer of an immovable property, whether or not the transfer takes place.‖ It covers not only advance related to immoveable property, but also money received at time of transfer of property.

However, as both Mr. Lal Singh and Mr. Nijjar Singh are agriculturists and both have income below basic exemption limit, sec 269SS shall not be applicable on them. Mr. Nijjar Singh have received ‘specified sum‘ other than account payee cheque/ draft or ECS. But this will not amount to violation of sec 269SS and hence, penalty u/s 271 D shall not be imposed.

The answer would remain same even if the land is other than agriculture land because the exemption provided is not related to type of property. Rather, the exemption is for the agriculturists. Therefore, sec 269SS will not be applicable in this case.

If the consideration for the land is Rs. 5,00,000 the answer will still remain same. However, in this case sec 269ST will be applicable. Sec 269ST provides that

Provided that the provisions of this section shall not apply to—

(ii) Transactions of the nature referred to in section 269SS;

Sec 269ST is not applicable on the transactions which are covered by sec 269SS. The transaction between two agriculturists who are having income below taxable limit is not covered by sec 269SS and hence sec 269ST shall be applicable on it.

As cash received by Mr. Nijjar singh exceeds Rs. 2,00,000, provisions of sec 269ST are violated. Penalty amounting to Rs. 5,00,000 shall be imposed u/s 271 DA.

Provisions of Section 269T

Mode of repayment of certain loans or deposits.

Applicability:

This section applies to all the persons i.e. individual, HUF, Company (including branch of the banking company), Partnership firm, AOP/BOI, Local authority, Co-operative society, Trust, AJP.

Provision:

The repayment, by any person, of any loan or deposit3 or specified advance 4, made with it, should not be done in any mode apart from account payee cheque or account payee bank draft drawn in the name of the person or by use of electronic clearing system through a bank account who has made the loan or deposit, if:

1. The amount of loan or deposit or specified advance along with any interest, if any payable on such loans or deposit is Rs. 20,000 or more or

2. As on the date of repayment, if there exists any other loan or deposits held by the person either in his own name or jointly with any other person, the aggregate amount of such loans or deposit together with interest, if any payable on such loans or depositis Rs. 20,000 or more or

3. In case of specified advances received by such person either in his own name or jointly with any other person, the aggregate of such specified advances along with any interest payable on such specified advances is Rs. 20,000 or more

The repayment made by a branch of a banking company or co-operative bank, of such loan / deposit, can also be made by crediting the amount to the savings bank account or to the current bank account held with the branch.

Cases where the above provisions do not apply:

The provisions of this section does not apply to in case the loan / deposit has been taken / made by the following persons:

Government;

any banking company, post office savings bank or cooperative bank;

any corporation established by a Central, State or Provincial Act;

any Government company as defined in section 617 of the Companies Act, 1956 (1 of 1956) ;

such other institution, association or body or class of institutions, associations or bodies which the Central Government may, for reasons to be recorded in writing, notify in this behalf in the Official Gazette.

Example. XYZ Ltd. had deposited of Rs. 18,500 from Mr. Arshdeep. During the previous year 2017-1 8, such deposit has become due for repayment (Interest payable Rs. 3100). XYZ Ltd repaid such amount by way of bearer cheque.

The provision of section 269T shall be made applicable if amount to be repaid (together with interest) exceeds Rs. 20,000. In this case,XYZ Ltd. had repaid Rs. 21,600 otherwise than by account cheque or draft or ECS, there is a clear violation of provisions of section 269T.

Example. XYZ Ltd had accepted deposited of Rs. 12000 from Mr. Singh on 01-05-2015 for a period of two year (Rate of interest 12% p.a. payable annually). It further accepted deposit of Rs. 15,000 (Rate of interest 10% p.a payable annually). Date of second deposit was 01-06-2016. On 01-05-2017, XYZ Ltd repaid Rs.16,800 (together with interest) towards first deposit in cash. XYZ Ltd also repaid Rs. 16,500 (together with interest) toward first deposit in cash. XYZ Ltd. also repaid Rs. 16,500 towards second deposit on 03-05-2017 in cash.

Does your answer differ in point no. (b) Above, if second deposit of Rs. 15,000 was in a joint name of Mr. & Mrs. Singh

The provision of the section 269T shall be made applicable if aggregate amount of deposits held by a person together with interest exceeds Rs.20,000 . Therefore, at the time of repayment of first deposit in cash, there is a violation of provision of section 269T since aggregate deposits together with interest exceeded Rs. 20,000.

However, there is no violation of section 269T by XYZ Ltd. at the time of repayment of second deposit in cash since neither the amount of deposit with interest nor the aggregate amount deposit held by Mr. Singh on that date together with interest exceeds the threshold limit of Rs. 20,000.

The answer will not differ because the law mentioned under section 269Tis applicable even if deposits are held in joint name with other person.

Example(i) Mr. A, an individual, has deposited Rs.15,000 on 1st May, 2019 for 48 months by bearer cheque and another Rs.15,000 on 30th June, 2019 in cash to purchase a new certificate of 48 months tenure.

(ii) Mr. A has applied for premature withdrawal against both the certificates and the company has paid him Rs.16,500, by a bearer cheque, against principal and interest on 23rd March, 2020, due against his first certificate (purchased in 2019) and Rs.15,500 in cash on 25th March, 2020, against the second certificate.

Fearless General Finance & Investment Limited, a residuary non-banking company, accepts public deposits, issues deposit certificate and repays the same after some period of time alongwith interest, under different schemes run by it.

Following transactions were noted from their books of account:

Discuss the violation of income tax provision, if any, and consequential penalty for each transaction. Will it make any difference if the certificates were held jointly with Mrs. A, wife of Mr. A, while repaying back in cash or bearer cheque?

i. There is no violation of section 269SS at the time of acceptance of the first deposit of Rs.15,000 on 1.5.2019, since it is not in excess of the threshold limit of Rs.20,000. However, violation under section 269SS is attracted at the time of acceptance of the second deposit in cash on 30th June, 2019, since as on that date, there is already an outstanding deposit of Rs.15,000 and another cash deposit of Rs.15,000 would take the aggregate to Rs.30,000, which exceeds the threshold limit of Rs.20,000. Therefore, penalty under section 271 D of a sum equal to the amount of deposit taken from Mr. A is attracted for failure to comply with the provisions of section 269SS.

ii. In this case, there is a violation of the provisions of section 269T at the time of first repayment by bearer cheque on 23rd March, 2020, since on that date, the aggregate amount of deposits held by Mr. A with the non-banking company (together with interest payable on such deposits) is more than Rs.20,000. Therefore, penalty under section 271 E equal to the amount of deposit so repaid will be attracted for failure to comply with the provisions of section 269T. However, the second repayment of Rs.15,500 on 25th March, 2020 in cash cannot be considered as a violation of section 269T, since neither the amount of deposit with interest thereon nor the aggregate amount of deposits held by Mr. A on that date together with interest exceeds the threshold limit of Rs.20,000. The provisions of section 269T will be attracted even if the certificate is being held by Mr. A in joint name with his wife.

Penalty for failure to comply with section 269T:

As per Section 271 E of the Income tax act, 1961 if a person fails to comply with Section 269T then the Joint Commissioner shall charge a sum by way of penalty equal to the amount of the loan or deposit or specified sum so repaid.

Example:

Mr. A holds the following accounts with ABC Ltd, a banking company:

Account 1: FD of Rs. 10,000; interest payable Rs. 1,250

Account 2: FD of Rs. 8,750 interest payable Rs. 1,120

ABC Ltd repays the amount of FD along with the applicable interest payable on such FD to Mr. A, in a mode other than account payee cheque or account payee bank draft. Will there be any contravention of the provisions of section 269T?

On a plain understanding of the section, one would assume that since only Rs. 11,250 is being paid to Mr. A.

1234

V. Restrictions on Cash Transactions in Real Estate

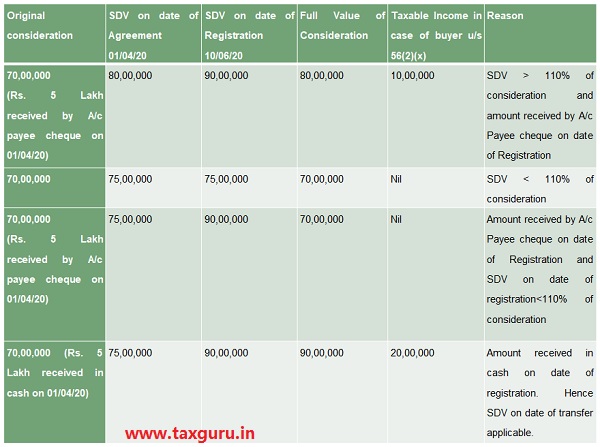

♦ Stakes in transactions in immovable properties are quite high and so are the tax implications. It is not only perceived but an open secret in India that sale transactions of immovable properties are undervalued leading to leakage of tax revenue causing losses to the Government and unaccounted money is not good for the health of the society in general. Therefore, the restlessness on the part of Government to plug such leakage and attempts by assessees and tax professionals to avoid hardships to genuine assessees. The provisions of Sec 50C,sec 43CA and sec 56(2)(x) of the Income Tax Act, 1961 specifically dealing with transactions in immovable properties have been inserted in the Act. As per the provisions of these sections, if any immovable property is sold below the stamp duty value (or circle rate) then such case will fall under Section 50C, Section 43CA, Section 56(2)(x) and double taxation shall apply on the difference in the stamp duty value and transfer price in the hands of seller and buyer. In the existing framework of the Income Tax Act, for the same income or rather the deeming income, both the seller and the buyer of land and/or building, are being taxed and as such the pressing of service of such deeming fiction of taxation both in the hands of the seller and/or buyer of land and/or building is resulting in “Double Taxation”.

♦ Under the provisions contained in Section 50C and sec43CA, in case of transfer of a capital asset/stock in trade being land or building or both, the value adopted or assessed by the stamp valuation authority for the purpose of payment of stamp duty shall be taken as the full value of consideration for the purposes of computation of capital gains. These provisions have further been ammended to provide relief to the seller who has entered into an agreement to sell the property much before the actual date of transfer of the immovable property and the sale consideration is fixed in such agreement. The government has amended the provisions of section 50C/43CA so as to provide that where the date of the agreement fixing the amount of consideration for the transfer of immovable property and the date of registration are not the same, the stamp duty value on the date of the agreement may be taken for the purposes of computing the full value of consideration. It is further proposed to provide that this provision shall apply only in a case where the amount of consideration referred to therein, or a part thereof, has been paid by way of an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account, on or before the date of the agreement for the transfer of such immovable property.

Taxability in the hand of Seller

If the immovable property is considered as a capital asset-

As per Section 50C, if a capital asset, being land or building or both, is transferred for a consideration below the stamp duty value, then such stamp duty value shall be the deemed value of the consideration for the purpose of calculating capital gain under Section 48. The original consideration paid for the transfer shall not be considered for the purpose of capital gain in the hands of the seller.

However, if the date of an agreement fixing the amount of consideration and the date of registration for the transfer of the capital asset is different then the stamp duty value as on date of agreement may be taken for the purpose of computing full value of consideration. Provided that the amount of consideration or a part thereof has been received by way of an account payee cheque or account payee draft or use of electronic clearing system through a bank account or through such other electronic mode as may be prescribed, on or before the date of the agreement for transfer.

Finance Act 2020 (applicable from A.Y. 2021-22) has amended the applicability of Section 50C only in those cases where the stamp duty value exceeds one hundred and ten percent (earlier 105%) of the consideration so received or accrued for the transfer of capital asset, being land or building or both.

If the immovable property is considered an asset other than capital asset such as stock in trade-

As per section 43CA, if an asset (other than a capital asset), being land or building or both, is sold below the stamp duty value then such stamp duty value shall be deemed value of the consideration and used for the purpose of computing profit and gains from transfer of such assets.

Finance Act 2020 (applicable from A.Y. 2021-22) has amended the applicability of Section 43CA only in those cases where the stamp duty value exceeds one hundred and ten percent (earlier 105%) of the consideration so received or accrued for the transfer of an asset (other than a capital asset), being land or building or both.

Also, if the date of an agreement fixing the amount of consideration and the date of registration for the transfer of an asset is different then the stamp duty value as on date of agreement may be taken for the purpose of computing full value of consideration

Provided that the amount of consideration or a part thereof has been received by way of an account payee cheque or an account payee bank draft or by use of electronic clearing system through a bank account or through such other electronic mode as may be prescribed on or before the date of agreement for transfer of the asset.

Reference to the valuation officer (available to the seller in both option mentioned above)

Where assessee claims before any Assessing Officer that the stamp duty value exceeds the fair market value of the property as on the date of transfer and such stamp duty value has not been disputed in any appeal or revision or no reference has been made before any other authority, court or the High Court, the Assessing Officer may refer the valuation of the asset to a Valuation Officer.

If the value assessed by Valuation officer is lower than the stamp duty value, the assessed value shall be considered as the deemed sale price.

If the value assessed by Valuation officer is higher than the stamp duty value, the stamp duty value remains deemed sale price.

So, if the reference is made to the Valuation officer then it may be possible that the stamp duty value may decrease but it cannot be increased on the basis of the valuation officer.

Taxability in the hand of buyer

As per Section 56(2)(x), if any person receives an immovable property for a consideration which is less than stamp duty value of the property and such excess is more than:-

the amount of fifty thousand rupees and

the amount equal to ten percent (earlier 5%) of the consideration then stamp duty value of such property as exceeds such consideration shall be taxable as income in the hands of buyer and chargeable under the head Income from Other Sources.

Section 56(2)(x) shall not apply to any property received:-

from any relative; or on the occasion of the marriage of the individual; or

under a will or by way of inheritance

Where the date of an agreement fixing the value of the consideration for the transfer of the asset and the date of registration of the transfer of the asset are not same, the stamp duty value may be taken as on the date of the agreement for transfer and not as on the date of registration for such transfer. However, this exception shall apply

only in those cases where amount of consideration or a part thereof for the transfer has been paid by way of an account payee cheque or an account payee bank draft or by use of electronic clearing system through a bank account or through such other electronic mode as may be prescribed, on or before the date of the agreement for transfer of such immovable property:

Note:- Similar option of referencing to valuation officer (as available under Section 50CA) is also available to the assessee.

Where there is decrease in stamp duty value on date of registration as compared to stamp duty value on the date of agreement

In case stamp duty value as on date of registration has decreased from the stamp duty value as on date of agreement, it would be beneficial to the assessee to adopt the stamp duty value as on date of registration. The word used in this section 43CA, 50C and 56(2)(x) is “may”.

“Where the date of agreement fixing the value of consideration for transfer of the asset and the date of registration of such transfer of asset are not the same, the value referred to in sub-section (1) may be taken as the value assessable by any authority of a State Government for the purpose of payment of stamp duty in respect of such transfer on the date of the agreement.”

Further the Ahmedabad Bench of ITAT in case of Dharamshibhai Somani v. ACIT has made the following observations which are to the effect that the amendment is optional to the assessee – “The amendment in Section 50C was brought in to provide relief to the assessee in a situation in which the stamp duty valuation of a property has risen between the date of execution of agreement to sell and execution of sale deed, as is the norm rather than exception, but the real estate market is now traversing through a difficult phase and there can be situations in which there is a fall in the stamp duty valuation rates with the passage of time. Such a situation has actually arisen in many places in the country, such as in Gurgaon, New Delhi and even in Dehradun and some other places. It is therefore possible that, at first sight, first proviso to Section 50C may seem to work to the disadvantage of the assessee in certain situation in the event of the word `may’ being construed as mandatory in application, but then one cannot be oblivious to the fact that this proviso states that “the value adopted or assessed or assessable by the stamp valuation authority on the date of agreement may be taken for the purposes of computing full value of consideration for such transfer (emphasis supplied)” making it clearly optional to the assessee and that in any event, what has been brought by the lawmakers as a measure of relief to the taxpayers cannot be construed as resulting in a higher tax burden on the tax payers”

Therefore, it is not mandatory for assessee to adopt stamp duty value as on date of agreement even if payment is by specified mode. The law has given option to the assessee and has not made it mandatory to take value as on date of agreement. It may be concluded that the assessee can take lower of the stamp duty values as assessable value, provided it is not lower than the actual consideration.

Applicability of Stamp Duty Value on the Date of Agreement, when Earnest Money is Received by Book Adjustments

The provisions of sec 50C and sec 43CA clearly provide that if an assessee intends to adopt stamp duty value as on date of agreement, amount of consideration should be received by way of an account payee cheque or account payee bank draft or by use of electronic clearing system through a bank account or through such other electronic mode as may be prescribed, on or before the date of the agreement. The payment by book adjustment or journal entry is not as per the specified modes. Therefore, where the consideration on or before date of agreement is received by book adjustment, the benefit of adoption of stamp duty value on date of agreement cannot be availed. In case where the seller of the property receives another property in consideration and payment is not received by account payee cheque/ account payee bank draft/ ECS, the benefit of adoption of stamp duty value on date of agreement u/s 50C, 43CA and 56(2)(x) of the Act shall not be available.

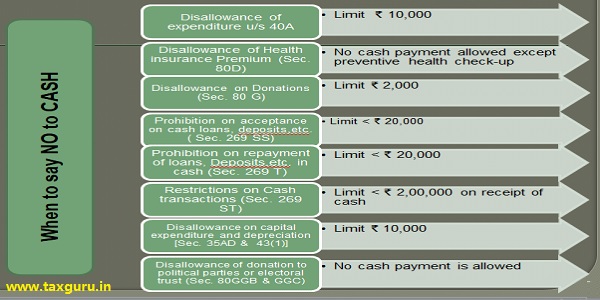

VI. Restrictions on Income Tax Deductions in case of Cash Payment

i. Deduction in respect of health insurance premia under Section 80D

Analysis of Section 80D

In case of an Individual

(a) Deduction in respect of insurance premium paid for family: A deduction to the extent of ₹ 25,000 is allowed in respect of the following payments-

(1) premium paid to effect or keep in force an insurance on the health of self, spouse and dependant children or

(2) any contribution made to the Central Government Health Scheme or

(3) such other health scheme as may be notified by the Central Government. Contributory Health Service Scheme of the Department of Atomic Energy has been notified by the Central Government.

(b) Deduction in respect of insurance premium for parents: A further deduction up to ₹ 25,000 is allowable to effect or to keep in force an insurance on the health of parents of the assessee. There is no difference that parents are dependent or not.

Quantum of deduction in case of senior citizen: An increased deduction of

₹ 50,000 (instead of ₹ 25,000) shall be allowed in case any of the persons mentioned above is a senior citizen /.e., an individual resident in India of the age of 60 years or more at any time during the relevant previous year.

(c) Deduction in respect of payment towards preventive health check-up:

Section 80D provides that deduction to the extent of ₹ 5,000 shall be allowed in respect payment made on account of preventive health check-up of self, spouse, dependant children or parents made during the previous year. However, the said deduction of ₹ 5,000 is within the overall limit of ₹ 25,000 or 50,000), specified in (a) and (b) above.

(d) Deduction for medical expenditure incurred on senior citizens: As a welfare measure towards i.e., person of the age of 60 years or more and resident in India, who are unable to get health insurance coverage, deduction of upto would be allowed in respect of any payment made on account of medical expenditure in respect of a such person(s), if no payment has been made to keep in force an insurance on the health of such person(s)

Though medical expenditure is not defined anywhere in the Act, but going by the motive, medical expenditure should cover every medical expense whether or not these expenditure are covered under any health insurance policy. Therefore, you can say that expenses such as consultation fees, medicines, hearing aids and so on can be claimed as deduction.”

“Senior citizen” means an individual resident in India who is of the age of 60 years or more at any time during the relevant previous year.

(e) Mode of payment: For claiming such deduction under section 80D, the payment can be made:

(1) by any mode, including cash, in respect of any sum paid on account of preventive health check-up;

(2) by any mode other than cash, in all other cases.

It is to be noted that only cash payment can be made in cash for preventive health checkup. No other cash payment is being allowed to avail deduction u/s 80D of the Act. It is further to be noted that no cash payment is allowed even in case of medical expenditure incurred for senior citizen.

In case of a HUF

Deduction under section 80D is allowable in respect of premium paid to insure the health of any member of the family. The maximum deduction available to a HUF would be ₹25,000 and in case any member is a senior citizen, ₹ 50,000.

Further, the amount paid on account of medical expenditure incurred on the health of any member(s) of a family who is a would qualify for deduction subject to a maximum of 50,000) provided no amount has been paid to effect or keep in force any insurance on the health of such person(s).

Other conditions

The other conditions to be fulfilled are that such premium should be paid by any mode, other than cash, in the previous year out of his income chargeable to tax. Further, the medical insurance should be in accordance with a scheme made in this behalf by –

(a) the General Insurance Corporation of India and approved by the Central Government in this behalf; or

(b) any other insurer and approved by the Insurance Regulatory and Development

Deduction where premium for health insurance is paid in lump sum [Section 80D(4A)]

(a) Appropriate fraction of lump sum premium allowable as deduction: In a case where mediclaim premium is paid in lumpsum for more than one year by:

(1) an individual, to effect or keep in force an insurance on his health or health of his spouse, dependent children or parents; or

(2) a HUF, to effect or keep in force an insurance on the health of any member of the family, then, the deduction allowable under this section for each of the relevant previous year would be equal to the appropriate fraction of such lump sum payment.

Example:

Rohan is aged 45 years, and his father is aged 75 years. Rohan has taken a medical cover for himself and his father for which he pays insurance premium of Rs 30,000 and Rs 35,000 respectively. What would be the maximum amount he can claim by way of a deduction under Section 80D?

Ans: Rohan can claim up to Rs 25,000, for the premium paid on his policy.

As for the policy taken for his father, who is a senior citizen, Rohan can claim up to Rs.50,000. In the given case, the deduction is Rs 25,000 and Rs 35,000. Therefore, the total deduction that he can claim for the year is Rs 60,000

♦ *Family members includes individual, his/her spouse and dependent children.

♦ *Parents may be dependent or not. But it does not include father-in-law / mother-in-law.

♦ *.In case any of the persons specified above (i.e. husband, wife, father, mother) is a senior citizen (i.e. 60 years or more) and Mediclaim Insurance premium is paid for such senior citizen, deduction amount is Rs. 50,000. If father is of 62 years and mother is of 58 years, the benefit of senior citizen will be available.

♦ * In case a non-resident is of age 60 years or above, he shall not get benefit of enhanced deduction of Rs. 50,000.But if father is a non- resident senior citizen and mother is a resident senior citizen, the benefit of Rs.50000/-will be allowed. Any of two must be a resident senior citizen.

♦ * The aggregate payment on account of preventive health check-up of self, spouse, dependent children, father and mother cannot exceed Rs. 5,000.

♦ ** Medical Expenditure is allowed if no amount has been paid towards health insurance of such person

Can you get deduction u/s 80D of Mediclaim policy for Overseas Journey?

Deduction for policy for overseas travel can be taken. There is nothing in the provision u/s 80D which prohibits claim of deduction u/s 80D for medical insurance for overseas journey. The only requirement, as given in section 80D(5) is that the insurance companies issuing such overseas insurance should be one of these

(5) The insurance referred to in this section shall be in accordance with a scheme made in this behalf by

(a) the General Insurance Corporation of India formed under section 9 of the General Insurance Business (Nationalisation) Act, 1972 (57 of 1972) and approved by the Central Government in this behalf; or

(b) any other insurer and approved by the Insurance Regulatory and Development Authority established under sub-section (1) of section 3 of the Insurance Regulatory and Development Authority Act, 1999 (41 of 1999).

ii. Section 80GGA

Donations for scientific research or rural development An Assessee (other than an assessee whose Gross Total Income includes income chargeable under the head ―profits and gains of business or profession‖) is entitled to deduction in respect of certain donations for scientific, social or statistical research or rural development programme or for carrying out an eligible project or National Urban Poverty Eradication Fund. Such donation can be given in cash, or by cheque or draft.

However, no deduction is allowed in respect of cash transaction/contribution exceeding Rs.10,000 (Rs. 2,000 w.e.f 01/06/2020)

iii. Section 80GGB

Donations by Indian company to political parties / electoral trust Any sum contributed by an Indian company to any political party or an electoral trust is not allowed as deduction while computing taxable income in respect of any sum contributed by way of cash.

iv. SECTION 80GGC

Section 80GGC of the Act provides for the benefit of those who make donations to political parties. There are certain conditions and criteria which have to be followed by the individual for the said benefits. Section 80GGC specifies the deduction under the Income Tax Act which is allowed from the total gross income of specified assessees for the contributions made to a political party or an electoral trust. This entire amount is eligible for tax deduction provided that it is not deposited in cash, but rather by other means.

Analysis of sec 80GGC of the Act

The objective of the Section was mainly to allow for transparency in the electoral funding and therefore, trying to make it corruption-free. Moreover, it also encourages more voluntary contributions towards the political parties by taxpayers.

The tax deductions are made only to specified assessees

The deduction falls under the Chapter VI-A deductions, which implies that the total amount which can stand for the tax deduction cannot be more than the total taxable income.

What is the eligibility criteria u/s 80GGC?

Section 80GGC can be claimed by any person except any local authority or artificial juridical persons who are wholly or partly funded by the government. The following groups are specified under the Section 80GGC to make the political contribution- an individual, a Hindu Undivided Family (HUF), a firm, an AOP or BOI and an Artificial Juridical Person. The last candidate in the list should not be funded by the

The tax deduction benefits can also be availed by making donations to multiple political parties rather than only one.

Deduction limit- While the entire contribution is eligible for the deduction, it should be made sure that the mode for the donation should never be in cash.

v. SECTION 80JJAA

(i) Quantum and period of deduction:

Where the gross total income of an assessee to whom section 44AB applies, includes any profits and gains derived from business, a deduction of an amount equal to 30% of additional employee cost incurred in the course of such business in the previous year, would be allowed for three assessment years including the assessment year relevant to the previous year in which such employment is provided.

(ii) Eligibility Criteria

The deduction would be allowed only subject to fullfilment of the following conditions:

VII. Restrictions on Cash Transactions of Rs. 2 Lacs or More

Provisions of Section 269ST

Section 269 T was inserted in the Income Tax Act, 1961 by the Finance Act, 2017. The government has aimed to curb generation of black money, to move towards less cash economy and promote digital economy. The government has attempted to target and penalize receiver instead of payer. It is applicable whether the recipient person is a seller of goods or provider of service transferor of capital assets or any other person. Further, section begins with words ‘no person’ which means this section is applicable to all whether individual, company, firm, trust or association of persons. This section is applicable to residents and non residents. We shall divide the section into 5 parts to understand it in a better way:

A. No person shall receive an amount of two lakh rupees or more in aggregate from a person in a day

The first clause of the section has restricted any person, to not receive an amount of Rs. 2 Lakh or more from a person in a day otherwise than by an account payee cheque or an account payee bank draft or use of electronic clearing system through a bank account. Here purpose of the payment is irrelevant. The main focus is ‘from a person’ and ‘in a day’.

Now a question arises what is a meaning of a day. A legal day commences at 12 o’ clock midnight and continues until the same hour the following night. {Prabhu Dayal Sesma vs State of Rajasthan, AIR 1986 SC 1948)

The restriction is applicable even if the different receipts are in relation to distinct transactions entered into on same day or different days. This section will be violated if following four pre-requisites are fulfilled:

i) There is single payer

ii) There is a single receiver.

iii) The payment is in single day.

iv) The amount received by the person in cash is Rs. 2 Lakhs or above.

The payment may be towards two separate invoices of different dates and each invoice below Rs. 2 Lakh, but the person cannot receive Rs. 2,00,000 or more in cash from a person in aggregate in a single day.

B. In respect of a single transaction

This part of the section restricts receipt of Rs. 2,00,000 or more in respect of a single transaction otherwise than by an account payee cheque or an account payee bank draft or use of electronic clearing system through a bank account. Here the major focus is on ‘single transaction’. The number of installments or parts in which payment is made is irrelevant. Further, here word ‘a person’ is not used. Therefore, the recipient cannot receive Rs.2,00,000 or more in cash in a single transaction even if different persons are making payment. However, if the each of invoice amounts are below Rs. 2 Lakh, this provision may not be contravened. The pre-requisites for section to be violated are:

i) Single Receiver

ii) The cash payment relating to a particular transaction is Rs. 2,00,000 or more.

If the parties try to split their payments, such that one transaction is given effect to over multiple days like making payments of Rs. 10,000 on different dates in respect of a single transaction, then obviously it will not fall under first clause as aggregate is out of question being payments received on different dates but is covered by second clause.

Example

M/s Lotus Chemicals issued invoice of Rs. 7,50,000 to their customer on 19/12/2019. The customer intends to make payment in cash in 10 weekly installments of Rs. 75,000 each. Whether M/s Lotus Chemicals can accept the above proposal?

M/s Lotus Chemicals cannot accept the above proposal as the cash receipts (though on different dates) are towards a single transaction and exceeds Rs. 2 Lakh.

C. In respect of transactions relating to one event or occasion from a person

This clause attempts to target transactions scattered over different days but relating to a single event or occasion. Here major focus is ‘one event or occasion’ and ‘a person’. Pre-requisites for attraction of this section shall be:

i) Single Receiver

ii) Single Payer

iii) Cash payment relating to single event/ occasion is Rs. 2 Lakhs or more.

From the above it is interesting to note that in clause (c) of Section 269ST of Income Tax Act the words “from a person” have been used. Due to this now the language has became that “No person shall receive an amount of Two lakh rupees or more in respect of transactions relating to one event or occasion from a person”. In cases where there are more than one transaction and they are related with one event or occasion, the entity will fell in clause (c) and in such a situation, separate limit will became available for different persons in a joint transaction.

For example, if for a marriage there are 3 different bills of Rs. 1 lakhs each (total Rs. 3 lakhs), and all the three bills are in the name of three different persons say one bill (garden on rent for marriage reception,) of Rs. 1 lakhs is in the name of the person who is being married, second bill (given tent house services) is in the name of father of that person for Rs. 1 lakhs and the third bill (for decoration ) is in the name of the mother of that person for Rs. 1 lakhs. Then in such a situation entire Rs. 3 lakhs can be paid in cash etc. mode i.e., Rs. 1 lakh by the person being married, Rs. 1 lakhs by the father and Rs. 1 lakhs by the mother. Even if all the bills are in the joint names of three persons then also the payment can be made in the above manner.

D. Exemptions: The above provisions are not applicable in the following cases

Receipt by Government;

Receipt by any banking company, post office savings bank or co-operative bank

Transactions of the nature referred to in section 269SS i.e. acceptance of loans/ deposits/ specified advance.

Persons/ receipts notified by government:

Receipts (cash withdrawals) by any person from bank, cooperative bank or post office savings bank

- Receipt by business correspondent on behalf of banking company or cooperative bank as per RBI guidelines.

- Receipt by white label ATM operator from retail outlet sources on behalf of banking company or cooperative bank.

- Receipt from an agent by an issuer of prepaid payment instruments.

- Receipt by company/ institution issuing credit cards against bills raised in respect of one or more credit cards.

- Receipt exempt u/s 10(17A) i.e. any award from state/central government

E. Penalty u/s 271DA:

Penalty for failure to comply with provisions of section 269ST

(1) If a person receives any sum in contravention of the provisions of section 269ST, he shall be liable to pay, by way of penalty, a sum equal to the amount of such receipt: Provided that no penalty shall be imposable if such person proves that there were good and sufficient reasons for the contravention. (2) Any penalty imposable under sub-section (1) shall be imposed by the Joint Commissioner.

If any person violates sec 269ST, then penalty shall be levied @ 100% of such receipt.

Example 1: ABC & Co. issued invoice of Rs. 1,60,000 to Mr. Bhushan on 15/04/2020 and another invoice of Rs. 1,25,000 on 16/04/2020. Can ABC & Co receive the payment of Rs.2,85,000 in cash/ bearer cheque on 17/04/2020?

No, as the aggregate of both the invoices exceeds Rs. 2,00,000; ABC & Co. cannot receive the whole amount in cash/ bearer cheque. Only amount upto Rs. 1,99,999 can be received in cash/ bearer cheque in single day.

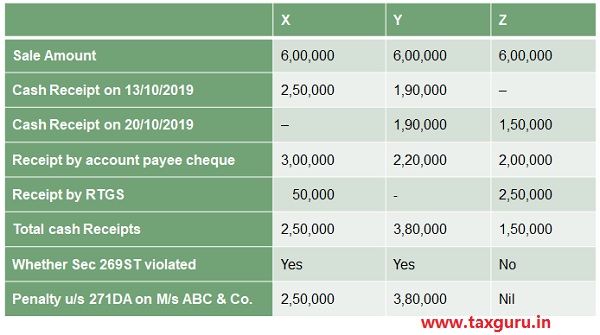

Example 2 : ABC & Co. issued following invoices and received following payments:

Example 3: M/s ABC & Co. sold a machinery for Rs. 6,00,000 to 3 different persons X, Y and Z

Example 4. Mr. Puneet receives following gifts on his marriage:

| S.No. | Particulars | Whether Sec 269ST Violated |

Reasons |

| 1 | Receives shagun of Rs.1,000 each in cash from 220 persons | No | None of the person gifted Rs.2 Lakh or more in cash. |

| 2 | Receives shagun of Rs.1,11,000 from his uncle on the marriage day and Rs.1,51,000 on the day of reception. | Yes | As the total cash receipt from a personrelating to occasion ‘marriage’ exceeds Rs. 2 Lakh |

| 3 | His uncle gifted Rs. 1,70,000 to him and Rs. 81,000 to his mother in cash | No | No person has received Rs.2 Lakh or more in cash. |

In case of 2nd and 3rd limb of sec 269ST the word ’transaction’ has been used

(b) in respect of a single transaction; or

(c) in respect of transactions relating to one event or occasion from a person

However, for the purposes of section 2(xxiv) of the Gift-tax Act, 1958, it has been held that the term ‘transaction’ refers to a bilateral transaction but not to a unilateral transaction. [Dr. A. R. Shukla v. CGT [1969] 74 ITR 167 (Guj.); CGT v. Jer Mavis Lubimoff [1978] 114 ITR 90 (Bom.), CGT v. Ebrahim Haji Usuf Botawala [1980] 122 ITR 62 (Bom.)]. Hence, a gift may not be covered under 2nd and 3rd limb of sec 269ST of the Act.

Following the above judgments, gift is a unilateral act and not a transaction. Therefore, in the above table, in case 2, where shagun of Rs.1,11,000 is received from his uncle on the marriage day and Rs.1,51,000 on the day of reception, there may not be violation of sec 269ST. However, the first limb i.e. in aggregate from a person in a day shall continue to apply in case of gifts.

Example 5. M/s Tania Event Managers arranged a marriage function in February 2020.

| Date | Particulars | Case 1 | Case-2 | Case-3 | Case-4 |

| 22/02/2020 | Invoice for ‘Ring Ceremony’ | 1,80,000 | 70,000 | 1,80,000 | 1,80,000 |

| 23/02/2020 | Invoice for catering on ‘Marriage Day’ | 1,90,000 | 60,000 | 1,90,000 | 1,90,000 |

| 23/02/2020 | Invoice for decoration on ‘Marriage Day’ | 45,000 | 45,000 | 45,000 | 45,000 |

| Total of Invoices | 4,15,000 | 1,75,000 | 4,15,000 | 4,15,000 | |

| 01/03/2020 | Received cash from Bride’s father | 1,75,000 | 1,75,000 | 1,75,000 | 1,75,000 |

| 03/03/2020 | Received cash from Bride’s father | 60,000 | – | – | 25,000 |

| 04/03/2020 | Received cash from Bride’s brother | – | – | 65,000 | – |

| 05/03/2020 | Received payment by credit card/ account payee cheque | 1,80,000 | – | 1,75,000 | 2,15,000 |

| Total cash payments | 2,35,000 | 1,75,000 | 2,40,000 | 2,00,000 | |

| From Bride’s father | 2,35,000 | 1,75,000 | 1,75,000 | 2,00,000 | |

| From Bride’s brother | – | – | 65,000 | – | |

| Violation of sec 269ST | Yes | No | No | Yes | |

| Penalty u/s 271DA | 2,35,000 | Nil | Nil | 2,00,000 |

Summary of Sec 269ST

| CLAUSES | Conditions | Irrespective of |

| a) in aggregate from a person in a day | Number of persons- 1

Number of Days-1 |

Number of transactions |

| a)in respect of a single transaction | Number of transactions- 1 | Number of persons

Number of days |

| a)in respect of transactions relating to one event or occasion from a person | Number of persons-1

Number of event/occasion- 1 |

Number of days

Number of transactions

|

VIII. Disallowance u/s 40A(3) vs Restrictions on cash u/s 269ST

Example: Five separate invoices of Rs. 60,000 each were issued to a customer. The customer intends to make cash payment in installments of Rs. 10,000 each on daily basis. State the applicability of Sec 269ST and 40A(3)?

As per sec 40A(3), if any payment is made by an assessee to a person in a day above Rs.10,000, other than by account payee cheque/ draft or ECS through bank account, then expenditure shall be disallowed i.e the expenditure shall not be allowed as deduction. For this reason, generally cash payments by debtors to any person are made up to Rs.10,000 only per day. But this restriction applies only to a person who is making payment for business purposes (or for any expenditure by a charitable/ religious trust). If any expenditure is incurred by assessee for personal purpose, then he can make payment above Rs. 10,000 in cash in a day. Further, this does not bind the recipient i.e. shopkeeper to accept only up to Rs. 10,000 per day from any customer. He can accept up to Rs. 1,99,999 in a day from any customer as per the provisions of sec 269ST of the Act.

As per sec 269ST, Rs 2 Lakh or more cannot be respected by any mode other than account payee cheque/ draft/ ECS in respect of a single transaction. In this case the recipient can accept up to Rs. 1,99,999 per day from the customer as each invoice is less than Rs. 2 Lakh. However, the customer has to examine the applicability and impact of sec 40A (3)

The provisions of second circumstance of sec 269ST of the Act envisage that no single transaction should exceed the specified limit. Although each of such receipts on daily basis are within the prohibited limit and not covered by the first circumstance, such receipts would fall under the prohibited category as they pertain to a single transaction.

| Invoice Date | Invoice Amount | Maximum Daily Cash Payment by Buyer

Sec 40A(3) |