Dear Professional Colleague,

Sub: ITR 7 Guidance Note issued by CPC Bengaluru

The Centralized Processing Center, Bengaluru has conducted an exclusive Webinar on ITR-7 for A.Y 2020-21 on 17.12.2020 from 04.00 PM to 05.30 PM for the benefit of Chartered Accountants, Tax Practitioners & Taxpayers.

The following topics were covered during the webinar:

- Guidance for filing ITR-7 for A.Y 2020-21.

- Common mistakes noticed in ITR-7 in the

- past and how to prevent them for A.Y. 2020-21

- How to rectify the errors of earlier assessment years

- Frequently asked questions relating to processing of ITR-7 at CPC

The Centralised Processing Center, Bengaluru has prepared “ITR 7 Guidance Note” based on the queries received during the said webinar. The said Guidance Note is prepared for the benefit of Chartered Accountants, Tax Practitioners & Tax Payers.

CENTRALIZED PROCESING CENTRAL

INCOME TAX DEPARTMENT

ITR-7 GUIDANCE NOTE

DISCLAIMER

The answers to the frequently asked questions given in this Guidance Note are based on an analysis of the queries submitted to us on various occasions citing specific cases and hence the answers may kindly be treated as indicative, as the responses could be varied based on specific facts. The contents of this Guidance Note are for information and broad guidance and do not have any independent legal sanctity. Any use of the contents of this Guidance Note may be carried out having due regard to the provisions of extant and relevant Acts, Rules, judicial Pronouncements, and Administrative/ Technical instructions / Circulars/ Advisories/ Notifications of competent authorities wherever applicable. Though every effort has been made to provide accurate and updated information, it is likely that some details may require to be updated or corrected on a continual basis. This is a publication for general usage of taxpayers and taxpayers’ representatives at large for reference purpose and hence the publisher is not responsible in any manner for any damages caused due to references made herein and the Department is not responsible. You are required to adhere to the Acts, Rules, Circulars and notifications issued from time to time.

No part of this Guidance Note can be used as reference in any court of law or other statutory purposes as the Guidance Note is an indicative reference material only for high level introduction to services provided by the Centralized Processing Center, Bengaluru. No part of the content may be re-used for any publication without prior permission of the Director of Income Tax (CPC), Bengaluru, in writing. Suggestions to improve the Guidance Note are welcome and it is requested that errors, if any, may kindly be brought to notice.

Guidance for Filing ITR-7 for AY 2020-21

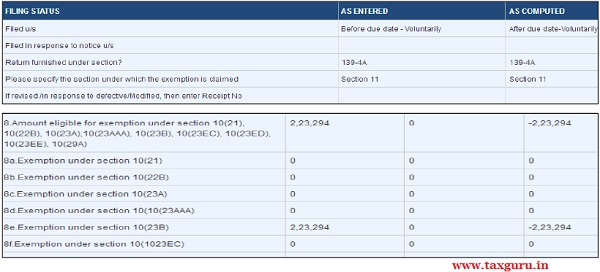

Section 11

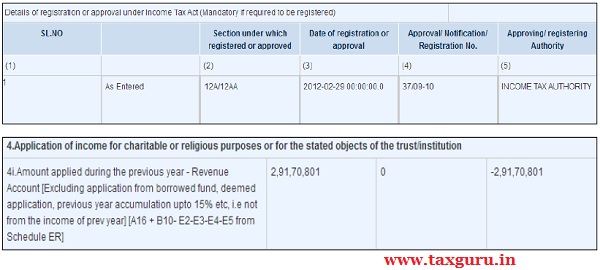

- Registration Details u/s 12A/12AA should be filled in Schedule Part-A General

- ‘Return furnished section’ should be selected as 139(4A) and ‘Section under which exemption claimed’ should be select as section 11 in Schedule Part-A General.

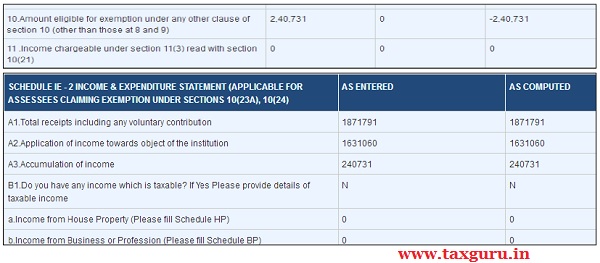

- Income should be disclosed in Schedule-AI and/or Schedule-VC

- Application of Income- Revenue expenditure should be disclosed in Schedule-ER

- Application of Income- Capital expenditure should be disclosed in Schedule-EC.

- Exemption u/s 11(1A) claimed in Schedule EC will be allowed to the extent of net consideration disclosed in the Schedule-AI.

- If the total income of the trust or institution without giving effect to the provisions of section 11 and section 12 exceeds the maximum amount which is not chargeable to income-tax, audit report in Form 10B has to be filled one month prior to the due date specified u/s 139(1) as per Section 44AB.

- If exemption under explanation 11(1)-Deemed Application is claimed – Form 9A should be filed within the due date specified u/s 139(1).

- If exemption under section 11(2)– for Accumulation is claimed – Form 10 and Return of Income should be filed within the Due Date specified u/s 139(1).

- If there is any change in the Objects/activities during the year, assessee has to make an application for fresh registration within 30 days as per section 12A(1)(ab). This information needs to be provided in Schedule Part A General(2)

- If purpose of the trust is advancement of any other object of General Public utility, then the total receipts and Percentage of this activity should be mentioned in Schedule Part A General (2).

- However if the percentage of receipts of such activities exceed 20% of total receipts of the trust/Institution then exemption u/s 11 is not allowable (As per section 13(8)).

Exemption u/s 10(23C)(iv/v/vi/via)

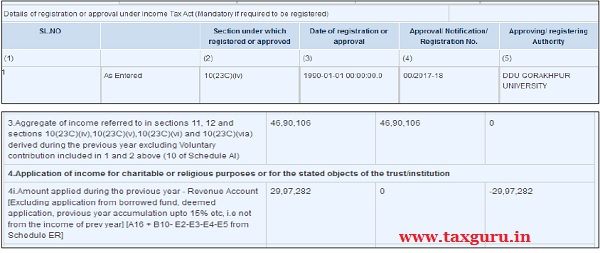

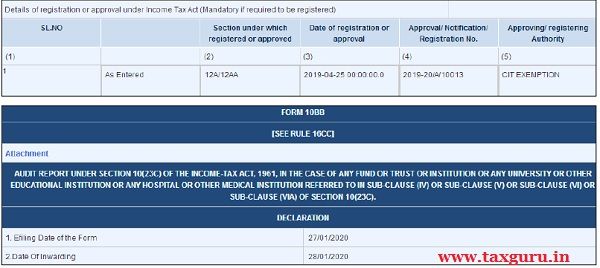

- Approval Details u/s 10(23C)(iv/v/vi/via) should be filled in Schedule Part A General.

- ‘Return furnished section’ should be selected as 139(4C) and ‘Section under which exemption claimed’ should be selected as section 10(23C)(iv/v/vi/via) in Schedule Part A General.

- Income should be disclosed in Schedule AI and/or Schedule VC.

- Application of Income- Revenue expenditure should be disclosed in Schedule ER

- Application of Income- Capital expenditure should be disclosed in Schedule EC.

- If the total income of the trust or institution without giving effect to the provisions of section 10(23C)(iv/v/vi/via) exceeds the maximum amount which is not chargeable to income-tax, audit report in Form 10BB to be filled one month prior to the due date specified u/s 139(1) as per Section 44AB.

- If exemption claimed under section 11(2), amount of Accumulation should be filled in Schedule-I.

- If assessee is approved u/s 10(23C)(iv or v) and purpose of the trust is advancement of any other object of General Public utility, then the total receipts and Percentage of such activities should be mentioned in Schedule Part-A General(2). However if the percentage of receipts of such activities exceed 20% of total receipts of the trust/Institution then exemption u/s 10(23C)(iv or v) is not allowable.

Exemption u/s 10(21)

- For Research Association – Approved u/s 35

- Registration Details u/s 35 should be filled in Schedule Part-A General.

- ‘Return furnished section’ should be selected as 139(4C)/(4D) and ‘Section under which exemption claimed’ should be selected as section 10(21)/ 10(21) read with section 35 in Schedule Part-A General.

- Receipts should be disclosed in Schedule-IE1 and/or Schedule-VC

- Exemption amount should be entered in No.8(a) of Schedule Part BTI.

Exemption u/s 10(23AAA)

- For Fund established for welfare of employees

- Registration Details u/s 10(23AAA) should be filled in Schedule Part-A General.

- ‘Return furnished section’ should be selected as 139(4C) and Section under which exemption claimed should be selected as section 10(23AAA) in Schedule Part-A General.

- Receipts should be disclosed in Schedule-IE1 and/or Schedule-VC.

- Exemption amount should be entered in no. 8(d) of Schedule Part-BTI.

Exemption u/s 10(23A)

- For Profession of Law, Medicine, Engineering, etc. as Specified by Central Govt.

- ‘Return furnished section’ should be selected as 139(4C) in Schedule Part-A General.

- ‘Section under which exemption claimed’ should be selected as section 10(23A) in Schedule Part-A General.

- Receipts should be disclosed in Schedule-IE2 and/or Schedule-VC.

- Exemption is not allowable on HP income, interest and dividend income.

- Exemption amount should be entered in No. 8(c) of Schedule Part-BTI.

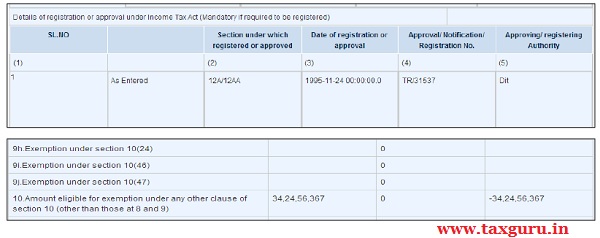

Exemption u/s 10(24)

- For Trade Unions

- ‘Return furnished section’ should be selected as 139(4C) in Schedule Part-A General.

- ‘Section under which exemption claimed’ should be selected as section 10(24) in Schedule Part-A General.

- Receipts should be disclosed in Schedule-IE2 and/or Schedule-VC.

- Exemption is not allowable on BP income and CG income.

- Exemption amount should be entered in SI.No.9(h) of Schedule BTI.

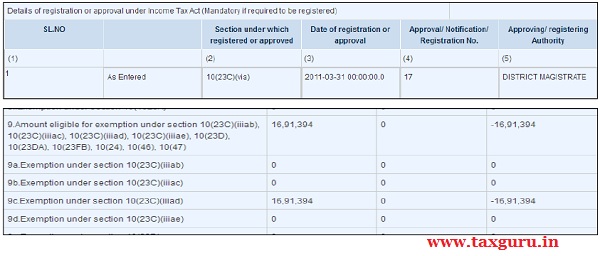

Exemption u/s 10(23C)(iiiab)/(iiiac)

- ‘Return furnished section’ should be selected as 139(4C) in Schedule Part-A General.

- ‘Section under which exemption claimed’ should be selected as section 10(23C)(iiiab)/(iiiac) in Schedule Part-A General.

- Objective of the institution should be mentioned as Education for 10(23C)(iiiab) and as Medical for 10(23C)(iiiac).

- Receipts should be disclosed in Schedule-IE3 and/or Schedule-VC.

- Grants received from Government should be disclosed in Schedule-VC / Schedule-IE3.

- As per Rule 2BBB, exemption is allowed only if Government grants of such university or other educational institution, hospital exceed 50% of the total receipts including any voluntary contributions.

- Exemption amount should be entered in SI.No.9 of Schedule Part-BTI.

Exemption u/s 10(23C)(iiiad)/(iiiae)

- ‘Return furnished section’ should be selected as 139(4C) in Schedule Part-A General.

- ‘Section under which exemption claimed’ should be selected as section 10(23C)(iiiad)/(iiiae) in Schedule Part-A General.

- Objective of the institution should be mentioned as Education for 10(23C)(iiiad) and as Medical for 10(23C)(iiiae).

- Receipts should be disclosed in Schedule-IE4 and/or Schedule-VC.

- As per Rule 2BC, exemption is allowable only if the annual receipts of such university or other educational institution, hospital does not exceed Rs.1 Crore.

- Exemption amount should be entered in the Part-BTI Sl.No.9.

Exemption u/s 10(22B), 10(23B), 10(23D), 10(23DA), 10(23EC), 10(23ED), 10(23EE), 10(29A), 10(46), 10(47)

- ‘Return furnished section’ should be selected as 139(4C) in Schedule Part-A General.

- ‘Section under which exemption claimed’ should be selected as 10(22B), 10(23B), 10(23D), 10(23DA), 10(23EC), 10(23ED), 10(23EE), 10(29A), 10(46), 10(47) in Schedule Part-A General.

- Receipts should be disclosed in Schedule-IE1 and/or Schedule-VC.

- Exemption amount should be entered in Sl. Nos.8 or 9, as applicable, of Schedule Part-BTI.

Exemption under other clauses of section 10

- ‘Return furnished section’ should be selected as Others in Schedule Part-A General.

- ‘Section under which exemption claimed’ should be selected as section 10(20), 10(23AA), 10(23AAB), 10(23BB), 10(23BBA), 10(23BBC), 10(23BBE), 10(23BBG), 10(23BBH), 10(23C)(i), 10(23C)(ii), 10(23C)(iii), 10(23C)(iiia), 10(23C)(iiiaa), 10(23C)(iiiaaa), 10(23C)(iiiaaaa) 10(25)(i), 10(25)(ii), 10(25)(iii), 10(25)(iv), 10(25)(v), 10(25A), 10(26AAB), 10(26B), 10(26BB), 10(26BBB), 10(44) in Schedule Part-A General.

- Receipts should be disclosed in Schedule-IE1 and/or Schedule-VC.

- Exemption amount should be entered in the respective field of Schedule Part BTI (Part BTI Sl.No. (10))

- Refer Boards Circular 18/2017 for TDS credit where income is unconditionally exempt u/s 10 (Eg. Approved Provident Fund, Approved Gratuity fund.

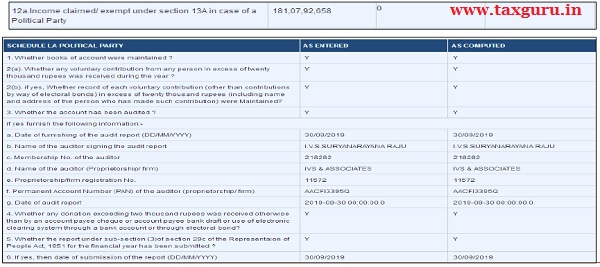

Exemption u/s 13A

For Political Parties

- ‘Return furnished section’ should be selected as 139(4B) in Schedule Part-A General.

- ‘Section under which exemption claimed’ should be selected as section 13A in Schedule Part-A General.

- Income should be mentioned under all heads of income and Schedule-VC

- Exemption is not allowable on BP income.

- Return of income should be filled within the due date specified u/s 139(1).

- Schedule-LA should be filled and all conditions mentioned in section 13A should be fulfilled.

- Exemption amount should be entered in Sl.No.12a of Schedule Part BTI.

Exemption u/s 13B

- For Electrol Trusts

- Registration Details u/s 13B should be filled in Schedule Part-A General.

- ‘Return furnished section’ should be selected as 139(4B) and ‘Section under which exemption claimed’ should be selected as section 13B in Schedule Part-A General.

- Exemption is allowable on Voluntary Contribution.

- Schedule-ET should be filled and all conditions mentioned in section 13B read with Rule 17CA should be fulfilled.

- Exemption amount should be entered in Sl.No.12b of Schedule Part-BTI.

Section wise – Applicable Schedules ITR 7 AY 2020-21

Section 11 or 10(23C)(iv to via)

- Income should be disclosed in Schedule-AI and/or Schedule-VC

- Application of Income- Revenue expenditure should be disclosed in Schedule-ER

- Application of Income- Capital expenditure should be disclosed in Schedule-EC

Exemption u/s 10(23A)

- Receipts should be disclosed in Schedule-IE2 and/or Schedule-VC.

- Exemption is not allowable on HP income, interest and dividend income.

- Exemption amount should be entered in Sl.No.8(c) of Schedule Part-BTI.

Exemption u/s 10(23C)(iiiab)/(iiiac)

- Objective of the institution should be mentioned as Education for 10(23C)(iiiab) and as Medical for 10(23C)(iiiac) in Schedule-IE3.

- Gross receipts including Government grants should be disclosed in Schedule-IE3 and/or Schedule-VC.

- Exemption amount should be entered in Sl.No.9 of Schedule Part BTI.

- Objective of the institution should be mentioned as Education for 10(23C)(iiiad) and as Medical for 10(23C)(iiiae) in Schedule-IE4.

- Receipts should be disclosed in Schedule IE4 and/or Schedule-VC.

- Exemption amount should be entered in Sl.No.9 of Schedule Part-BTI.

Exemption u/s 10(22B), 10(23B), 10(23D), 10(23DA), 10(23EC), 10(23ED), 10(23EE), 10(29A), 10(46), 10(47) and Other clauses of Sec 10

- Receipts should be disclosed in Schedule-IE1 and/or Schedule-VC.

- Exemption amount should be entered in Sl.No.8 of Schedule Part-BTI

Exemption u/s 13A

- Income should be mentioned under all heads of income and Schedule-VC.

- Exemption is not allowable on BP income.

- Schedule-LA should be filled and all conditions mentioned in section 13A should be fulfilled.

- Exemption amount should be entered in Sl.No.12a of Schedule Part-BTI.

Exemption u/s 13B

- Total Contribution should be disclosed in Schedule-VC.

- Exemption is allowable on Voluntary Contribution.

- Schedule-ET should be filled and all conditions mentioned in section 13B read with Rule 17CA should be fulfilled.

- Exemption amount should be entered in Sl.No.12b of Schedule Part-BTI.

COMMON MISTAKES MADE IN FILING ITR-7

Common Mistakes

- Assessees are claiming exemption without entering the registration / approval details in Schedule “Part-A General”.

- As per section 11(7), assessee is not eligible to claim exemption u/s 10 (other than 10(1) or 10(23C)) if the trust or institution is registered under Section 12A/12AA but claims it.

As per 20th proviso to section 10(23C), assessee is not eligible to claim exemption u/s 10 other than 10(1) if the trust or institution is approved u/s 10(23C)(iv/v/vi/via).

Assessee does not select the applicable clause of section in Schedule “Part-A General” and the amount of exemption entered in the corresponding field of Schedule “Part-BTI”

Receipts are disclosed in Schedules which is not applicable to assessee leading to disallowance of exemption claimed. Fill in only the appropriate schedule.

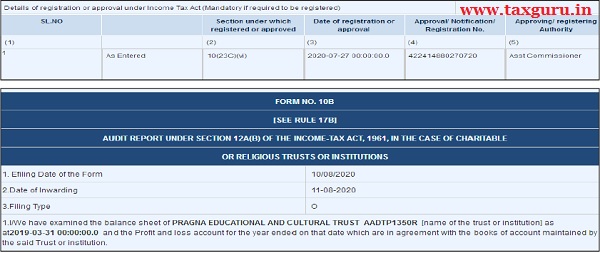

Assessee registered u/s 12A/12AA not e-filed the Audit Report in Form 10B – to be filed before filing ROI.

Assessee approved u/s 10(23C) (iv/v/vi/via) does not e-file Form 10BB – to be filed before filing ROI.

Form 10 & ROI are not e-filed within the due date u/s 139(1) – exemption claimed is not allowed.

Form 9A is not e-filed within the due date u/s 139(1) – Exemption claimed is not allowed.

Assessee claiming exemption u/s 13A and has not satisfied the condition mentioned u/s 13A and Return is not filed within the due date – exemption is not allowed.

Assessee claiming exemption u/s 13A but Return is not filed within the due date.

- Assessee is approved u/s 10(23C)(iv

- to via) but Audit Report is filed in Form 10B instead of Form 10BB.

- Assessee is registered u/s 12A/12AA but Audit Report is filed in Form 10BB instead of Form 10B.

- Assessee claiming exemption u/s 13B and has not satisfied the condition mentioned u/s 13B read with Rule 17CA.

- Assessee disclosed accreted income in Schedule 115TD but has not computed tax thereon. CPC computes tax on the accreted income and raises demand.

- Income due to non compliance to provisions of the Act has to be entered in Sr.No.5 – Additions – (sec.11(1B), 11(3),12(2) etc.) of Schedule Part – BTI and exemption is not allowable on the amount entered in this column.

- Date of registration : Should be prior to the AY & not during the AY.

Rectification Rights for AY 2018-19 and prior years have been transferred to the jurisdictional AOs.

Assessees can file their request for rectification before the Jurisdictional AOs.

With Regard to AY 2019-20 : details will be shared in the next presentation.