The Hon’ble Finance Minister, Ms. Nirmala Sitharaman, presented the Union Budget on 1 February 2020, introducing measures aimed at, inter-alia, reducing litigation, improving effectiveness of tax administration, providing tax certainty and simplifying compliance with the overall objective of enhancing the ease of doing business in India.

This article focuses on key proposals relating to Indian Transfer Pricing (TP) provisions, which are discussed below:

I. Profit attribution to business connection/ Permanent Establishment (PE) now covered under Safe Harbour Rules (SHR) and Advance Pricing Agreement (APA)

Determination of a PE and profit attribution thereto are among the most complex international tax issues being faced globally, with the same getting exacerbated due to digitalisation of the economy.

In India, different approaches/ methodologies for attribution of profits to PE have been endorsed/ adopted by judicial authorities [such as ad-hoc attribution, formulary apportionment, Functions, Assets & Risks (FAR) based approach, etc.], which has caused uncertainty and confusion in the minds of both taxpayers and the tax administration. To address this complex issue, the Central Board of Direct Taxes (CBDT) had formed a committee to recommend changes to Rule 10 of the Income-tax Rules, 1962 for attribution of profits to PE. The paper released by CBDT for public comments on 18 April 2019[1] recommended use of a fractional apportionment method, to apportion profits derived from sales made in India, using a weighted formula, with weightages given to sales, employees and assets.

On the international front, the OECD[2]/ Inclusive Framework on BEPS[3] has recently endorsed[4] the “Unified Approach” as the basis for negotiations of a consensus-based solution on new profit allocation and nexus rules to be agreed in 2020.

Further, SHR and APA provisions were introduced by the Indian government to reduce litigation and bring in tax certainty. SHR provides tax certainty for relatively smaller cases for future years on general terms, while APA provides tax certainty on case-to-case basis not only for future years but also for the rollback years.

Against this backdrop, the Budget proposes to cover determination of profit attributable [under section 9(1)(i) of the Act] to a PE within the scope of SHR and APA.

- The provisions will apply to an APA entered into on, or, after 1 April 2020. Further, the rollback benefit can also be availed.

- SHR will be applicable for Assessment Year (AY) 2020–21, and subsequent assessment years.

Here, it may be noted that the APA Guidance with FAQs issued by the Indian tax administration had earlier already clarified that, if an applicant admits having a PE, he can file the APA request for profit attribution to PE.

Considering the prevailing global uncertainty on this issue, it is important that detailed rules/ methodologies to be prescribed/ adopted by the tax administration under domestic law, take into account outcome of the OECD led project on tax challenges arising from digitalisation of the economy as well as Government of India’s obligations under international tax treaties.

II. Relaxation of interest limitation rules

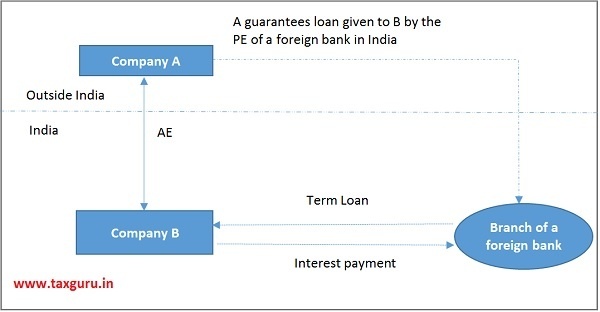

Under section 94B of the Act, the deductible interest or similar expense exceeding INR 1 crore of an Indian company or a PE of a foreign company, in respect of any debt issued by a non-resident, being an associated enterprise (AE), shall be restricted to 30 percent of its earnings before Interest, taxes, depreciation and amortization (EBITDA) or interest paid or payable to the AE, whichever is less. Further, a loan is deemed from an AE if an AE provides implicit or explicit guarantee in respect of the loan. The aforesaid section is broadly in line with the Action Plan 4 of the OECD BEPS project.

The Budget proposes[5] that interest limitation rules shall not apply to interest paid in respect of a debt issued by a lender which is a PE in India of a non-resident, being a person engaged in the business of banking.

The proposed amendment may be explained by way of below example:

Company A and Company B are part of a Group engaged in the manufacture and sale of industrial products. Company A has provided guarantee to the Indian branch (PE) of a third party foreign bank on the basis of which foreign bank provides loan to Company B. Accordingly, such debt would be deemed to have been issued by an AE under the proviso to section 94B(1) of the Act.

- Under the existing provisions, interest paid by Company B would have been covered under the ambit of interest limitation rules.

- Subsequent to the proposed amendment, the same would be outside the purview of interest limitation rules

III. Expansion in scope of Dispute Resolution Panel (DRP)

The DRP was set up as an alternate mechanism with a view to fast-track dispute resolution with respect to TP matters.

The Budget proposes[6] to expand the scope of DRP to include cases where the Assessing Officer proposes to make any variation prejudicial to the interest of the taxpayer in his order, regardless of whether the same translates into a variation in the income (or loss) returned by such taxpayer.

The Budget further proposes to expand the definition of ‘eligible assessee’ to include a non-resident, not being a company.

IV. Change in due date for filing Form No. 3CEB and maintenance of TP documentation

To enable pre-filled annual income tax returns, the due date for furnishing Form No. 3CEB and maintaining prescribed TP documentation (local file) is proposed to be one month prior to the due date of filing the annual income tax return.

For Financial Year (FY) 2019-20, the due date would be 31 October 2020.

V. New penalty[7] for false entry or omitted entry

The Budget proposes[8] to introduce a new section to provide for a levy of penalty equal to the aggregate amount of false entry or omitted entry on a person under certain circumstances. The false entry is proposed to include use or intention to use invoice in respect of supply or receipt of goods or services issued without actual supply or receipt of such goods or services.

This provision appears to have been introduced to deal with the issue of fake and fraudulent invoices under Goods & Services Tax (GST) regime. However, this could have far-reaching TP implications as well. Based on TP audit experience, in a number of cases, Transfer Pricing Officers (TPOs) have been found to determine arm’s length price of intra-group services availed by an Indian taxpayer from its overseas AE as ‘Nil’ on various grounds, including alleged failure of taxpayer to produce documentary evidence to demonstrate actual receipt of such services. The authors would like to highlight that satisfaction of need-benefit-receipt tests is inherently subjective and there is significant TP litigation on this matter in India.

Given the risk of tax administration expanding the scope of this section to cover TP issues, tax payers should maintain appropriate documentation to evidence the receipt and benefit of intra-group services.

VI. Concluding thoughts

The proposed amendments expanding scope of SHR and APA provisions as well as DRP provisions are welcome.

Further, considering the large number of TP cases stuck in litigation at various appellate levels, taxpayers may evaluate the proposed Vivad Se Vishwas Scheme under which they can pay only the amount of disputed taxes and get a waiver of interest and penalty (provided they pay by 31 March 2020[9]).

The authors also hope that currently unaddressed representations on rationalisation of Master File threshold and information requirements, introduction of inter-quartile range in line with global practice, release of revised safe harbor rules for FY 2019-20 onwards, etc., would be considered favorably by Government of India in the near future.

[1] This has not yet been finalized by CBDT

[2] Organisation for Economic Co-operation & Development

[3] Base Erosion & Profit Shifting

[4] OECD (2020), Statement by the OECD/G20 Inclusive Framework on BEPS on the Two-Pillar Approach to Address the Tax Challenges Arising from the Digitalisation of the Economy – January 2020, OECD/G20 Inclusive Framework on BEPS, OECD, Paris

[5] Will take effect from 1 April 2021

[6] Will take effect from 1 April 2020

[7] Under new section 271AAD of the Act

[8] Will take effect from 1 April 2020

[9] Those who avail this Scheme after 31 March 2020, will have to pay some additional amount. The Scheme will remain open till 30 June 2020.

Authors:

Manisha Gupta (Partner, Deloitte Haskins & Sells LLP) and Amer Qureshi (Director, Deloitte Haskins & Sells LLP), with support by Parineeta Lala (Deputy Manager, Deloitte Haskins & Sells LLP) and Vatsal Ponda (Assistant Manager, Deloitte Haskins & Sells LLP)

The views expressed by the authors are personal