Understand the criteria for individual and HUF income tax return filing, covering total income, assets outside India, and specific situations. Explore tax audit applicability under Section 44AB, including scenarios for businesses, professions, presumptive schemes, and non-residents. Gain clarity on the essential aspects of income tax and tax audit to ensure compliance and avoid penalties.

Income Tax applicability

This article will go over the criteria for Individual’s and HUF’s income tax returns. More often than not, individuals and HUFs are unaware of whether they are liable to file an income tax return or not. Many people say that since tax dues have been deducted as TDS, income tax return filing is not mandatory for them. Individuals and HUFs either opt not to file their returns or get delayed in filing returns as a result of this uncertainty. Through this post, we will try to clear up this doubt.

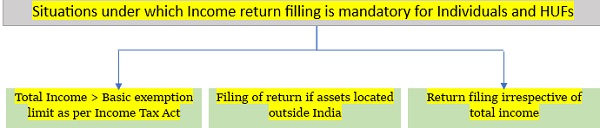

Requirement of filing the income tax return for individuals and HUFs:

Individuals and HUFs must know under what circumstances they are required to file income tax returns. In this article, we will give light on the provisions under which individuals and HIFs are required to file income tax returns.

1. Total Income > Basic exemption limited as per Income tax Act

Individuals and HUFs are required to file an income tax return if their total income exceeds the basic exemption limit as per the Income Tax Act. This means for individuals with ages below 60, total income exceeds 2.5 Lakhs. For individuals older than 60 but less than 80, total income exceeds 3 Lakhs; for those older than 80, total income exceeds 5 lakhs. For this purpose, income under the clubbing provision is also added to the individual’s income. For HUFs basis exemption limit is 2.5 Lakhs only.

The question among individuals and HUFs is what is to be considered for the calculation of total income. In this article, we will clear up this confusion also.

> Deductions are excluded while calculating total income: This means while calculating total income deductions covered under chapter VI-A i.e., sections 80C to 80U of the income tax act are to be excluded. After excluding this deduction from total income, if total income exceeds the applicable basic exemption limit, then income tax return filing is compulsory for individuals or HUF.

For Example: – Mr. A age 55 has an income mentioned in the below table

| Particulars | Amount |

| Net income under the head salary | 3,50,000 |

| Net income under the head house property | 60,000 |

| Gross Total Income | 4,10,000 |

| Less: Deductions under Chapter VI-A: | |

|

1,40,000 |

|

30.000 |

| Net Total Income | 2,40,000 |

As per the above table, Mr. A is not required to file an income tax return. But if we exclude deduction from the above calculated total income then the total income will be Rs. 4,10,000, which is more than the basic exemption list available to Mr. A. So, filing of income return will be mandatory for Mr. A if deductions are excluded from the above example. The same can be seen in the below-mentioned table:

| Particulars | Amount |

| Net Total Income | 2,40,000 |

| Add: Deductions under Chapter VI-A: | |

|

1,40,000 |

|

30.000 |

| Gross Total Income | 4,10,000 |

> Exemptions are excluded while calculating total income: We are required to exclude exemptions available under different sections while calculating the total income of individuals and HUFs. Exemptions available u/s 10(38), 10A, 10B, 10BA, 54, 54B, 54D, 54EC, 54F, 54G, 54GA, and 54GB are a few examples of exemptions to be excluded while calculating total income.

For Example: – Mr. B age 82 has an income mentioned in the below table

| Particulars | Amount |

| Net income under the head salary | 3,50,000 |

| Income under the head capital gain (Sale of the residential house) | 54,00,000 |

| Less: Exemption u/s 54 (Purchase of residential house) | (53,00,000) |

| Gross Total Income | 4,50,000 |

From the above table, it can be said that Mr. B is not required to file an income tax return. But as per the provision of the income tax act, exemptions are to be excluded while calculating total income. So, if exemptions are excluded, the total income of Mr. B will be Rs. 57,50,000 which is more than the exemption limit available to Mr. B. Therefore Mr. B is required to file an income tax return.

2. Filing of return if assets are located outside India

According to provisions of the income tax act, Income tax return filing is mandatory if an individual resident of India is a beneficial owner of any asset or a beneficiary in any asset and meets any of the following criteria at any time during the financial year:

> An individual resident of India holds any asset, including financial interest in any entity located outside India.

> An individual has signing authority in any account which is located outside India.

Income tax return filing is compulsory if an individual or HUF resident of India falls under any of the above situations, whether or not having income chargeable to tax.

3. Return filing irrespective of total Income

According to the provision of the income tax act, Income tax filing is mandatory if any person falls under any of the below situations:

> Any person has deposited more than Rs. 1 Cr in one or current more accounts maintained with a banking company or a cooperative bank

> Any person has incurred expenditure of more than Rs. 2 lakhs for himself or any other person for travel to a foreign country

> Any person has incurred expenditure of more than Rs. 1 lakh towards the consumption of electricity

> Total sales, turnover, and gross receipts, as the case may be, in the business is less than Rs. 60 lakhs during the previous year

> Total gross receipts in the profession do not exceed Rs. 10 lakhs during the previous year

> The aggregate of TDS and TCS during the previous year is Rs. 25,000 or more. However, for senior citizen limit is Rs. 50,000 or more

> Deposit in one or more saving bank accounts an aggregate of Rs. 50 lakhs or more during the previous year

Tax Audit Applicability

The above phrases might have been helpful to clear uncertainty about income tax return filing for individuals and HUFs. To make this article more informative we will also discuss tax audit applicability under various sections of the income tax act.

What is Tax Audit?

Before proceeding with tax audit applicability, we should know what tax audit means under the income tax act. A tax audit is an examination of a taxpayer’s financial statements and records to ensure that they are accurate and comply with the provisions of the income tax act.

Who is covered by Tax audit?

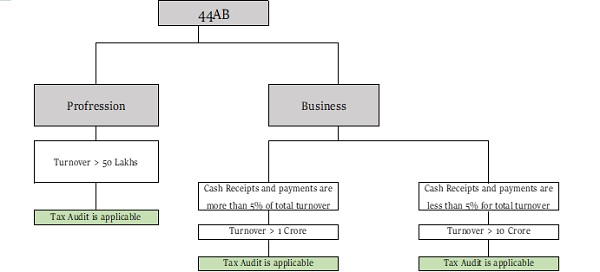

As per Section 44AB, the following persons are required to get their accounts audited:

1. Not opting for a presumptive scheme

As per the above chart, Tax audit is applicable in below mentioned 3 situations:

> In the case of a Profession, if Turnover or total gross receipts are more than Rs. 50 lakhs in a financial year

> In the case of a Business, if cash receipts and payments are more than 5% of total turnover and turnover is more than Rs. 1 Cr in a financial year

> In the case of a Business, if cash receipts and payments are less than 5% of total turnover but turnover is more than Rs. 10 Cr in a financial year

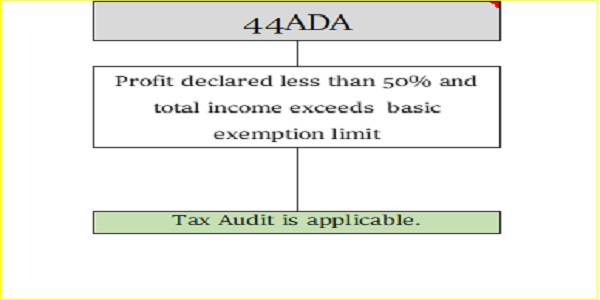

2. Profession opting for presumptive scheme u/s 44ADA

As per the provision of the Income-tax Act, Tax audit is applicable in the case of a profession, if a person opts for a presumptive scheme u/s 44ADA but declares profit less than the limit prescribed i.e.,50% of total turnover/gross receipt and his total income exceeds the income not chargeable to tax.

3. Taxpayer opting for presumptive scheme u/s 44AE

As per the provisions of the income tax act, in the case of presumptive scheme u/s 44AE, taxpayer fall under tax audit provisions in cases:

> Heavy Goods Vehicle: – If a taxpayer owns a heavy goods vehicle i.e., vehicle gross weight/unladen weight is more than 12,000 kgs, and declares income less the rate prescribed under provision i.e., a rate less than Rs. 1,000 per ton of gross vehicle weight per month per vehicle

> Other than Heavy Goods Vehicle: – If the taxpayer does not own a heavy goods vehicle but declares income less than the rate specified under the provision i.e., rate less than Rs. 7,500 per month per vehicle

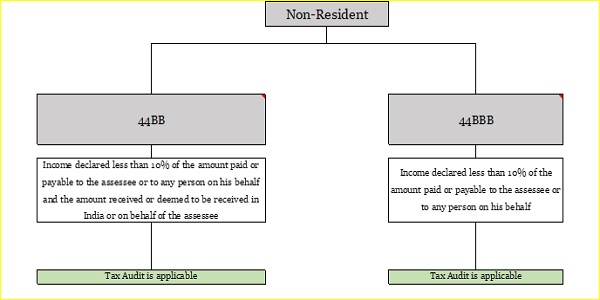

4. Non-resident opting for presumptive scheme

As per the provisions of the income tax act, a tax audit applies to Non-resident or foreign companies in below cases:

> If a non-resident opts for presumptive scheme u/s 44BB and declares income less than the rate prescribed under law i.e., less than 10% of the amount paid or payable to the taxpayer or any person on his behalf and the amount received or deemed to be received in India or on behalf of the taxpayer

> If a foreign company opts for presumptive scheme u/s 44BBB and declares income less than the rate prescribed under law i.e., less than 10% of the amount paid or payable to the taxpayer or any person on his behalf

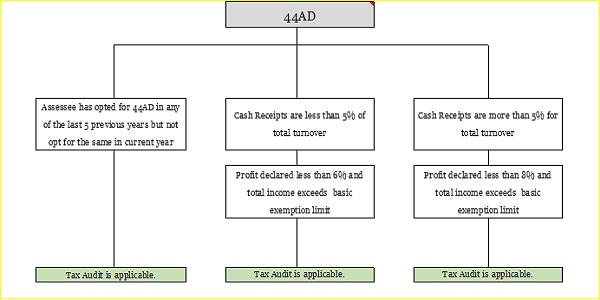

5. Taxpayer opting for presumptive scheme u/s 44AD

As per the income tax act, the presumptive scheme u/s 44AD is said as one of the important provisions. Tax audit is applicable u/s 44AD in the below cases:

> The taxpayer is not eligible to claim presumptive taxation u/s 44AD due to opting out from presumptive taxation in any one financial year from the 5 consecutive years from where the presumptive taxation opted and his income exceeds the maximum amount not chargeable to tax in the subsequent 5 years from the financial year when presumptive scheme opted out

> Tax payer’s total cash receipts are less than 5% of the total turnover and eligible for presumptive scheme u/s 44AD but declare income less than the rate prescribed under law i.e., less than 6% of total turnover

> Tax payer’s total cash receipts are more than 5% of the total turnover and eligible for presumptive scheme u/s 44AD but declare income less than the rate prescribed under law i.e., less than 8% of total turnover

Disclaimer: The author is not responsible for any damages if caused due to a mistake or not following the provisions strictly in the proceedings with any authority or court. This is just academic in nature and purpose. The author has tried to brief and explain the provision. Thanks, with regards.