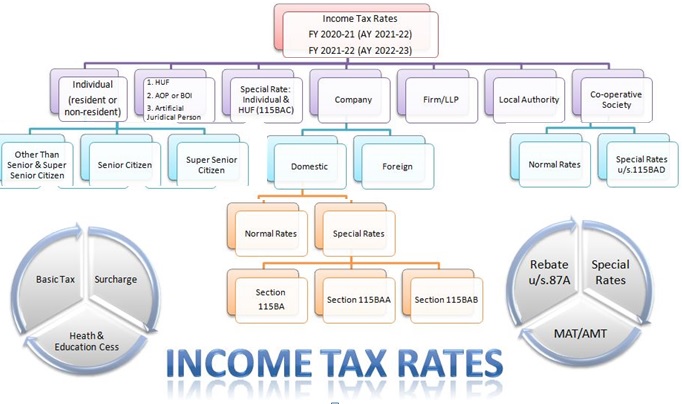

Rates of Income Tax for Financial year (FY) 2020-21 i.e. Assessment Year (AY) 2021-22 and FY 2021-22 (AY 2022-23) applicable to various categories of persons viz. Individuals, Firms, companies etc.

Introduction

This article summarizes Tax Rates, Surcharge, Health & Education Cess, Special rates, and rebate/relief applicable to various categories of Persons viz. Individuals (Resident & Non Resident), HUF, Firms/LLP, Companies, Co-operative Society, Local Authority, AOP, BOI, artificial juridical persons for income liable to tax in the Financial Year 2020-21 (Assessment Year 2021-22) and Financial Year 2021-22 (Assessment Year 2022-23). Since there is no change in Tax Rates in the Finance Bill/Budget 2021, hence Tax Rates applicable to both the assessment year are same.

Page Contents

- 1. Income Tax Rates applicable to Individuals (Resident / Non Resident for FY 2020-21 & 2021-22

- 2. Income Tax Rates for FY 2020-21 & FY 2021-22 for HUF, AOP, BOI, Other Artificial Juridical Person

- 3. Special Income Rates for Individual & HUF u/s. 115BAC for FY 2020-21 & FY 2021-22

- 4. Income Tax Rates applicable to Company for FY 2020-21 & FY 2021-22

- 5. Income Tax Rates for FY 2020-21 & FY 2021-22 for Partnership Firm & LLP

- 6. Income Tax Rates for FY 2020-21 & FY 2021-22 for Local Authority

- 7. Income Tax Rates for FY 2020-21 & FY 2021-22 for Co-operative Society

1. Income Tax Rates applicable to Individuals (Resident / Non Resident for FY 2020-21 & 2021-22

a. Income Tax

| Net Income Range | Rate of Income Tax |

| 1.1 Individuals (Other than senior and super senior citizen) | |

| Up to Rs. 2,50,000 | – |

| Rs. 2,50,000 to Rs. 5,00,000 | 5% |

| Rs. 5,00,000 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

| 1.2 Individuals (Senior Citizen) | |

| Up to Rs. 3,00,000 | – |

| Rs. 3,00,000 to Rs. 5,00,000 | 5% |

| Rs. 5,00,000 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

| 1.3 Individuals (Super Senior Citizen) | |

| Up to Rs. 5,00,000 | – |

| Rs. 5,00,000 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

b. Surcharge:Surcharge is levied on the amount of income-tax at following rates if total income of an assessee exceeds specified limits:-

| Range of Income | Rs. 50 Lakhs to Rs. 1 Crore | Rs. 1 Crore to Rs. 2 Crores | Rs. 2 Crores to Rs. 5 Crores | Rs. 5 crores to Rs. 10 Crores | Exceeding Rs. 10 Crores |

| Surcharge Rate | 10% | 15% | 25% | 37% | 37% |

Note 1: The enhanced surcharge of 25% & 37%, as the case may be, is not levied, from income chargeable to tax under sections 111A, 112A and 115AD. Hence, the maximum rate of surcharge on tax payable on such incomes shall be 15%.

Note 2: Marginal relief is available from surcharge in following manner-

| Net Income Range | Marginal Relief | |

| Exceeds | Do not Exceed | |

| 50 Lakh | 1 Crore | Amount payable as income tax and surcharge shall not exceed the total amount payable as income tax on total income of Rs 50 Lakh by more than the amount of income that exceeds Rs 50 Lakhs |

| 1 Crore | 2 Crore | Amount payable as income tax and surcharge shall not exceed the total amount payable as income-tax on total income of Rs. 1 crore by more than the amount of income that exceeds Rs. 1 crore |

| 2 Crore | 5 Crore | Amount payable as income tax and surcharge shall not exceed the total amount payable as income-tax on total income of Rs. 2 crore by more than the amount of income that exceeds Rs. 2 crore |

| 5 Crore | – | Amount payable as income tax and surcharge shall not exceed the total amount payable as income-tax on total income of Rs. 5 crore by more than the amount of income that exceeds Rs. 5 crore |

c. Health and Education Cess :Health and Education Cess is levied at the rate of 4% on the amount of income-tax plus surcharge.

d. Rebate u/s.87A

A resident individual (whose net income does not exceed Rs. 5,00,000) can avail rebate under section 87A. It is deductible from income-tax before calculating education cess. The amount of rebate is 100 per cent of income-tax or Rs. 12,500, whichever is less.

2. Income Tax Rates for FY 2020-21 & FY 2021-22 for HUF, AOP, BOI, Other Artificial Juridical Person

| Net Income Range | Rate of Income Tax |

| Up to Rs. 2,50,000 | – |

| Rs. 2,50,000 to Rs. 5,00,000 | 5% |

| Rs. 5,00,000 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

Note 1: Surcharge and Health & Education Cess: Same as Rates applicable to Individuals given above

3. Special Income Rates for Individual & HUF u/s. 115BAC for FY 2020-21 & FY 2021-22

The Finance Act, 2020, has provided an option to Individuals and HUF for payment of taxes at the following reduced rates from Assessment Year 2021-22 and onwards:

| Total Income (Rs) | Rate |

| Up to 2,50,000 | Nil |

| From 2,50,001 to 5,00,000 | 5% |

| From 5,00,001 to 7,50,000 | 10% |

| From 7,50,001 to 10,00,000 | 15% |

| From 10,00,001 to 12,50,000 | 20% |

| From 12,50,001 to 15,00,000 | 25% |

| Above 15,00,000 | 30% |

Note 1: Surcharge and Health & Education Cess as well as Rebate u/s.87A: Same as Rates applicable to Individuals given above

Note 2: The option to pay tax at lower rates shall be available only if the total income of assessee is computed without claiming specified exemptions or deductions

4. Income Tax Rates applicable to Company for FY 2020-21 & FY 2021-22

4.1 Domestic Company

Normal Income-tax rates applicable in case of domestic companies are as follows:

| Turnover Criteria | Assessment Year 2021-22 | Assessment Year 2022-23 |

| ♦ Where its total turnover or gross receipt during the previous year 2018-19 does not exceed Rs. 400 crore | 25% | NA |

| ♦ Where its total turnover or gross receipt during the previous year 2019-20 does not exceed Rs. 400 crore | NA | 25% |

| ♦ Any other domestic company | 30% | 30% |

Surcharge : The amount of income-tax shall be increased by a surcharge at the specified rate percentage of such tax:-

| Range of Income | Rs. 1 Crore to Rs.10 Crore | Above Rs. 10 Crore |

| Surcharge Rate | 7% | 12% |

The surcharge shall be subject to marginal relief.

Health and Education Cess : The amount of income-tax and the applicable surcharge, shall be further increased by health and education cess calculated at the rate of 4 percent of such income-tax and surcharge.

Special Tax rates applicable to a domestic company

The special Income-tax rates applicable in case of domestic companies are as follows:

| Domestic Company | Tax Rate |

| ♦ Where it opted for section 115BA | 25% |

| ♦ Where it opted for Section 115BAA | 22% |

| ♦ Where it opted for Section 115BAB | 15% |

Surcharge : The rate of surcharge in case of a company opting for taxability under Section 115BAA or Section 115BAB shall be flat 10% irrespective of amount of total income.

Health and Education Cess: The amount of income-tax and the applicable surcharge, shall be further increased by health and education cess calculated at the rate of 4 percent of such income-tax and surcharge.

MAT : The domestic company who has opted for special taxation regime under Section 115BAA & 115BAB is exempted from provision of MAT. However, no exemption is available in case where section 115BA has been opted.

In that case, the provisions of Minimum Alternate Tax (MAT) applies, tax payable cannot be less than 15% (+HEC) of “Book profit” computed as per section 115JB.

However, MAT is levied at the rate of 9% (plus surcharge and cess as applicable) in case of a company, being a unit of an International Financial Services Centre and deriving its income solely in convertible foreign exchange.

4.2 Foreign Company

| Nature of Income | Tax Rate |

| Royalty received from Government or an Indian concern in pursuance of an agreement made with the Indian concern after March 31, 1961, but before April 1, 1976, or fees for rendering technical services in pursuance of an agreement made after February 29, 1964 but before April 1, 1976 and where such agreement has, in either case, been approved by the Central Government | 50% |

| Any other income | 40% |

Surcharge : The amount of income-tax shall be increased by a surcharge at the specified rate percentage of such tax:-

| Range of Income | Rs. 1 Crore to Rs.10 Crore | Above Rs. 10 Crore |

| Surcharge Rate | 2% | 5% |

However, the surcharge shall be subject to marginal relief.

Health and Education Cess : The amount of income-tax and the applicable surcharge, shall be further increased by health and education cess calculated at the rate of 4 percent of such income-tax and surcharge.

5. Income Tax Rates for FY 2020-21 & FY 2021-22 for Partnership Firm & LLP

Partnership firm (including LLP) is taxable at 30%.

Surcharge : The amount of income-tax shall be increased by a surcharge at the rate of 12% of such tax, where total income exceeds one crore rupees. However, the surcharge shall be subject to marginal relief (where income exceeds one crore rupees, the total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees).

Health and Education Cess: The amount of income-tax and the applicable surcharge, shall be further increased by health and education cess calculated at the rate of 4 percent of such income-tax and surcharge

6. Income Tax Rates for FY 2020-21 & FY 2021-22 for Local Authority

Local authority is taxable at 30%.

Surcharge : The amount of income-tax shall be increased by a surcharge at the rate of 12% of such tax, where total income exceeds one crore rupees. However, the surcharge shall be subject to marginal relief (where income exceeds one crore rupees, the total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees).

Health and Education Cess : The amount of income-tax and the applicable surcharge, shall be further increased by health and education cess calculated at the rate of 4 percent of such income-tax and surcharge.

7. Income Tax Rates for FY 2020-21 & FY 2021-22 for Co-operative Society

7.1 Normal Rates

| Taxable income | Tax Rate |

| Up to Rs. 10,000 | 10% |

| Rs. 10,000 to Rs. 20,000 | 20% |

| Above Rs. 20,000 | 30% |

Surcharge: The amount of income-tax shall be increased by a surcharge at the rate of 12% of such tax, where total income exceeds one crore rupees. However, the surcharge shall be subject to marginal relief (where income exceeds one crore rupees, the total amount payable as income-tax and surcharge shall not exceed total amount payable as income-tax on total income of one crore rupees by more than the amount of income that exceeds one crore rupees).

Health and Education Cess: The amount of income-tax and the applicable surcharge, shall be further increased by health and education cess calculated at the rate of four percent of such income-tax and surcharge.

7.2 Special tax rates applicable to a Co-operative societies

| Taxable income | Tax Rate |

| Any income | 22% |

Note:

1. The Finance Act, 2020 has inserted a new Section 115BADin Income-tax Act to provide an option to the co-operative societies to get taxed at the rate of 22% plus10% surcharge and 4% cess.

2. The resident co-operative societies have an option to opt for taxation under newly Section 115BADof the Act w.e.f. Assessment Year 2021-22. The option once exercised under this section cannot be subsequently withdrawn for the same or any other previous year.

3. If the new regime of Section 115BADis opted by a co-operative society, its income shall be computed without providing for specified exemption, deduction or incentive available under the Act. The option to pay tax at lower rates shall be available only if the total income of co-operative society is computed without claiming specified exemptions or deductions

4. The societies opting for this section have been kept out of the purview of Alternate Minimum Tax (AMT).

5. Further, the provision relating to computation, carry forward and set-off of AMT credit shall not apply to these assessee’s.

******

Income Tax Rates compiled by:

CA Sagar Gambhir | FCA, DISA (ICAI), DIRM (ICAI), B.COM | casagargambhir@gmail.com

Author can be reached at casagargambhir@gmail.com for any queries, issues & recommendations relating to article. Any feedback for improvement would be really appreciated.

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author Bio

I am working in Muscat, Sultanate of Oman. There are no personal taxes in this country.

As part of my final settlement on retirement, I will be entitled to an End Of Service Benefit ( equivalent of Gratuity). Will this be taxable in India, once I return to India post retirement and my status changes from NRI to Resident?

Gratuity and Retirement benefits are exempt to the extent limit specified as per link below–https://www.incometaxindia.gov.in/_layouts/15/dit/mobile/viewer.aspx?path=https://www.incometaxindia.gov.in/charts%20%20tables/list_of_benefits_available_to_a_salaried_person_final.htm&k=&IsDlg=0

Further Residential status depends upon no. of days stay in India. Once you return to India, you will be a Resident. But can continue to enjoy some tax benefits available to NRIs as per criteria prescribed by Tax Law.

With Govt abolishing DDT at source for companies and abolishing of 10 L annual dividend exemption for tax payers – now the dividend is added as income and taxed – this has been disastrous for tax payers- , but benefits the Companies as well as govt – but who cares for tax payers

In my case the income was about 26 lakh before this IT disastrous rule came – and adding 7 lakh as dividends- my total becomes 23 L. Earlier I could take deduction as 3.25 L .

In this situation which of the two tax paying options for I Tax should I take ?? Thanks everyone for advise !

I am a 72 yrs retd Defence man and get gross monthly pension of 108000 and avail 1.50 L permissible deductions>my bank int comes to around 70K.

How much Itax payable for current FY

Pension 12,96,000

Less Std ded and perm ded (-) 2,00,000

bal 10,96,000

Add bank int (70k -10k) + 60,000

Taxable 11,56,000

Tax 20% 0n 10L =2L

Bal 30% on 1.56 L =46,800

Tot 2,46,000

add 45 % edn cess 9,872

Tot Tax payabale 2,55,872

Is my calculation correct?(means out of 12 months,approx 3 months pension goes to I Tax)

What advice to reduce tax besides std ded of 50K and LIC of 1 L and Tax relief long term MFs of 1.50L of G total of 2 L of permissible ded.

If totable taxable income exceeds Rs. 2 crore including Short term capital gains but is below Rs. 2 cr excluding STCG, is the surcharge applicable on the income other than STCG 15% or 25% ?

15%

how to earn rupees so i can pay income tax?

1. I got retired on 31-01-2021.

2. My taxable income is= Rs 5,076,823.00(salary=5,013,190 & Interest from F.D=63,633)

3. My DOB=11-01-1961 Whether I am entitled for tax benefit for Senior Citizen for whole amount or partial amount.

4.what will be my tax calculation, cess and surcharge etc.

Please send me asper new tax sceam

Is old tax regime applicable for fy 2021-22 (ay 2022-23)?

Very useful information given in the article

I am Bank Manager.My total/net income is 15.60 Lac. Please let me inform what is tax payable amount snd surcharge snd cess %age.-Regards

Refer tax calculator -https://www.incometaxindia.gov.in/pages/tools/tax-calculator.aspx

Can you please explain me how rebate will work, if I am under 4.5 – 5 lakhs slab ?

Yes, full tax rebate for taxable income below 5 lacs. (Max Rebate 12500)

Shall i switch over the New scheme to old scheme while filing return of Assesment year 2021-22 please. My DDO has recover the TDS as per new scheme now i found that i am beneficial for old scheme. Please offer comments

Yes , you can do the same

Whether the amount received as Gratuity is included in the total income for calculation of IT, though Gratuity is fully exempted from Tax.

Not included

INCOME Rs. 1000000 (Fy 2020-21).Sr. CIitizen

Nil investment. INCOME TAX? PLEASE

Tax calculator

https://www.incometaxindia.gov.in/pages/tools/tax-calculator.aspx

I am a US citizen. I was a resident Indian till I left India in December, 2019. Now I am in USA and could not return to India due to COVID- 19. I am now planning to return to India in June,2021.

Since the whole of my stay in 2020 was in US, should I pay Income Tax as a NRI for the year from April,1,2020 to March, 31:2021. I have pension income from Railways.

What are my tax rates, my income from pension will be about Rs. 7.5 lakhs. Can I save 1.5 lakhs if I invest in ELSS mutual funds. Please clarify,

Will I get advantage if I am more than 80 years.

Thanks.

Thank you, CA. Sagar Gambhir, for this article. I have a few questions. I am a senior citizen (age 65) and an NRI but, in FY 2020-21 due to Covid-19 I could not travel to my destination countries. So, for AY2021-22 I will be filing my tax return as a resident Indian. My only income in India comes from bank fixed deposit interest. Questions: (i) do I have to formally change my residence status for tax purpose and, if yes, how? (ii) Do I qualify for senior citizen related tax benefits? (iii) what are the tax deductions I can claim? Thank you.

Not just the salaried middle class, but the pensioners, including seniors and super seniors have been totally neglected!

Should an 85 year old pensioner be treated the same way under the new tax scheme, as a 35 year old salaried person? Moreover, should the pensioners also be made to pay the 4% cess ? Haven’t we contributed throughout our active years ? Don’t we deserve any consideration at all at an age when our income has been halved and our expenses have doubled ?

Good

Why does this government treat higher income group of salaried class as milking cows? Just because they don’t have collective bargaining power….it’s the salaried which pays the taxes fully and after that yet we have to pay GST on all the services and products that we buy or avail. Isn’t tax on tax principally wrong

Government knows that we the Salaried Class employee can not do much to dent their vote bank. So they are least bothered.

Thank you very much

informative