Understand Income Tax Assessment for Co-operative Societies, covering definitions, computation of total income, deductions under Section 80P, rates for AY 2022-23, 2023-24, and the new Section 115 BAE introduced in AY 2024-25. Explore proposed benefits and recent tax reforms for cooperative societies.

1. Definition of a Co-operative Society as per the Income-Tax Act.

Section 2(19): ‘co-operative society‘ means a co-operative society registered under the Co-operative Societies Act, 1912 (2 of 1912), or under any other law for the time being in force in any State for the registration of co-operative societies.

2. Computation of Total Income of Co-operative Societies

Following is the procedure to find out tax liability of a co-operative society.

a. Income from House Properties

b. Income from business

c. Income from Capital Gains

d. Income from Other Sources

Gross Total Income

Less : Deductions

a. Sec 80G

b. Sec 80GGA

c. Sec 80GGC

d. Sec 80-IA

e. Sec 80-IAB

f. Sec 80-IB

g. Sec 80-IBA

h. Sec 80-IC

i. Sec 80-IE

j. Sec 80JJA

k. Sec 80JJAA

l. Sec 80P

Sec 80 P is one of the important deduction applicable to co-operative societies. Sec 80 P is as follows:

80P. (1) Where, in the case of an assessee being a co-operative society, the gross total income includes any income referred to in sub-section (2), there shall be deducted, in accordance with and subject to the provisions of this section, the sums specified in sub-section (2), in computing the total income of the assessee.

(2) The sums referred to in sub-section (1) shall be the following, namely :—

(a) in the case of a co-operative society engaged in—

(i) carrying on the business of banking or providing credit facilities to its members, or

(ii) a cottage industry, or

(iii) the marketing of the agricultural produce of its members, or

(iv) the purchase of agricultural implements, seeds, livestock or other articles intended for agriculture for the purpose of supplying them to its members, or

(v) the processing, without the aid of power, of the agricultural produce of its members, the whole of the amount of profits and gains of business attributable to any one or more of such activities ;

(b) in the case of co-operative society, being a primary society engaged in supplying milk raised by its members to a federal milk co-operative society, the whole of the amount of profits and gains of such business;

(c) in the case of a co-operative society engaged in activities other than those specified in clause (a) or clause(b) [either independently of, or in addition to, all or any of the activities so specified], so much of its profits and gains attributable to such activities as does not exceed fifteen thousand rupees; however, in the case of consumer’s co-operatives society, this deduction shall be Rs 100,000 in respect of the profits and gains from the other activities.

(d) in respect of any income by way of interest or dividends derived by the co-operative society from its investments with any other co-operative society, the whole of such income;

(e) in respect of any income derived by the co-operative society from the letting of godowns or warehouses for storage, processing or facilitating the marketing of commodities, the whole of such income;

(f) in the case of a co-operative society, not being a housing society or an urban consumers’ society, or a society carrying on transport business or a society engaged in the performance of any manufacturing operations with the aid of power, where the gross total income does not exceed twenty thousand rupees, the amount of any income by way of interest on securities chargeable under section 18 or any income from house property chargeable under section 22.

Explanation.—For the purposes of this section, an urban consumers’ co-operative society means a society for the benefit of the consumers within the limits of a municipal corporation, municipality, municipal committee, notified area committee, town area, or cantonment.

(2) In a case where the assessee is entitled also to the deduction under section 80H or section 80J, the deduction under sub-section (1) of this section, in relation to the sums specified in clause (a) or clause (b) or clause (c) of sub-section (2), shall be allowed with reference to the income, if any, as referred to in those clauses included in the gross total income, as reduced by the deductions under section 80H and section 80J.

(3) Nothing contained in this section shall apply to a co-operative society carrying on insurance business in respect of the profits and gains of that business computed in accordance with section 44.

III. Rates of income Tax applicable to co-operative societies.

Assessment Year 2022-2023

Where the total income does not exceed 10,000-10% of total income

Where the total income exceeds 10,000 but does not exceeds 20,000-1000+20% on the excess over 10,000

Where the total income exceeds Rs 20,000 -3000 plus 30% on the excess over 20,000

Long term capital gain tax-20%

Surcharge: 12% of income tax if total income exceeds 1 crore rupees (Subject to Marginal Relief)

Health and Education cess@4%.

Alternative Tax Regime-As per Sec 115 BAD

Section 115 BAD is an option to resident co-operative societies. Details are as follows.

Tax Rate: 22%

Add:Surcharge@10%

Add: Health and Education cess@4%.

Here income is computed without providing deductions and exemptions.

Alternate Minimum Tax (Sec 115 JC)

115JC. (1) Not withstanding anything contained in this Act, where the regular income-tax payable for a previous year by a person, other than a company, is less than the alternate minimum tax payable for such previous year, the adjusted total income shall be deemed to be the total income of that person for such previous year and he shall be liable to pay income-tax on such total income at the rate of eighteen and one-half per cent.

It is not applicable to a co-operative society which has exercised the option as per sec 115 BAD

Assessment Year 2023-2024

Where the total income does not exceed 10,000-10% of total income

Where the total income exceeds 10,000 but does not exceeds 20,000-1000+20% on the excess over 10,000

Where the total income exceeds Rs 20,000 -3000 plus 30% on the excess over 20,000

Long term capital gain tax-20%

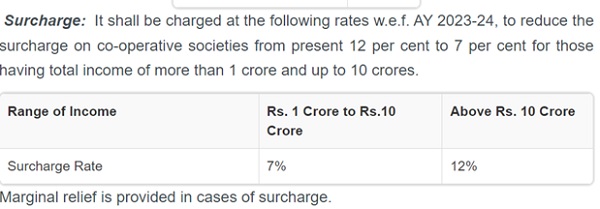

Surcharge:

Picture:1

(Source: https://taxguru.in/income-tax/income-tax-rates-fy-2023-24-ay-2024-25.html)

Health and Education cess@4%.

Alternative Tax Regime-As per Sec 115 BAD

Section 115 BAD is an option to resident co-operative societies. Details are as follows.

Tax Rate: 22%

Add:Surcharge@10%

Add: Health and Education cess@4%.

Here income is computed without providing deductions and exemptions.

Alternate Minimum Tax (Sec 115 JC)

115JC. (1) Notwithstanding anything contained in this Act, where the regular income-tax payable for a previous year by a person, other than a company, is less than the alternate minimum tax payable for such previous year, the adjusted total income shall be deemed to be the total income of that person for such previous year and he shall be liable to pay income-tax on such total income at the rate of fifteen percent.

It is not applicable to a co-operative society which has exercised the option as per sec 115 BAD

Assessment Year 2024-2025

Sec 115 BAE is a new section as per the Finance Act 2023.

Following section 115 BAE shall be inserted after section 115 BAD by the Finance Act, 2023, w.e.f 01/04/2024.

After section 115BAD of the Income-tax Act, with effect from the 1st day of April, 2024, the following section shall be inserted, namely:— “115BAE. (1)

Notwithstanding anything contained in this Act but subject to the provisions of this Chapter, other than those mentioned under section 115BAD, the income-tax payable in respect of the total income of an assessee, being a co-operative society resident in India, for any previous year relevant to the assessment year beginning on or after the 1st day of April, 2024, shall, at the option of such assessee, be computed at the rate of fifteen per cent. if the conditions contained in sub-section (2) are satisfied:

Provided that where the total income of the assessee includes any income, which has neither been derived from nor is incidental to, manufacturing or production of an article or thing and in respect of which no specific rate of tax has been provided separately under this Chapter, such income shall be taxed at the rate of twenty-two per cent. and no deduction or allowance in respect of any expenditure or allowance shall be made in computing such income:

Provided further that the income-tax payable in respect of the income, of the assessee deemed so under the second proviso to sub-section (4) shall be computed at the rate of thirty per cent.:

Provided also that the income-tax payable in respect of income, being short term capital gains derived from transfer of a capital asset on which no depreciation is allowable under the Act shall be computed at the rate of twenty-two per cent.:

Provided also that where the assessee fails to satisfy the conditions contained in sub-section (2) in any previous year, the option shall become invalid in respect of the assessment year relevant to that previous year and subsequent assessment years and other provisions of the Act shall apply to the assessee as if the option had not been exercised for the assessment year relevant to that previous year and subsequent assessment years.

(2) For the purposes of sub-section (1), the following conditions shall apply, namely:—

(a) the co-operative society has been set-up and registered on or after the 1st day of April, 2023, and has commenced manufacturing or production of an article or thing on or before the 31st day of March, 2024 and,—

(i) the business is not formed by splitting up, or the reconstruction, of a business already in existence;

(ii) does not use any machinery or plant previously used for any purpose.

Explanation 1.—For the purposes of sub-clause (ii), any machinery or plant which was used outside India by any other person shall not be regarded as machinery or plant previously used for any purpose, if the following conditions are fulfilled, namely:—

(A) such machinery or plant was not, at any time previous to the date of the installation, used in India;

(B) such machinery or plant is imported into India from any country outside India; and

(C) no deduction on account of depreciation in respect of such machinery or plant has been allowed or is allowable under the provisions of this Act in computing the total income of any person for any period prior to the date of installation of machinery or plant by the person.

Explanation 2.—Where any machinery or plant or any part thereof previously used for any purpose is put to use by the assessee and the total value of such machinery or plant or part thereof does not exceed twenty per cent. of the total value of the machinery or plant used by the assessee, then, for the purposes of sub-clause (ii), the condition specified therein shall be deemed to have been complied with;

(b) the assessee is not engaged in any business other than the business of manufacture or production of any article or thing and research in relation to, or distribution of, such article or thing manufactured or produced by it.

Explanation.—For the removal of doubts, it is hereby clarified that the business of manufacture or production of any article or thing shall include the business of generation of electricity, but not include a business of,—

(i) development of computer software in any form or in any media;

(ii) mining;

(iii) conversion of marble blocks or similar items into slabs;

(iv) Bottling of gas into cylinder;

(v) Printing of books or production of cinematograph film; or

(vi) any other business as may be notified by the Central Government in this behalf;

(c) the total income of the assessee has been computed,—

(i) without any deduction under the provisions of section 10AA or clause (iia) of sub-section (1) of section 32 or section 33AB or section 33ABA or sub-clause (ii) or sub-clause (iia) or sub-clause (iii) of sub-section (1) or sub-section (2AA) of section 35 or section 35AD or section 35CCC or under any of the provisions of Chapter VI-A other than the provisions of section 80JJAA;

(ii) without set off of any loss carried forward or depreciation from any earlier assessment year, if such loss or depreciation is attributable to any of the deductions referred to in clause (i); and

(iii) by claiming the depreciation, if any, under section 32, other than clause (iia) of sub-section (1) of the said section, determined in such manner as may be prescribed.

(3) The loss and depreciation referred to in sub-clause (ii) of clause (c) of sub-section (2) shall be deemed to have been given full effect to and no further deduction for such loss shall be allowed for any subsequent year.

(4) Where it appears to the Assessing Officer that, owing to the close connection between the assessee to which this section applies and any other person, or for any other reason, the course of business between them is so arranged that the business transacted between them produces to the assessee more than the ordinary profits which might be expected to arise in such business, the Assessing Officer shall, in computing the profits and gains of such business for the purposes of this section, take the amount of profits as may be reasonably deemed to have been derived therefrom:

Provided that in case the aforesaid arrangement involves a specified domestic transaction referred to in section 92BA, the amount of profits from such transaction shall be determined having regard to arm’s length price as defined in clause (ii) of section 92F:

Provided further that the amount, being profits in excess of the amount of the profits determined by the Assessing Officer, shall be deemed to be the income of the assessee.

(5) Nothing contained in this section shall apply unless the option is exercised by the person in the prescribed manner on or before the due date specified under sub-section (1) of section 139 for furnishing the first of the returns of income for any previous year relevant to the assessment year commencing on or after the 1st day of April, 2024, and such option once exercised shall apply to subsequent assessment years:

Provided that once the option has been exercised for any previous year shall not be allowed to be withdrawn for the same or any other previous year.”.

Information

Press Information Bureau

Government of India

Ministry of Cooperation

29 MAR 2023 5:38PM by PIB Delhi

Taxes on Cooperative Societies

As per Budget announcement 2023-24, following income tax related benefits are being proposed for the Cooperative Societies:

i. The new co-operative society formed on or after 01.04.2023, which commences manufacturing or production by 31.03.2024 and do not avail of any specified incentive or deduction, is proposed to be allowed an option to pay tax at a concessional rate of 15 per cent similar to what is available to new manufacturing companies. This announcement would benefit new cooperatives engaged in manufacturing/production activities.

ii. For sugar co-operatives, for years prior to assessment year 2016-17, if any deduction claimed for expenditure made on purchase of sugarcane has been disallowed, same shall be recomputed after allowing such deduction upto the price fixed or approved by the Government for such previous years. This decision of the Government will provide benefit of approximately

₹10,000 crore of principal amount of Income-Tax to sugar cooperatives. For this purpose, all sugar co-operatives, who are eligible for deduction, are required to approach the assessing officer, suitably.

iii. A higher limit of Rs. 2 lakh per member for cash deposits to and loans in cash by Primary Agricultural Cooperative Societies (PACS) and Primary Cooperative

iv. Agricultural and Rural Development Banks (PCARDBs) has been provided.

v. A higher limit of Rs. 3 Crore for TDS on cash withdrawal has been provided to cooperative societies.

Similarly, during Financial Year 2022-23, following tax benefits were also provided to Cooperative Societies:

a. Reduction in Minimum Alternate Tax (MAT): MAT reduced for cooperatives from 18.5% to 15%.

b. Reduction in surcharge on cooperative societies: Surcharge reduced from 12 % to 7% for co- operative societies having income between Rs. 1 to 10 Cr.

(Source: https://pib.gov.in/Pressreleaseshare.aspx?PRID=1911876)

(Republished with amendments)

Author Bio