Introduction: The Directorate of Income Tax (Systems) issues a crucial communication regarding High Risk Non-filer cases for the Assessment Year 2017-18. This article delves into the details of the communication, the Risk Management Strategy (RMS) Cycle 3, and the actions recommended for the concerned authorities.

Detailed Analysis:

1. Identification of Non-filers: The communication highlights the importance of filing income tax returns for taxpayers exceeding the prescribed limit. Non-filers with potential tax liabilities are identified through a thorough analysis of various data sources, including AIR/CIB data, TDS/TCS Statements, and overall taxpayer profiles.

2. RMS Cycle – 3 Execution: The Risk Management Strategy (RMS) Cycle 3 focuses on the non-filer category for the Assessment Year 2017-18. Approved rules and parameters guide the identification of High Risk Non-filer cases, providing a strategic approach to manage potential tax liabilities.

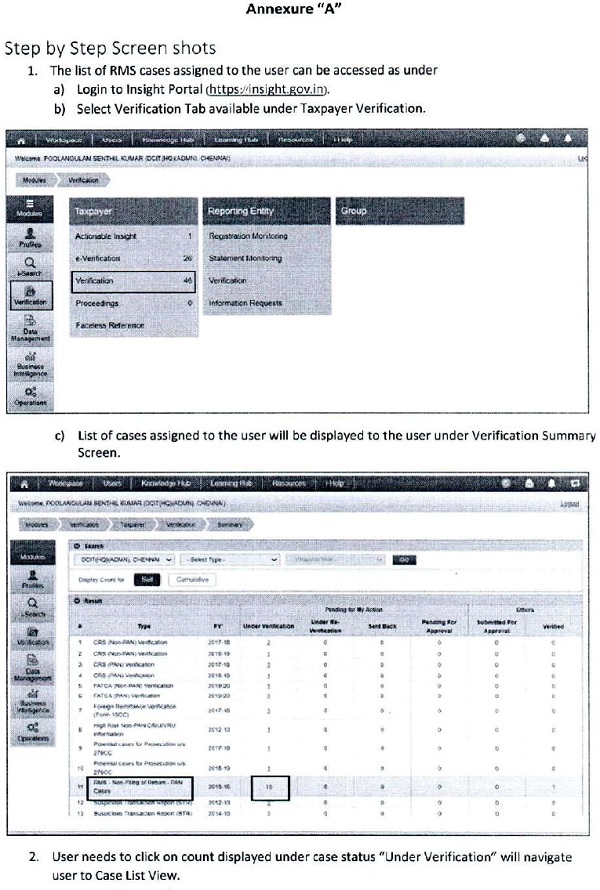

3. Insight Portal Access: The communication informs about the visibility of high-risk Non-filer cases on the Insight Portal. Jurisdictional Assessing Officers can access these cases through the ‘RMS – Non filing of Return PAN cases’ category on the Insight Portal, enabling them to review and take necessary actions.

4. Profile Views on Insight Portal: The Insight Portal offers Profile Views containing comprehensive information related to assigned cases. This includes comparative ITR information, financial profiles, address details, asset information, and third-party data. These details aid Assessing Officers in making informed decisions.

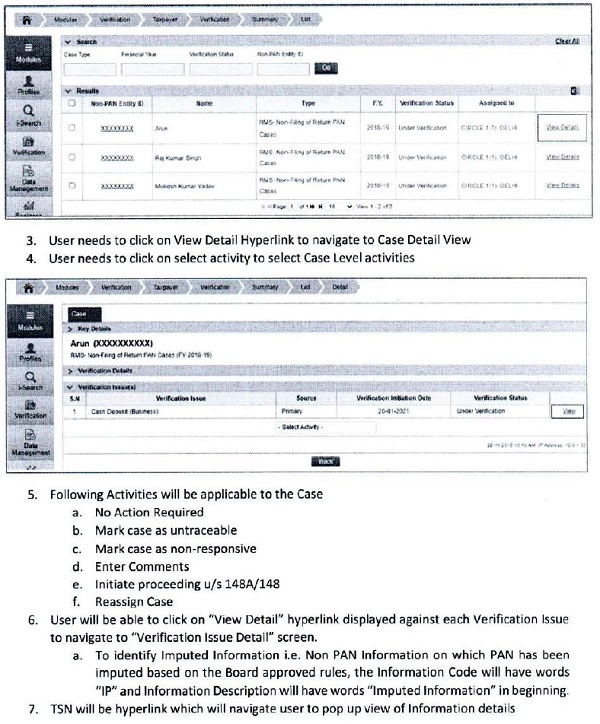

5. Activities Available on Case Detail Screen: The article outlines various activities accessible on the Case Detail screen, such as marking cases as untraceable, non-responsive, entering comments, case reassignment, declaring ‘No Return Required,’ and initiating proceedings under relevant sections of the Income Tax Act.

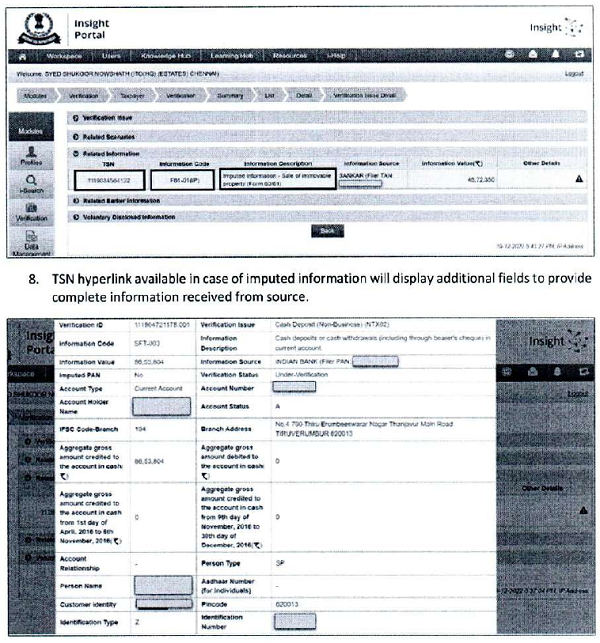

6. Action under Section 148A: The communication emphasizes that necessary action under Section 148A of the Income-tax Act, 1961, will be taken for the disseminated cases under RMS Cycle-3 for AY 2017-18. This action will be executed considering all relevant provisions of the Act.

7. Reference to Notifications/Instructions: Assessing Officers are encouraged to refer to relevant Notifications, Instructions, Circulars, and Standard Operating Procedures (S.O.Ps) issued by the Central Board of Direct Taxes (CBDT) concerning cases disseminated under the Risk Management System.

8. Technical Support: The communication provides information on seeking technical assistance. Users encountering technical difficulties can contact the Insight helpdesk through the provided helpline number and email address.

Conclusion: In conclusion, the Directorate of Income Tax (Systems) takes a proactive approach in disseminating information about High-Risk Non-filer cases for AY 2017-18. The article provides a comprehensive overview of the Risk Management Strategy, Insight Portal functionalities, and recommended actions for Assessing Officers, ensuring a systematic and informed approach in handling these cases.

*****

Insight Instruction No. 70

Directorate of Income Tax (Systems),

ARA Centre, Ground Floor, E-2,

Jhandewalan Extension,

New Delhi – 110055

F. No. DGIT(5)-2/ADG(5)-2/Jt.DIT(S)-2(3)/RMS Cycle – 3/445/2023-24 Date: 16/11/2023

To,

All Principal Chief Commissioner(s) of Income Tax/CCsIT

All Principal Director General(s) of Income Tax /DGsIT

All Principal Commissioner(s) of Income Tax /CsIT/CsIT(Admin & TPS)/CsIT (TDS)

All Principal Director(s) of Income Tax/DsIT

Sir/Madam,

Sub – Dissemination of certain High Risk Non-filer cases pertaining to the AY 2017-18 on Insight Portal selected under Risk Management Strategy (RMS) Cycle 3 – reg.

Kindly refer to the above.

2. A taxpayer who is having income above the prescribed limit or fulfils any other condition mentioned in section 139 of the Act is required to file return of income. Non-filers with potential tax liabilities are identified by analysing information received under, AIR/CIB data, TDS/TCS Statement etc. and overall taxpayer profile based on the information available in the database.

3. RMS Cycle – 3 for non-filer category of cases has been executed for AY 2017-18 on the basis of rules/parameters thereto approved by the Board under RMS (Risk Management Strategy) for identifying High Risk Non-filer cases with potential tax liabilities.

4. In respect of above, certain high-risk Non-filer cases for relevant assessment year(s) as approved by the Board have been made visible to the Jurisdictional Assessing Officers on Verification module of the Insight Portal with following case type – ‘RMS – Non filing of Return PAN cases’. The cases can be accessed on INSIGHT portal using following path‑

Insight Portal – Verification -Taxpayer – Verification – Case type – RMS -Non filing of Return PAN cases’

For detailed description of Case View and underlying Info, User may refer to the Annexure “A” enclosed.

5. Underlying information including various third-party data/information related to PAN of assigned cases may also be accessed on Profile Views of Insight Portal. Profile Views shows various information related to taxpayer including:

a. Comparative ITR information under Return Profile (TRP)

b. Comparative key values, financial ratios etc. under Financial Profile (TFP)

c. Details of various address, email, mobile numbers under, Master Profile (IMP)

d. List of accounts, immovable assets etc under Asset Details (TAD)

e. List of key persons, shareholders etc uncle, Relationship (TM)

f. Third Party Information, Aggregated TDS Payments, Aggregated GST Transactions, and other information under Taxpayer Annual Summary (TAS)

6. Following activities are available on Case Detail screen which can be accessed by clicking Initiate Activity drop down button.

a. Mark case as untraceable: This generic functionality allows user to mark such cases where the communications are not getting delivered to the taxpayers untraceable for feedback purpose.

b. Mark case as Non-Responsive: User can mark such crises where the communications are getting delivered to the taxpayer but the taxpayer is not responding to the queries sent on Compliance Portal through this functionality.

c. Enter Comments: User can record remarks at the case level.

d. Case Reassignment: The user can select multiple cases and re-assign/transfer them.

e. No Return Required: In Non-filing of Return (NMS): RMS cases, the user can mark a case as ‘No Return Required’, if the user comes to this conclusion post assessment of response submitted by the taxpayer.

f. Initiate Proceedings u/s 1484/148: The dropdown provides the user a generic technical functionality to initiate proceedings for RMS cases related to issuance of notice u/s 148A or notice u/s 148 of the Income Tax Act, 1961. The user may use this particular functionality for initiating proceedings related to issuance of notice u/s 148A for cases under RMS.

7. Further, necessary action u/s 148A of the Income-tax Act. 1961 in respect of the above disseminated cases for AY 2017-18 under RMS Cycle-3 shall be taken after taking into account all relevant applicable provisions of the Act.

8. The Assessing Officers may also further refer to relevant Notifications/Instructions/Circulars/S.O.Ps for cases disseminated under Risk Management System issued by the CBDT front time to time.

9. In case of any technical difficulty being observed, users my immediately contact OR write to Insight helpdesk. (Helpdesk number – 18001034216, Email id: helpdesk@insight.gov.in).

Yours faithfully,

(Ankit Verma)

Jt.DIT (Systems)-2(3)

Copy to:

1. PPS to Chairperson, Member (Admin & Faceless Scheme(s)). Member (A&J), Member (IT & R), Member (inv.), Member (L & 5), Member (TPS), CBDT and DGIT(S), Delhi & DGIT(S)-2, Bangalore, for information.

2. Nodal officer of ITBA, Insight i-Library, https://www.irsofficersonline.gov.in.

Jt.DIT (Systems)-2(3)