Goods and Services Tax (GST) – the new tax regime is much talked about as a major tax reform. It is a comprehensive tax regime to be levied on manufacture, sale and consumption of goods and services throughout India, to subsume central indirect taxes like excise duty, countervailing duty and service tax, as also state levies like value added tax, octroi and entry tax, luxury tax. In simple words, it is a “single taxation’ system which shall be on the supply of goods and services, right from the manufacturer to the consumer. In order to remove existing complexity of Indirect taxes in India, GST has been introduced. However, in the recent discussion with Finance Minister Arun Jaitley, the rollout of GST is likely to be settled by June 1 or July 1 considering in mind the mandatory timeline of September.

It is also expected that Finance Minister will announce the timetable for this ambitious tax reform in his budget speech on February 1, 2017. Hence, it is imperative to take necessary steps towards GST transition in case the provisional registration number is not applied by registered business in India. This is will not only help in smooth functioning of levy of taxes but also allows GST-registered businesses to claim tax credit to the value of GST they paid on purchase of goods or services as part of their normal commercial activity.

GST seeks to address challenges with the current indirect tax regime by

- broadening the tax base,

- eliminating cascading of taxes,

- increasing compliance, and

- Reducing economic distortions caused by inter-state variations in taxes.

Consistent with the federal structure of the country, it will have two components: one levied by the Centre (hereinafter referred to as Central GST), and the other levied by the States (hereinafter referred to as State GST). The proposed structure shall be as follows:

The proposed GST regime shall have the following features:

- It shall be a destination based taxation

- It shall have a Dual Administration – Centre and state

- State wise determination of taxable person – no more centralized registration

- Seamless credit amongst goods and services

The tax-rates are yet to be determined depending upon the type of industry, goods and services, but as per recent discussion of GST council on November 3, 2016 the tax rates would be at 4 slabs, i.e., 5%, 12%, 18% and 28%.

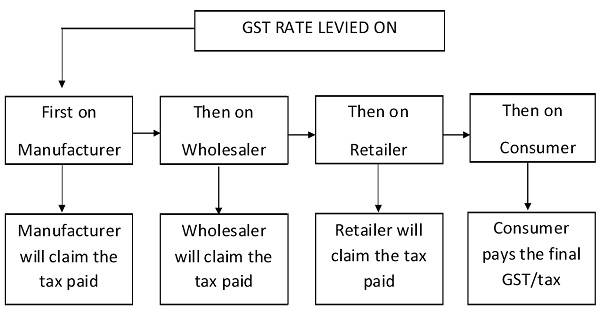

It is advisable that all the existing taxpayers registered under VAT, Service Tax, and Excise to migrate themselves into GST regime via GST Common portal maintained for the same. The applicability of GST can be understood by pictorial representation given below:

The major benefit of this structure is transparency and accountability of the registered taxpayers. In case you don’t pay tax on what you sell, you will not get credit for taxes on your inputs. That would mean you will buy from those who have already paid taxes on what they are supplying to you.

(Author can be reached at Pri.gera05@gmail.com)

Uploaded company reg.detail pan no. Import export code but not get provisional id in himachal perdesh .