CMA Awadh Jaiswal

1. Introduction

GST stands for “Goods and Services Tax”. GST Bill officially known as “The Constitution (122nd Amendment) Bill, 2014″received assent from The President of India on 8th September, 2016 and is going to be implemented in India from 1stApril, 2017.

GST is an Indirect tax reform and going to harmonize the indirect tax regime in India, minimizing the procedural and documentary compliance requirements, mitigating cascading effect of taxation and ultimately reducing the cost of production and inflation in the economy by subsuming a plethora of Central and State Level taxes.It is going to be a single tax on the supply of goods and services with the same provisions as against multipleacts & compliances and returns by subsuming below Central/State Level taxes:

Taxes Subsumed at Central Level:

– Central Excise Duty

– Additional Excise Duty

– Service Tax

– Additional Custom Duty (CVD)

– Special Additional Duty of Custom (SAD)

Taxes Subsumed at State Level:

– Sales Tax/ State level Value Added Tax

– Central Sales Tax

– Entertainment Tax

– Octroi/Entry Tax

– Purchase Tax

– Luxury Tax

– Taxes on Lottery, betting and gambling

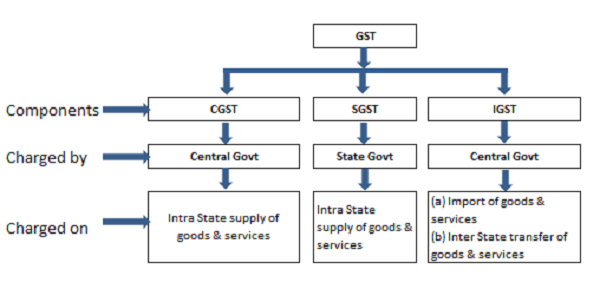

2. GST Mechanism : CGST/SGST/IGST

GST will be levied on each supply of goods and services. Centre will levy CGST, while state will levy SGST. Apart from this the Centre would levy and collect the Integrated Goods and Services Tax (IGST) on all Import of goods & services and inter-State supply of goods & services.

The input tax credit of CGST would be available for discharging the CGST liability on the output at each stage. Similarly, the credit of SGST paid on inputs would be allowed for paying the SGST on output. No cross utilization of credit would be permitted.Again the IGST mechanism has been designed to ensure seamless flow of input tax credit from one State to another. The inter-State seller would pay IGST on the sale of his goods to the Central Government after adjusting credit of IGST, CGST and SGST on his purchases. The exporting State will transfer to the Centre the credit of SGST used in payment of IGST. The importing dealer will claim credit of IGST while discharging his output tax liability (both CGST andSGST) in his own State. The Centre will transfer to the importing State the credit of IGST used in payment of SGST. This input tax credit mechanism can be simply understood by below diagram:

GST council on its meeting on 3rd November, 2016 prescribed the below Rates of GST:

| Rates | Description |

| 5 % | Lower rate for mass consumption of goods, i.e.-Medicines, Spices etc. |

| 12% | Meri rate for necessary goods |

| 18% | Standard rate for all common goods |

| 28% | Higher rate for luxury and demerit goods |

Zero tax rate will apply to 50% of the items present in the Consumer Price Index basket, including foodgrains such as rice and wheat.

- Registration under GST

> Every person shall have a Permanent Account Number issued under the Income Tax Act, 1961 in order to be eligible for grant of registration under Section 19 of the Model GST Law, except for a non-resident taxable person who may be granted registration on the basis of any other document as may be prescribed.

> Any supplier who carries on any business at any place in India and whose aggregate turnover exceeds threshold limit as prescribed (Rs. 20 lacs) in a year is liable to get himself registered. An agriculturist shall not be considered as a taxable person and shall not be liable to take registration. However, certain categories of persons mentioned in Schedule III of Model GST Law are liable to be registered irrespective of his threshold limit:

a) Persons making any inter-State taxable supply;

b) Casual taxable persons;

c) Persons who are required to pay tax under reverse charge;

d) Non-resident taxable persons;

e) Persons who are required to deduct tax under section 37;

f) Persons who supply goods and/or services on behalf of other registered taxable persons whether as an agent or otherwise;

g) Input service distributor;

h) Persons who supply goods and/or services, other than branded services, through electronic commerce operator;

i) Every electronic commerce operator;

j) An aggregator who supplies services under his brand name or his trade name; and\

k) Such other person or class of persons as may be notified by the Central Government or a State Government on the recommendations of the Council.

> Person who does not fall under Schedule –III may apply for registration voluntarily.

> A suomoto registration by department is also possible for the Person meeting the prescribed conditions of law.

> As compared to earlier service tax provisions, here there is no option to take centralized registration for services under Model GST Law.Person having multiple business vertical in the State, may apply for each vertical but not necessary.

> There will be common online registration, common return and common Challan for Central and State GST.

4. Payment of Tax, Returns under GST, Due date and Penalty:

a) Payment of Tax:

> Deposit made towards tax, interest, penalties shall be paid online using debit /credit cards, NEFT etc.Which will be credited to electronic cash ledger account.

> Self-assessed ITC claimed in the return shall be credited to electronic credit ledger account.

> Payment towards tax, interest, penalties can be made from electronic cash or credit ledger accounts subject to the rules, conditions prescribed.

b) Returns under GST

> Every registered dealer is required to file GST return for the prescribed tax period, however Government entity/PSU etc. not dealing in GST, persons exclusively dealing in exempted / Nil rated / non –GST goods or services would neither be required to obtain registration nor required to file returns under the GST law.

> Other key points related to GST return:

a) GST return can be filed online only.

b) There will be common e-return for CGST/SGST/IGST.

c) Filing of NIL return is mandatory.

d) Revised return can’t be filed. Any correction/modification in the return already filed can be done in subsequent returns only.

e) Return to be treated as valid only after payment of tax.

c) Types of return and due date to file

| Sl. No | Form No | Particulars | Due Date |

| 1 | GSTR-1 | Outward supplies made by taxpayer (other than compounding taxpayer and ISD) | 10th of next month |

| 2 | GSTR-2 | Inward supplies received by a taxpayer (other than a compounding taxpayer and ISD) | 15th of the next month |

| 3 | GSTR-3 | Monthly return (other than compounding taxpayer and ISD) | 20th of the next month |

| 4 | GSTR-4 | Quarterly return for compounding Taxpayer | 18th of the month next to quarter |

| 5 | GSTR-5 | Periodic return by Non-Resident Foreign Taxpayer | Last day of registration |

| 6 | GSTR-6 | Return for Input Service Distributor (ISD) | 15th of the next month |

| 7 | GSTR-7 | Return for Tax Deducted at Source | 10th of the next month |

| 8 | GSTR-9 | Annual Return | 31st Dec of next FY |

*only common purpose main forms are mentioned here, apart from this there exist a no of other forms as well.

d) Penalty for Late filing of Return:

> For Annual return: ₹ 100 /day for each day of default (max to 0.25% aggregate turnover)

> Other than annual return: ₹ 100 /day for each day of default (max to Rs.5000)

5. Conclusion:

GST is going to fulfill the concept of “One country-One tax” to a greater extent and has lot many advantages. But still the law is in the provisioning phase and there are issues which needs to be clarified in order to make the people aware of the clear provisions of the law and avoid any ambiguity. Still the Law is capable enough for creating the common market, promoting Investment boost and for supporting the Concept of Make in India and a lot more. In nutshell, it’s a great reform in Indian taxation system and definitely it is going to boost the Indian economy.

(Author is an “Oracle Finance Consultant” with “Wipro Technologies”, Chennai and can be reached at “jayaswalji@gmail.com”).

Disclaimer: Every efforts has been taken care of for making this article error free ,still the author assumes no responsibility for any errors which may be found there in. The article doesn’t covers all the provisions of the Model GST law and is for the purpose of basic understanding and sharing knowledge only. Practical implication of the provisions of the law may vary depending upon the actual case study, so it is advisable to take the expert opinion for any specific case study.

Author Bio