Can you imagine a situation, when even before receiving your hard earned money in your bank account, government demands tax on such income twice the amount for which you are actually liable? Yes, such a situation can happen when you are having your income from outside India, where you might be required to pay tax twice on the same income to the Indian Government, as well as the government of the country from whom you have earned money.

Taxation Rules of Foreign Income:

Any Nation State, taxes the Income of the persons on the basis of 2 criteria’s:

Let’s take an example: An Indian resident having a house property in UK is desirous of selling it. Now, tax implication on such will be as follows:

- He has to pay tax on capital gains in UK, as per source rule, in accordance with the laws of UK

- Further, since he is resident in India, his world income is taxable in India in accordance with the residence rule. Therefore, while filing his ITR in India, he has to include such capital gain in into account while preparing his computation of Income.

This leads to the situation of double taxation of same income, and therefore shrinking the net disposable income of the persons paying taxes.

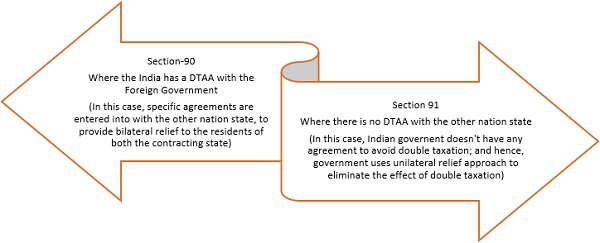

To Mitigate such a situation, government enters into various agreements with other/ partner countries to provide relief to its residents, and such an agreement with other nation states is known as Double Taxation Avoidance Agreement (DTAA) covered under section 90 & 91 of the Income Tax Act, 1961.

The government with the aim to provide transparent and justifiable taxation system to its residents, ensures to avoid the double taxation of same income, via:

How can you claim the Foreign Tax Credit (FTC)?

- To avail the benefit of FTC, you need to file form 67 on the Income Tax portal on or before the due date of filing of ITR

- A statement of Computation of Income of that country outside India

- A statement of the foreign tax deducted along with the proof (challan, TDS receipt etc.)

- A certificate or statement specifying the nature of Income and the manner of tax deducted from the tax authority outside India or the person responsible for deduction of such tax.

Other relevant details:

- FTC shall be available against the amount of tax, surcharge, and cess payable under Indian tax laws, but not against interest, fee, or penalty.

- FTC (Foreign Tax Credit) is the sum of the credit amounts estimated separately for each source of income originating in a specific nation.

- FTC shall be available against the amount of tax, surcharge, and cess payable under Indian tax laws, but not against fee, interest, or penalty.

- If the foreign tax is challenged, the FTC will not be available.

- FTC shall be available in the year in which the income corresponding to such tax has been offered or assessed to tax in India.

- Even tax payable under Section 115JB (Minimum Alternate Tax) is eligible for Foreign Tax Credit.

- The lower of the tax payable on such income under Indian tax legislation and the foreign tax paid shall be the FTC (Foreign Tax Credit).

- The Foreign Tax Credit is calculated by converting the currency in which the foreign tax was paid or deducted at the Telegraphic Transfer Buying Rate on the last day of the month immediately preceding the month in which the tax was paid or deducted.

Conclusion

The FTC (Foreign Tax Credit) guidelines have provided relief to worldwide Indian enterprises that derive a large portion of their revenue from foreign sources. The regulations have addressed a number of concerns that needed clarification or might cause undue hardship to the assessee. However, there are some long-standing issues in the foreign tax credit field that have yet to be addressed. Litigation on a variety of other issues is also a possibility.

About the Author

The author is  , FCA helping foreign companies in setting up and closure business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants is a well-established Chartered Accountancy firm founded in the year 1997 with its head office at New Delhi.

, FCA helping foreign companies in setting up and closure business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants is a well-established Chartered Accountancy firm founded in the year 1997 with its head office at New Delhi.