The taxation of dividends can result in double taxation, as companies pay taxes on their profits before distributing them to shareholders. This article examines the provisions of the Income Tax Act of India regarding dividend taxation and explores global practices in this area. It also raises questions about the fairness of double taxation and its potential impact on investments and economic growth.

Background

When someone invest in an equity of a company, they invest with the two major purpose of Capital appreciation and for Dividend, and accordingly capital appreciation i.e. capital gain is taxed under Income from Capital Gain and Dividend is taxed under Income from Other Source or Income from Business & Profession (under certain Cases). But Dividend which is getting taxed has been reached to us after paying taxes and it is not DTA, which means taxes which we as an investor is paying on dividend is under Double taxation.

Tax Provisions

So to understand this more briefly let us first understand the meaning of dividend under Income Tax 1961,

As per Section 2(22) dividend includes: –

(a) any distribution by a company of accumulated profits, whether capitalised or not, if such distribution entails the release of assets by the company to its,

(b) any distribution to its shareholders by a company of debentures, debenture-stock, or deposit certificates in any form, whether with or without interest, and any distribution to its preference shareholders of shares by way of bonus, to the extent to which the company possesses accumulated profits, whether capitalised or not;

(c) any distribution made to the shareholders of a company on its liquidation, to the extent to which the distribution is attributable to the accumulated profits of the company immediately before its liquidation, whether capitalised or not;

(d) any distribution to its shareholders by a company on the reduction of its capital, to the extent to which the company possesses accumulated, whether such accumulated profits have been capitalised or not;

(e) any payment by a company, not being a company in which the public are substantially interested, of any sum by way of advance or loan to a shareholder, being a person who is the beneficial owner of shares (holding not less than ten per cent of the voting power), or to any concern in which such shareholder is a member or a partner and in which he has a substantial or any payment by any such company on behalf, or for the individual benefit, of any such shareholder, to the extent to which the company in either case possesses accumulated profits;

but “dividend” does not include— (i) a distribution made in accordance with sub-clause (c) or sub-clause (d) in respect of any share issued for full cash consideration, where the holder of the share is not entitled in the event of liquidation to participate in the surplus assets ;

(ii) any advance or loan made to a shareholder or the said concern specified in Sec 2(22)(e) by a company in the ordinary course of its business, where the lending of money is a substantial part of the business of the company ;

(iii) any dividend paid by a company which is set off by the company against any sum previously paid by it and treated as a dividend within the meaning of Sec 2(22)(e), to the extent to which it is so set off; (iv) any payment made by a company on buy back of shares; (v) any distribution of shares pursuant to a demerger.

According to Explanation 2 of the section, The expression “accumulated profits” in sub-clauses (a), (b), (d) and (e), shall include all profits of the company up to the date of distribution or payment referred to in those sub-clauses, and in sub-clause (c) shall include all profits of the company up to the date of liquidation, but shall not, where the liquidation is consequent on the compulsory acquisition of its undertaking by the Government or a corporation owned or controlled by the Government under any law for the time being in force, include any profits of the company prior to three successive previous years immediately preceding the previous year in which such acquisition took place.

Explanation to the concept

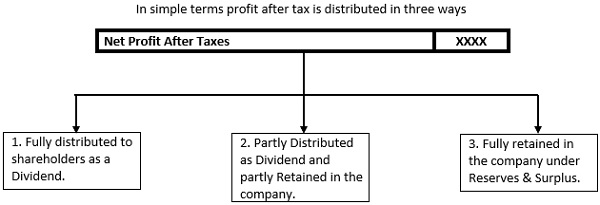

The definition of dividend clearly indicates that the dividend is distributed to the shareholders from the profit of the company accumulated in the form of reserves & surplus or profits earned till date of distribution.

But now let us see how this profit is calculated or accumulated in Reserves and Surplus

| Particular | Amount |

| Income from Operation & from Other Source | XXXX |

| Less: Expenses | XXXX |

| Less: Depreciation & Amortization | XXXX |

| Less: Interest on Debt (if any) | XXXX |

| Net Profit Before Taxes | XXXX |

| Less: Taxes on Profit | XXXX |

| Net Profit After Taxes | XXXX |

Now, the profit after tax is divided to total number of shares is called Earning per share (EPS) and when this EPS is distributed either wholly or partly to the shareholders is known as dividend per share (DPS). In case of partly distribution, company retain part of his earning for reinvestment or for future uncertainties or if inadequate profits in future dividend is distributed from this undistributed portion of profit.

In all three cases, dividend is payable by the company out of the profit after tax. So the question arises if the company has already paid taxes on the profit and dividend is nothing but apportion of it which is now a part of shareholders capital or we say owners capital, with this point of view dividend can also be said as withdrawal of our own money which we have invested or earned on investment after paying taxes and again including dividend into calculation of investors’ total income for calculating and paying taxes. Isn’t it double taxation on dividend? And if it is an income of the investor then it should be cost to the company and it must be able to get tax deduction on it but that’s not the case.

Let us understand this with an example:-

| (Amount in INR) | |

| Profit before Tax (PBT) | 1,000 |

| Less: Tax Rate @ 40% of PBT | 400 |

| Profit after tax (PAT) | 600 |

| Dividend declared by company out of PAT | 200 |

As mentioned above, the dividend declared by the company will be taxed in hands of shareholders on which tax is already paid by the company.

Further, on comparison with the taxability of the partnership firm, the exemption is provided to the profits distributed by the firm to its partner’s u/s 10(2A) while calculating the total income for the purpose of Income Tax. The said exemption u/s 10(2A) came into effect from Finance Act, 1992, which reads as “Before the changes made by the Finance Act, the system of levy of tax on firm involved double taxation. The firm as such was taxed in respect of its total income at rates varying from 5% to 18%. After deducting the tax payable by the firm, the balance of income was distributed among the partners and they were again taxed at appropriate rates.” And the profit distributed by the firm to their partners is also known as dividend.

Global Scenario

As the world has becomes a small market, the investors would not mind to shift their business from one country to another when it comes to tax saving. These days countries offering tax incentives or benefits attract investors and apparently these countries grow marginally in comparison to other countries. As a point to our discussion, there are countries which provide tax benefits on dividend income to investors and establish some of the best practices around the globe are discussed hereunder –

i) Australia: – In Australia dividend can be franked or unfranked. In franked dividend Australian resident company pays tax at rate of 30% and for the distribution of profit after tax, tax credit has been provided to the investors on the amount of dividend which has already been taxed. While in case of unfranked dividend company don’t pay taxes and it is taxable in hands of investors. Amount of franked and unfranked dividend or amount of tax credit is already provided to the investors at a time of payments.

ii) United Kingdom: – In UK, the dividend allowance has been provided to the recipient up to certain limit. And these limits has been declared by their revenue department for every fiscal year e.g. from 6th April 2018 to 5th April 2023 GBP 2,000 and for FY 2023-24 GBP 1,000 were announced.

iii) Malaysia: – In Malaysia, the dividend provided by the company to their shareholder is exempt fully.

Conclusion

When the profits of the firm distributed after tax is considered to be double taxed and exempted in the hands of partners then why the profits of the company distributed to their shareholders is taxed in the hands of investors? Why the dividends are getting taxed twice? Will there be any exemption for the investors in upcoming future? Whether India will adopting the best practice in near future or it will come up with some new idea to avoid double taxation, especially when the investor are eyeing on India for investments and India is looking for these investments to grow economy rapidly?

These are some of the question which is still unanswered and require clarification not only in India but in every other country in which dividend is taxable.

Author Bio