STATEMENT OF OBJECTS AND REASONS

1. Over the years, the pendency of appeals filed by taxpayers as well as Government has increased due to the fact that the number of appeals that are filed is much higher than the number of appeals that are disposed. As a result, a huge amount of disputed tax arrears is locked-up in these appeals. As on the 30th November, 2019, the amount of disputed direct tax arrears is Rs. 9.32 lakh crores. Considering that the actual direct tax collection in the financial year 2018-19 was Rs.11.37 lakh crores, the disputed tax arrears constitute early one year direct tax collection.

2. Tax disputes consume copious amount of time, energy and resources both on the part of the Government as well as taxpayers. Moreover, they also deprive the Government of the timely collection of revenue. Therefore, there is an urgent need to provide for resolution of pending tax disputes. This will not only benefit the Government by generating timely revenue but also the taxpayers who will be able to deploy the time, energy and resources saved by opting for such dispute resolution towards their business activities

3. It is, therefore, proposed to introduce The Direct Tax Vivad se Vishwas Bill, 2020 for dispute resolution related to direct taxes, which, inter alia, provides for the following, namely:—

a. The provisions of the Bill shall be applicable to appeals filed by taxpayers or the Government, which are pending with the Commissioner (Appeals), Income tax Appellate Tribunal, High Court or Supreme Court as on the 31st day of January, 2020 irrespective of whether demand in such cases is pending or has been paid;

b. the pending appeal may be against disputed tax, interest or penalty in relation to an assessment or reassessment order or against disputed interest, disputed fees where there is no disputed tax.

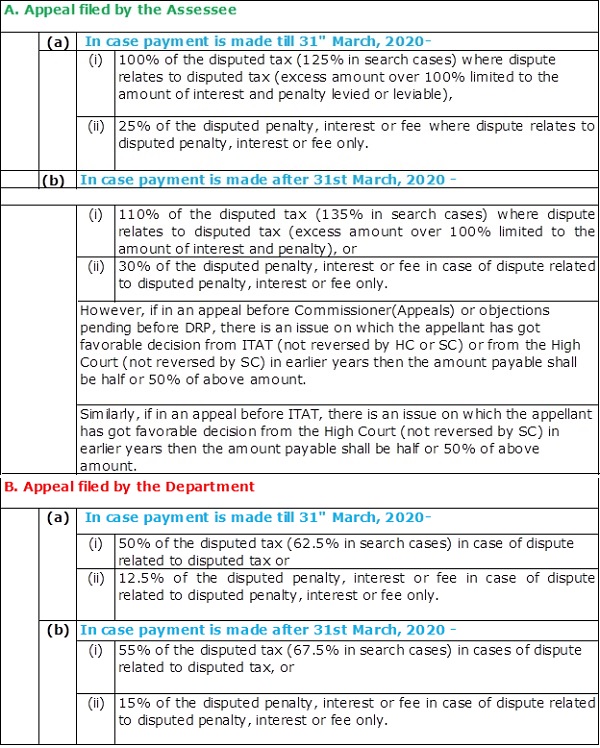

c. in appeals related to disputed tax, the declarant shall only pay the whole of the disputed tax if the payment is made before the 31st day of March, 2020 and for the payments made after the 31st day of March, 2020 but on or before the date notified by Central Government, the amount payable shall be increased by 10 per cent. of disputed tax;

d. in appeals related to disputed penalty, disputed interest or disputed fee, the amount payable by the declarant shall be 25 per cent. of the disputed penalty, disputed interest or disputed fee, as the case may be, if the payment is made on or before the 31st day of March, 2020. If payment is made after the 31st day of March, 2020 but on or before the date notified by Central Government, the amount payable shall be increased to 30 per cent. of the disputed penalty, disputed interest or disputed fee, as the case may be.

e. The Bill was passed by the Lok Sabha on 04-03-20 with certain amendments as cleared by the cabinet.

f. The salient feathers of the Amended Scheme as passed by the Lok Sabha on 04-03-20 are as under:

1. The epicenter of the scheme is “Disputed” amounts, be it tax, interest or penalty. The definition of Dispute is directly linked to the definitions of “tax, interest or penalty“ in respect of which appeal has been filed by the appellant and such appeal is pending on 31st January 2020. Relief is granted from the aggregate amount of disputed tax, disputed interest, disputed penalty and disputed fee.

2. The first thing therefore is to ascertain the eligibility of an appellant to the said scheme. Only those appellants will be eligible under this scheme in respect of whom disputed liability has been determined and the appellant has filed an appeal in respect of the disputed amount and the appeal is pending as on 31st January 2020. If no appeal has been filed or the time period prescribed for filing the appeal has expired then he is not eligible under the scheme subject to some exceptions.

3. Since the epicenter of the scheme is the determination of the disputed amount, the appellant must first ascertain the amount of disputed tax to be followed by the determination of disputed interest, penalty and fees.

4. For determination of the disputed tax under the scheme, extensive provisions have been made in the definition of the Appellant, Determination of disputed tax under different situations, Quantum of relief to be granted etc.

Sec 2(1)(b) defines an “appellant” under the scheme.

(i) a person in whose case an appeal or a writ petition or special leave petition has been filed either by him or by the income-tax authority or by both, before an appellate forum and such appeal or petition is pending as on the specified date;

(ii) a person in whose case an order has been passed by the Assessing Officer, or an order has been passed by the Commissioner(Appeals) or the Income Tax Appellate Tribunal in an appeal, or by the High Court in a writ petition, on or before the specified date, and the time for filing any appeal or special leave petition against such order by that person as not expired as on that date;

(iii) a person who has filed his objections before the Dispute Resolution Panel under section 144C of the Income tax Act, 1961 and the Dispute Resolution Panel has not issued any direction on or before the specified date;

(iv) a person in whose case the Dispute Resolution Panel has issued direction under sub-section (5) of section 144C of the Income-tax Act and the Assessing Officer has not passed any order under sub-section (13) of that section on or before the specified date;

(v) a person who has filed an application for revision under section 264 of the Income-tax Act and such application is pending as on the specified date;”

Sec 2(1)(j) defines Disputed tax :Disputed tax in relation to an assessment year or financial year, as the case may be, means the income-tax, including surcharge and cess (hereafter in this clause referred to as the amount of tax) payable by the appellant under the provisions of the Income-tax Act, 1961, as computed under different circumstances

| Case (1) : Assessment made by the AO | Returned Income | Assessed Income | |

| Income as per Return of Income | 70.00 | 70.00 | |

| Add: Disallowances- | 10.00 | ||

| Add: Under Reported Sales- | 50.00 | ||

| Assessed income – | 70.00 | 130.00 | |

| Tax Payable | 23.14 | 42.98 | |

| Disputed Tax | 19.84 | ||

–

| Case (2) : Appeal filed but pending before the CIT (A) | Not Contested | Contested |

| Undisputed/Disputed Income | 10.00 | 50.00 |

| Tax payable | 3.31 | 16.53 |

| Interest payable (Say for 2 years) | 1.19 | |

| Penalty u/s 270A-Misreporting @ 50% of the Tax | 0.60 | – |

| Amount payable | 5.10 | 16.53 |

| (a) Amount payable immediately-Income not contested | 5.10 | |

| (b) Amount Payable if paid upto 31-03-20 | 16.53 | |

| (c) Amount Payable if paid after 31-03-20 | 18.18 |

–

| Case (3) : Disputed tax due to Notice of enhancement given by the CIT (A) | Returned Income | Assessed Income |

| Assessed Income as per Order of AO | 50.00 | |

| Notice of enhancement given u/s 251 | – | 20.00 |

| Disputed Income | 70.00 | |

| Total Disputed Tax payable if paid upto 31-03-20 | 23.14 | |

| Total Disputed Tax payable if paid after 31-03-20 | 25.45 |

–

| Case (4) : Disputed Tax : Appeal disposed off by the ITAT | Appellant | Revenue |

| Income contested (Rs. 50 + 20 Lakhs enhancement) | 70.00 | 70.00 |

| Less: Relief granted by the ITAT | 40.00 | |

| Balance disputed income | 30.00 | 70.00 |

| (a) Amount Payable if paid upto 31-03-20 | 9.92 | 23.14 |

| (b) Amount Payable if paid after 31-03-20 | 10.91 | |

| Here the appellant has following options | Paid upto 31-03-20 | Paid after 31-03-20 |

| 1) Settle Self Appeal- Amount payable | 9.92 | 10.91 |

| 2) Settle Revenue Appeal- Amount Payable @ 50% | 11.57 | 12.73 |

| 3) Settle both the Appeals- Amount payable | 21.49 | 23.64 |

| If the appellant does not settle the Revenue Appeal and later on if the Revenue Appeal is decided against the appellant then the amount payable will as under | ||

| Tax payable | 23.14 | |

| Interest payable (Say for 3 years | 12.50 | |

| Penalty u/s 270A-Misreporting @ 50% of the Tax | 11.57 | |

| Final Amount payable | 47.21 | |

–

| Case (5) : Appeal filed before the High Court . | Appellant | Revenue |

| Disputed Income | 30.00 | 70.00 |

| Less: Relief Granted by the HC | 20.00 | – |

| Balance Disputed Income | 10.00 | 70.00 |

| (a) Amount Payable if paid upto 31-03-20 | 3.31 | 23.14 |

| (b) Amount Payable if paid after 31-03-20 | 3.64 | 25.45 |

| Here also the appellant has following options | Paid upto 31-03-20 | Paid after 31-03-20 |

| 1) Settle Self Appeal- Amount payable | 3.31 | 3.64 |

| 2) Settle Revenue Appeal- Amount Payable @ 50% | 11.57 | 12.73 |

| 3) Settle both the Appeals- Amount payable | 14.88 | 16.37 |

| If the appellant does not settle the Revenue Appeal and later on if the Revenue Appeal is decided against the appellant then the amount payable will as under | ||

| Tax payable | 23.14 | |

| Interest payable (Say for 4 years) | 16.66 | |

| Penalty u/s 270A-Misreporting @ 50% of the Tax | 11.57 | |

| Final Amount payable | 51.37 | |

–

| Case (6) : Disputed MAT Credit | Normal provisions | MAT provisions |

| Assessed Income as per Order of AO | 80.00 | 150.00 |

| Tax payable thereon | 24.72 | 29.70 |

| MAT Credit | 4.98 | |

| Additions to the Book Profit | 20.00 | |

| Revised Book Profit | 170.00 | |

| Tax payable thereon | 33.66 | |

| Revised MAT Credit | 3.96 | |

| In such a case the assessee has following options | ||

| a) Carry forward the revised MAT credit OR | 3.96 | |

| b) Pay an amount of difference in MAT Credit and carry forward the original MAT credit | 1.02 | |

| 4.98 | ||

| Case (7) : Disputed amount of unabsorbed Loss or Unabsorbed Depreciation to be carried forward | Returned Loss | Assessed Loss |

| Assessed Loss as per Order of AO | 90.00 | 90.00 |

| Less: Disallowance of expenses | 30.00 | |

| Revised Loss | 60.00 | |

| Less: Depreciation claimed | 50.00 | |

| Add: Depreciation allowed | 25.00 | 25.00 |

| Revised Loss after Depreciation | 35.00 | |

| In such a case the assessee has following options | ||

| a) Carry forward the reduced assessed unabsorbed Depreciation and Business Loss | 35.00 | |

| OR | ||

| b) Pay an amount of tax on reduced business Loss and reduced depreciation and C/F the original Loss | 30.00 | 9.92 |

| 25.00 | 8.27 | |

| 18.19 | ||

| Original Loss carried Forward | 90.00 | |

| Case (8) : Disputed Tax on Search operations | Returned Income | Assessed Income | |

| Income as per Return of Income | 70.00 | 70.00 | |

| Add: On Search operations | 50.00 | ||

| Returned/Assessed income | 70.00 | 120.00 | |

| Tax Payable | 21.63 | 39.67 | |

| Disputed Tax | 18.04 | ||

| (a) 125% of the Disputed Tax if paid before 31-03-20 | 22.55 | ||

| (b) 135% of the Disputed Tax if paid after 31-03-20 | 24.35 | ||

| In the above case whether 125% of the tax will be calculated on tax on search operation only or on the entire assessed income ? | |||

Analysis of Clarification issued by the CBDT Circular 7/2020/04-03-20

a) Appellate forum means CIT(A) , ITAT, HC, SC, SLP before the SC

b) Vivad se Vishwas means “VSV”

c) Assessee/appellant/declarant have been used inter-changeably

d) Deemed Appeal means where time to file appeal against any order has not expired.

1) Appeals eligible under the VSV

a. All cases where order has been passed but the time limit for filing appeal before the Appellate forum has not expired as on 31-01-20

b. All cases of Appeals, Writ, SLP in so far as they relate to quantification of tax liability AND ARE pending as at 31-01-20 before

i. Appellate Forum

ii. Dispute Resolution Panel (DRP)

iii. revision application under section 264

iv. Tax arbitration, conciliation or mediation

2) VSV against order of AAR can’t be used for proceedings pending before Authority of Advance Ruling (AAR) unless it relates to quantification of tax liability

3) Only disputed interest appeal : Appeals which covers only disputed interest (Tax dues not disputed) are eligible. However if the dispute involves Tax and Interest both then settling only tax dispute will automatically settle the disputed interest also without any payment i.e. total waiver of disputed interest.

4) Refund against disputed amount If the amount in dispute has been paid before filing declaration under VVS then the amount, to the extent it exceeds the disputed amount determined under VSV will be refunded without any interest u/s 244A.

5) Eligibility in case of search operations.

Appeals in Case of search operation are not eligible if the amount of disputed tax exceeds 5 Crore in that assessment year. However if say there are 7 assessments relating to search & seizure, out of which in 4 assessments, disputed tax is five crore rupees or less in each year and in remaining 3 assessments, disputed tax is more than five crore rupees in each year, declaration can he filed for 4 assessments where disputed tax is five crore rupees or less in each year.

6) Setting aside of assessment. If assessment has been set aside to reconsider the issues of, say additions and other issues which have not been remanded back then in such a case disputed tax shall be the tax which would have been payable had the addition in respect of which the order was set aside by the appellate authority was to be repeated by the AO. Further, the appellant shall also be required to settle other issues, which have not been set aside and in respect of which either appeal is pending or time to file appeal has not expired.

7) Appeals against disputed tax and disputed penalty If there are two appeals, one for disputed penalty and other for disputed tax then the appellant can settle the disputed tax appeal and the disputed penalty appeal will abate. However the appellant can’t settle the disputed penalty appeal only and continue with the disputed tax appeal.

8) Late Fees u/s 234E and 234F appeals: Such appeals are eligible under VSV and amount payable under VSV shall be 25% or 30% of the disputed fee, as the case may be. If the fee imposed under section 234E or 234F pertains to a year in which there is disputed tax, the settlement of disputed tax will not settle the disputed fee. If assessee wants to settle disputed fee, he will need to settle it separately by paying 25% or 30% of the disputed fee, as the case may be.

9) Qualifying and non-qualifying tax arrears

If the tax arrears include tax on issues that are excluded from the VSV such cases are not eligible under VSV. There is no provision under VSV to settle part of a pending dispute in relation to an appeal for an assessment year. For one pending appeal, all the issues are required to be settled and if anyone of the issues makes the declaration invalid, no declaration can be filed.

10) Writ against notice issued u/s 148 The assessee would not be eligible for VSV as there is no determination of income against the said notice.

11) Waiver application against interest u/s 234A, 234B or 234C: Such cases are not covered under VSV. Waiver applications are not appeal within the meaning of VSV.

12) Picking and choosing issues: Not allowed. With respect to one order, the appellant must chose to settle all issues.

13) Delay in deposit of TDS/TCS appeals: Such appeals are eligible under VSV which are disputed and pending in appeal. However, if there is no dispute related to TDS or TCS and there is delay in depositing such TDS/TCS, then the dispute pending in appeal related to interest levied due to such delay will be covered under Vivad se Vishwas.

14) Enhancement notice given by CIT(Appeals): The disputed tax in such cases shall be increased by the amount of tax pertaining to issues for which notice of enhancement has been issued.

15) Tax disputes covered under the VVS : Only disputes relating to income-tax are covered. Wealth tax , STT, CTT and equalization levy disputes are not covered.

16) Settlement of two appeals pending against (i) the assessment order under section 143(3) and another order under section 147/143(3) passed for the same assessment year then appellant an option to settle either of the two appeals or both appeals for the same assessment year. If he settles both the appeals then the disputed tax would be the aggregate amount of disputed tax in both appeals.

17) Appeals for disputed penalty only: If time to file appeal in ITAT against the order of CIT(A) has not expired then such cases will be treated as deemed appeal cases which are eligible under VSV.

18) Prosecution instituted and pending in court. are not covered under VSV. However, where only notice for initiation of prosecution has been issued with reference to tax arrears, the taxpayer has a choice to compound the offence and opt for VSV.

19) Appeal and Rectification both pending: In such cases the disputed tax would be calculated after giving effect to the rectification order passed, if any.

20) Calculation of disputed when demand paid while being in appeal

During assessment an addition is made and additional demand of Rs. 16,000 has been raised, which comprises of disputed tax of Rs. 10,000 and interest on such disputed tax of Rs.6000. Penalty has been initiated separately. Assessee has paid the demand of Rs. 14,000 during pendency of appeal; however interest under section 220 of the Act is yet to be calculated. In such cases the disputed tax of Rs 10,000 (at 100%) is to be paid on or before 31″ March 2020. Since he has already paid Rs. 14,000, he would be entitled to refund of Rs. 4,000 (without section 244A interest). Further, the interest leviable under section 220 and penalty leviable shall also be waived.

21) Calculation of disputed tax when order has been set aside: To illustrate, The AO made two additions of Rs 20,000/- and Rs 30,000/-. The tax on this comes to Rs 6,240/- and Rs 9,360/– and interest comes toRs.2,500 and Rs.3,500 respectively. CIT(A) has confirmed the two additions.

ITAT confirmed the first addition (Rs 20,000/-) and set aside the second addition (Rs 30,000/-) to the file of AO for verification with a specific direction. Assessee appeals against the order of ITAT with respect to first addition. In such a case the assessee can avail the VSV for both the additions. In this case the disputed tax would be the sum of disputed tax on both the additions i.e. Rs. 6240/plus Rs. 9,360/-

22) The amount of tax required to be paid to avail the benefit of the VSV shall be in accordance with the Table produced below.

23) Credit of taxes paid earlier against disputed tax: The amount payable by the appellant under VSV shall be determined by the DA and credit for taxes paid against the disputed tax before filing declaration shall be available to the appellant.

24) Credit of TDS to deductee when Deductor settles TDS appeal (against order U/S 201): The deductee shall be allowed to claim credit of taxes in respect of which the deductor has availed of dispute resolution under VSV. However, the credit will be allowed as on the date of settlement of dispute by the deductor and hence the interest as applicable to deductee shall apply.

25) Settlement of disallowance u/s 40(a)(i)/(ia) on settlement of TDS default:

Where an appellant settles TDS liability as deductor of TDS under VSV (i.e. against order u/s 201), then he will he get consequential relief of expenditure allowance under proviso to section 40(a)(i)/(ia) in the year in which the tax was required to be deducted.

To illustrate, If the dispute is settled with respect to order under section 201, appellant will not be required to pay any tax on the issue relating to disallowance under section 40(a)(i)/(ia). Further if the appellant has made payment against the addition representing section 40(a)(i)/(ia) disallowance, the appellant shall not be entitled to interest under section 244A of the Act on amount refundable under VSV

26) Settlement of TDS default: If a deductor fails to deduct TDS from income paid to the deductee and the Deductee has settled his appeal relating to assessment of an income which was not subjected to TDS then such deductor would not be required to pay the corresponding TDS amount. However, he would be required to pay the interest u/s 201(IA) which he can settle under VSV at 25% or 30% of the disputed interest.

27) Separate appeals for assessment and penalty: If the appellant has 2 appeals i) against assessment order and ii) against penalty order relating to same assessment then he can settle the appeal against assessment order and the penalty appeal will be automatically covered.

28) Part relief in appeal: For example if there are 5 issues in appeal 2 of which has been decided in favour of the appellant and 3 in favour of the department. Under the VSV an appellant has a choice, i) to settle his appeal on 3 issue ii) to settle departmental appeal on 2 issues iii) or to settle both the appeals. If he decides to settle only his deemed appeal, then department would be free to file appeal on the two issues (where the assessee has got relief) as per the extant procedure laid down and directions issued by the CBDT.

29) Prior favourable order from the SC : If the appellant has got decision in his favour from SC on an issue, there is no dispute now with regard to that issue and he need not settle that issue. If that issue is part of the multiple issues, the disputed tax may be calculated on other issues considering nil tax on this issue.

30) Issues contested and not contested in appeal: Addition was made u/s 143(3) on two issues whereas appeal filed only for one addition then under VSV interest and penalty will be waived only in respect of the issue which is disputed in appeal and for which declaration is filed. Hence, for the undisputed issue, the tax, interest and penalty shall be payable,

31) Prior order in favour of the appellant:

In this case, on the issue where the taxpayer has got relief from ITAT in an earlier year (not reversed by the HC or SC) the disputed tax shall be computed at 50% of the normal rate of 100%, 110%, 125% or 135%, as the case may be.

32) Option for settlement of all appeals : The appellant will option to settle his own appeal or settle the departmental appeal or settle both the appeals. If the departmental appeal is not settled then the issue in appeal will remain live and may be decided against the appellant in future. In that case the appellant will have to pay full tax, interest and penalty. For settlement of both the appeals the appellant will have to pay 100% of disputed tax as per his appeal and 50% of the disputed tax as per departmental appeal.

33) Refund of amount paid under VSV: Any amount paid in pursuance of a declaration made under the VSV shall not be refundable under any circumstances.

34) Reinstatement of Appeal: There is no question of reinstatement of appeal because appeals are to be withdrawn before the grant of certificate by DA. After the grant of certificate by DA the appellant is required to withdraw appeal.

35) Intimation of payment under VSV: The declarant has not only to pay the amount determined VSV within but also to intimate the DA of the fact of payment.

36) Immunity from levy of interest, penalty or prosecution: On passing of an order the VSV the DA shall not institute any proceeding for any offence; impose penalty, or charge any interest in respect of tax arrears. This shall be reiterated in the order under passed by DA.

37) Rectification of Order: The DA shall be able to amend his order under clause 5 to rectify any apparent errors.

38) Appeal against the Order under VSV : Appeal before any appellate forum against the order under VSV will not be acceptable.

39) Withdrawal of Departmental appeal : On intimation of payment to the DA the department shall withdraw department appeals.

40) Financial Difficulty : If payment is not made as per order passed under VSV for any reason or for financial difficulties, the declaration will be null and void.

41) Appeal effect :In cases where demand has been reduced by giving appeal effect the AO shall pass order under the relevant provisions of VSV to create demand against which the amount payable shall be adjusted.

42) Immunity from prosecution: Total immunity from prosecution in cases where an order is passed by the DA that the amount payable under VSV has been paid by the declarant.

43) No Acquiescence: (to acquiesceis to agree to something or to give in). If an issue has been settled under VSV then the Revenue/Appellant can’t contend that they have acquiesced in the decision on the disputed issue by settling the dispute and therefore same position to apply in other cases on the same issues.

44) Unabsorbed MAT, Loss or Depreciation to be C/F : Two options

include the amount of tax related to such MAT credit or loss or depreciation in the amount of disputed tax and carry forward the MAT credit or loss or deprecation

to carry forward the reduced tax credit or loss or depreciation. CBDT will prescribe the manner of calculation in such cases.

45) Secondary Adjustments -International taxation : Secondary adjustment under section 92CE consequent to primary adjustments will be applicable.

46) Setting precedent: If an appellant has settled the dispute under VSV in an assessment year then it is not open for Revenue to take a stand that the additions have been accepted by the appellant and hence he cannot dispute it in future assessment years.

47) Amount payable under the scheme

Errors and omissions may kindly be brought to the notice of the author.

Disclaimer: This write up is meant only for academic use. Readers are expected to consultant their professional consultants before acting on it. The author assumes no civil, criminal or financial liability for any action taken on the basis of this write-up.

Author Bio

DTVSV ONLINE FORMREQUIRES TAX IN SEARCH CASE WHERE AS IT WAS NOT A SEARCH CASE..

WHAT TO FILL IF NIL

in case of power generation companies, if the said amount is recoverable from customer then again tax is applicable to the income. Hence there is a chance of double taxation of the same amount

weather payment under VSVS is a tax expenses or business expenses

Whether credit for appeal fees paid earlier can be taken against laibilty to pay tax under dtvsv

whether Department Appeal pending at High Court in respect of Block Assessment u/s 158BC covered in DTVSV Scheme.?