1. A new section 206AB is introduced in the Finance Act 2021 for deduction of tax at source at higher rates to identify non-filers of Income Tax Returns. These defaulters will be identified and higher Tax Deducted at Source (TDS) be levied on them. Section 206AB is applicable w.e.f. 01 July 2021

This section mandated that all non-filers of income tax return (ITR) for the past two fiscal years will be subjected to higher TDS. These non-filers are called specified persons under sec 206AB of the Income Tax Act

2. Specified Person:The “specified person” means a person:

(a) who has not filed the returns of income for both of the two financial years immediately prior to the financial year in which tax is required to be deducted and

(b) Where the time limit of filing return of income under sub-section (1) of section 139 has expired for both the financial years.

(c) The aggregate of tax deducted at source and tax collected at source in his case is rupees fifty thousand or more in each of these two previous years.

3. Higher Rate of TDS: The tax shall be deducted at the higher of the following rates: –

(a) At twice the rate specified in the relevant provision of the Act

(b) At twice the rates in force

(c) At the rate of five percent

4. Illustration: M/S BEL is required to deduct tax at source @ 2% on payment to MR. Kundra, a contractor on 10th July 2021. Compliance Check to ascertain whether Mr. Kundra is a specified person or not is as explained below:

| (a) | The tax required to be deducted in 2021-22 |

| (b) | Financial Years immediately prior to FY – 2020-21 & 2019-20 |

| (c ) | The time limit of filing a return has not expired for 2020-21. (For FY 2020-21, the time limit is 30th Sep 2021) |

| (d) | Thus, M/S BEL has to check whether Kundra Agency has filed ITR for both the FY 2019-20 & 2018-19 |

| (e) | Further, it has to check whether the aggregate of TDS and TCS is Rs. 50000/- or more in each of the years 2019-20 & 2018-19. |

4.1 TDS @ 5% is required to be deducted by M/S BEL if Mr. Kundra is non-compliant with ALL the following cases

(a) ITR for FY 2019-20 –not filed

(b) ITR for FY 2018-19 –not filed

(c) The aggregate of TDS & TCS of Mr. Kundra in 2019-20> Rs. 50000

(d) The aggregate of TDS & TCS of Mr. Kundra in 2018-19 > Rs. 50000

4.2 If the provisions of section 206AA apply to a specified person, in addition to the provision of this section, the tax shall be deducted at higher of the two rates provided in this section and section 206AA. (Section 206AA of the Income-tax Act, 1961 provides that if PAN is not furnished by the payee, the withholding tax rate would be 20% or the rate in force, whichever is higher.)

4.3 Thus, if the specified person, Mr. Kundra has not furnished PAN Number to M/S BEL the tax is required to be deducted @ 20%.

5. This provision is not applicable on TDS under the following sections: –

Section 192A – Payment of accumulated balance due to an employee

Section 194B – Winnings from lottery or crossword puzzle

Section 194BB – Winning from a horse race

Section 194LBC – Income in respect of investment in securitization trust

Section 194N – Payments of certain amounts in cash

6. Compliance Check Functionality: Income Tax Department has provided a new functionality “Compliance Checkto facilitate tax deductors/collectors to verify if a person is a“Specified Person” as per section 206AB & 206CCA.

This functionality is made available through Reporting Portal of the Income-tax Department (https://report.insight.gov.in).

8. Step by Step procedure to register on Portal and do Compliance Check

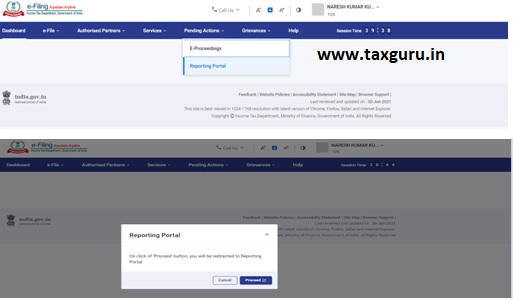

Login to www.incometax.gov.in with a TAN credential. Click on Pending Action > Reporting Portal

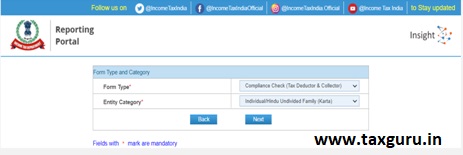

You will be redirected to Reporting Portal. Select Form Type “Compliance Check (Tax Deductor & Portal)

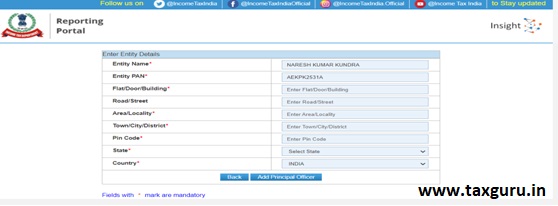

Entity Name & PAN Number will be Auto populated. Entered Address details and click on Principal officer.

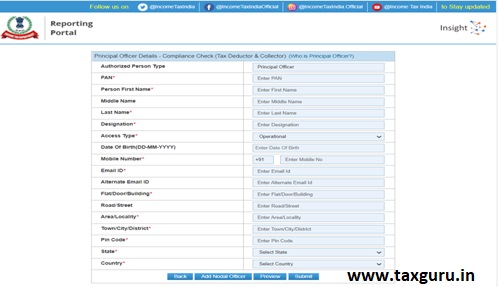

Enter the details of the principal officer & click on Submit.

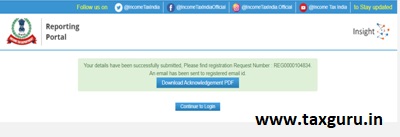

Download Acknowledgment / Continue to login

9. Accessing the functionality on Reporting Portal – by Principal Officer

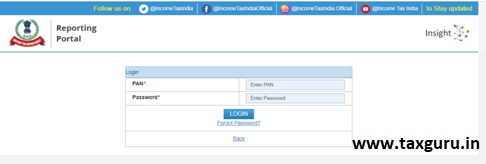

Go to Reporting Portal at URL https://report.insight.gov.in. On the left sidebar of the Reporting Portal homepage, click the Login button

Enter the required details (of Principal Officer) in the respective fields (PAN and Password as received in the email or updated password) and click Login to continue.

If Principal Officer’s PAN is registered for multiple Forms & ITDREIN, he/she needs to select Form type as Compliance Check (Tax Deductor & Collector) and associated ITDREINs from the drop-down.

Select Authorized person from the drop-down menu. Click on proceed.

10. Compliance Check for Section 206AB & 206CCA

After successfully logging in, the home page of Reporting Portal appears. Click on the Compliance Check for Section 206AB & 206CCA link provided as a shortcut on the left panel.

Upon clicking Compliance Check for Section 206AB & 206CCA on the home page, the compliance check functionality page appears.

Through the functionality, tax deductors or collectors can verify if any person (PAN) is a “Specified Person” as defined in Section 206AB & 206CCA.

The same can be done in two modes: · PAN Search: To verify for single PAN · Bulk Search:

To verify for PANs in bulk PAN Search (Single PAN Search)

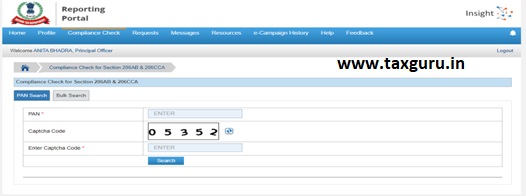

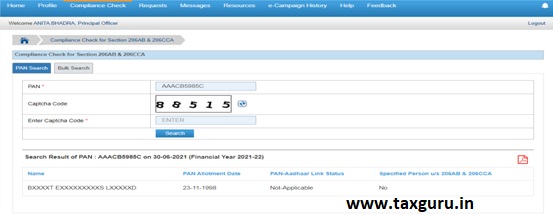

Step 1: Select PAN Search tab under Compliance Check for Section 206AB & 206CCA functionality.

Step 2: Enter valid PAN & captcha code and click Search.

Step 3: Click the PDF icon to download the details in PDF format.

Following Output result will be displayed upon entering a valid PAN & captcha code.

The output result will not be shown if an Invalid PAN is entered. Output Result-

- Financial Year: Current Financial Year

- PAN: As provided in the input.

- Name: Masked name of the Person (as per PAN).

- PAN Allotment date: Date of allotment of PAN.

- PAN-Aadhaar Link Status: Status of PAN-Aadhaar linking for individual PAN holders as of date. The response options are Linked (PAN and Aadhaar are linked), Not Linked (PAN & Aadhaar are not linked), Exempt (PAN is exempted from PAN-Aadhaar linking requirements as per Department of Revenue Notification No. 37/2017 dated 11th May 2017), or Not-Applicable (PAN belongs to non-individual person).

- Specified Person u/s 206AB & 206CCA: The response options are Yes (PAN is a specified person as per section 206AB/206CCA as on date) or No (PAN is not a specified person as per section 206AB/206CCA as on date). The output will also provide the date on which the “Specified Person” status as per section 206AB and 206CCA are determined.

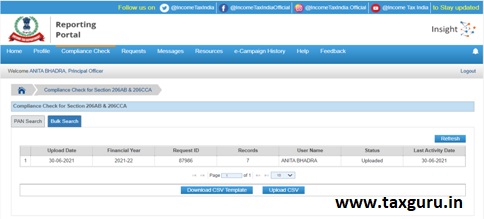

Bulk Search

Step 1: Select the “Bulk Search” tab.

Step 2: Download the CSV Template by clicking on the “Download CSV Template” button.

Step 3: Fill the CSV with PANs for which “Specified Person” status is required. (Provided PANs should be valid PANs and count of PANs should not be more than 10,000).

Step 4: Upload the CSV by clicking on the “Upload CSV” button.

Step 5: The uploaded file will start reflecting with Uploaded status.

The status will be as follows:

- Uploaded – The CSV has been uploaded and pending processing.

- Available – Uploaded CSV has been processed and results are ready for download.

- Downloaded – The user has downloaded the output results CSV.

- Link Expired – Download link has been expired. Step 6: Download the output result CSV once the status is available by clicking on the Available link. Step 7: After downloading the file, the status will change to Downloaded and after 24 hours of availability of the file, the download link will expire and the status will change to Link Expired. Output Result (CSV): Output result CSV file will have the following details:

- Financial Year: Current Financial Year

- PAN: As provided in the input. Status shall be “Invalid PAN” if provided PAN does not exist. · Name: Masked name of the Person (as per PAN).

- PAN Allotment date: Date of allotment of PAN.

- PAN-Aadhaar Link Status: Status of PAN-Aadhaar linking for individual PAN holders as of date. The response options are Linked (PAN and Aadhaar are linked), Not Linked (PAN & Aadhaar are not linked), Exempt (PAN is exempted from PAN-Aadhaar linking requirements as per Department of Revenue Notification No. 37/2017 dated 11th May 2017), or Not-Applicable (PAN belongs to non-individual person).

- Specified Person u/s 206AB & 206CCA: The response options are Yes (PAN is a specified person as per section 206AB/206CCA as on date) or No (PAN is not a specified person as per section 206AB/206CCA as on date). The output will also provide the date on which the “Specified Person” status as per section 206AB and 206CCA are determined.

Disclaimer: The article is for education purposes only.

The author can be approached at caanitabhadra@gmail.com

Author Bio

Hi,

Can it happen that person marked specified at start of financial year, status can change back during the course of year at any time ?

For transactions after the due date of ITR filing, a compliance check is required to be run on the portal again.

If transaction occurs in the month of December 2021, should the compliance check be run in portal (As due date of 139(1) has expired and thus status of F.Y. 20-21 has to be checked) or the check done in the beginning of the year should be applied?