SUSHIL CHANDRA

Chairman, CBDT &

Special Secretary to the Government of India

(GOVERNMENT OF INDIA

Ministry of Finance/Department of Revenue

Central Board of Direct Taxes

North Block, New Delhi-110001

E-mail : chairmancbdt@nic.in

Tele : 23092648 & Telefax : 23092544

D.O.F.No. 225/256//2018/ITA.II

Dated the 4th of July, 2018

My Dear Pr. Chief-Commissioner

You may recall that vide Instruction No. 17/2015 dated 9th November, 2015, Board had issued Guidelines for constitution of Local Committees in each of the Pr. CCIT Regions to expeditiously deal with taxpayers’grievances arising from High Pitched Scrutiny Assessments. The Committees were required to dispose of taxpayers’grievance after examining the case on parameters such as high-pitched additions on frivolous grounds, non-observance of principles of natural justice, non-application of mind, gross negligence etc. on the part of Assessing Officer. In cases where Local Committee found the order to be unreasonable or high-pitched, they were required to submit report to the concerned Pr. CCIT/CCIT so that proper administrative actions could be taken in such cases.

2. In last three years, the performance of Local Committees has not been found to be satisfactory. Last Year i.e. for 2016-2017, after follow-up from the Board, Pr. CCsIT furnished their report on cases held to be high-pitched by the Local Committees. In some of the instances/cases, these reports were found to be deficient/incomplete. For 2017-2018, not a single report of Local Committee from any of the Regions has been received in the Board. It may be mentioned that vide Instruction No. 17/2015, Pr. CCsIT were required to highlight outcome of work of Local Committees in their monthly DO Letters to the respective Zonal Member, however, it is observed that very few charges are following this practice. I have also got a personal feedback from some of the charges that Local Committees have not been duly reconstituted after transfer/promotion of Members of the existing Local Committee. I have also been informed that meetings of the Local Committee are not being held regularly in most of the Regions. You would also appreciate that all these deficiencies in functioning of Local Committees are hampering their effectiveness in tackling high-pitched assessments in an institutional manner.

3. Therefore, I would like to take this opportunity to emphasise that it is necessary to give due attention by the Pr. CCsIT themselves to monitor performance of Local Committees on a regular basis so that these Committees serve as a useful mechanism/institution to curb high-pitched assessments in the Income-tax Department. In addition to the mechanism outlined in Instruction No. 17/2015, following further steps should also be taken in cases which are found to be high-pitched by the Local Committees:

3.1 Wherever Local Committee has taken a view that addition made in the assessment order is high-pitched, explanation of the Assessing Officer should invariably be called for. Wherever required, administrative action such as inter-city transfer of the concerned Assessing Officer to non-sensitive post should be taken in such cases without any delay. Further, appropriate disciplinary action should also be taken/initiated in these cases;

3.2 No coercive action should be taken for recovery of demand in cases which have been identified as high-pitched by the Local Committee;

3.3 The concerned Commissioner (Appeals) should be requested to expedite hearing in such cases.

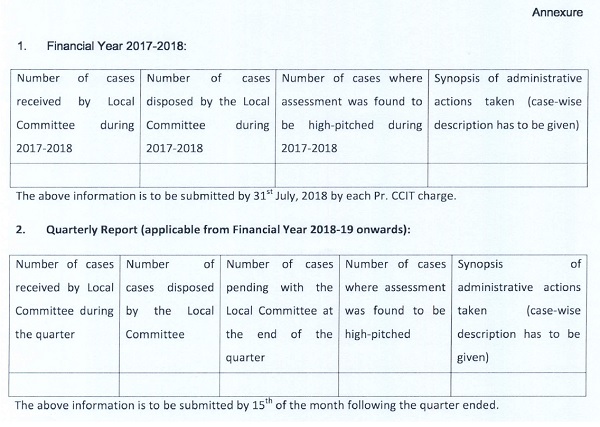

4. All Pr. CCsIT are requested to furnish the reports of Local Committees regarding assessments framed during the Financial Year 2017-2018 by 315′July, 2018 to Member (IT&C) as per the enclosed format. Thereafter, report of Local Committee would be required to be furnished to the Board every quarter as per the prescribed format.

5. I would also like that proper publicity in this regard may also be given at the local level. With the above initiatives along with your active involvement, I am hopeful that in future, Local Committees would inspire the taxpayers to place their grievances arising from high-pitched assessments before the Local Committees for appropriate redressal.

Enclosure: as above

Yours sincerely,

(Sushil Chandra)