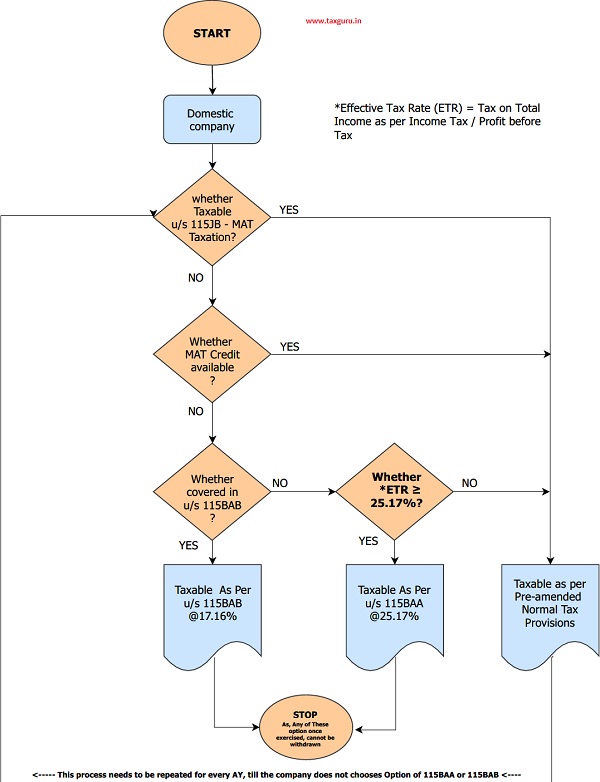

Government has brought in the Taxation Laws (Amendment) Ordinance 2019 and announces major relief in corporate tax for domestic companies, in order to boost the Make in India initiative. Corporate tax reduced to 22% (Effective Tax Rate 25.17% inclusive of Surcharge and Cess) for domestic firms while for new manufacturing companies, tax rate has been brought down to 15% (Effective Tax Rate 17.01% inclusive of Surcharge and Cess). Further Minimum alternate Tax Rate been reduced to 15% from 18.5% for Company availing exemptions. Article discusses Impact of recent changes on Tax rate and MAT.

| Particulars | Section 115BAA Tax on income of certain domestic companies. |

Section 115BAB Tax on income of certain new domestic manufacturing companies. |

| Applicability | At the Option of the Assessee, option once exercised, cannot be withdrawn | At the Option of the Assessee, option once exercised, cannot be withdrawn |

| Applicable Assessment Year | AY 2020-21 onwards | AY 2020-21 onwards |

| Timing of exercising option | On or before the due date specified u/s 139(1) for furnishing the returns | On or before the due date specified u/s 139(1) for furnishing the returns |

| Basic Tax Rate | 22% | 15% |

| Surcharge Rate | 10% | 10% |

| Cess | 4% | 4% |

| Effective Rate | 25.17% | 17.16% |

| Whether MAT applicable u/s 115JB | Not Applicable | Not Applicable |

| Conditions for Applicability | No Condition | Company has been registered on or after the 01/10/2019, and has commenced manufacturing on or before 31/03/2023 |

| No Condition | The company is not engaged in any business other than the business of manufacture or production of any article or thing | |

| Restrictive Conditions | ||

| No deduction u/s | Section 10AA | Section 10AA |

| No deduction u/s | Section 32(1)(iia) Additional Depreciation |

Section 32(1)(iia) Additional Depreciation |

| No deduction u/s | Section 32AD

Section 33AB Section 33ABA or Section 35(1)(ii),(iia) & (iii) Section 35(2AA), (2AB) Section 35AD Section 35CCC Section 35CCD |

Section 32AD

Section 33AB Section 33ABA or Section 35(1)(ii),(iia) & (iii) Section 35(2AA), (2AB) Section 35AD Section 35CCC Section 35CCD |

| No set off of loss | If such loss is attributable to any of the deductions referred to above | If such loss is attributable to any of the deductions referred to above |

| Special Conditions | No Condition | AO can verify whether the transaction with close connection parties, resulted in more than the ordinary profits.

These transactions to be considered as Specified Domestic Transactions subject to Arm’s Length Price |

Analysis of Savings in Tax Rates, if option u/s 115BAA if exercised

| Income Slabs | Pre–Amendment Scenario | Tax Rate as per New option given u/s 115BAA |

Savings in Tax Rates | ||

| Companies having turnover Below Rs 400 cr | Companies having turnover of Rs 400 cr or more | Companies having turnover Below Rs 400 cr | Companies

having turnover of Rs 400 cr or more |

||

| total income upto Rs 1 Crore | 26.00% | 31.20% | 25.17% | 0.83% | 6.03% |

| total income exceeding Rs 1 Crore but not exceeding Rs 10 crore | 27.82% | 33.38% | 25.17% | 2.65% | 8.21% |

| total income exceeding Rs 10 crore | 29.12% | 34.94% | 25.17% | 3.95% | 9.77% |

|

Above rates are including of Applicable Surcharge and Cess’s |

|||||

Disclaimer: – This document is intended for private circulation & knowledge sharing purpose only. All efforts have been made to ensure the accuracy of information in this document, however we will not be responsible for any errors that may have crept in inadvertently and do not accept any liability whatsoever, for any direct or consequential loss howsoever arising from any use of this document. The document shall not be construed as professional advice or an opinion

Author Bio

Whether Surcharge is applicable on income below 1Cr? Whether rate of 25.17% is uniform for category of domestic companies earning income below 1Cr, between 1Cr and 10Cr, 10Cr and above?