Legislative intent:

PM Modi’s words during Mann Ki Baat programme before launching of Benami Law:

“Even now, some people think they can bring their black money, the money earned through corruption or the one which is unaccounted for, back into the system through illegal means. Unfortunately, they are misusing the poor for this purpose by misleading, luring or tempting them by putting money into their accounts.”

“These people are trying to find ways to again bring their ill-gotten wealth, black money, benami and unaccounted cash back in to the system. They are scouting for illegal ways to save their black money and unfortunately even in this pursuit they are looking to misuse the poor.”

Why the erstwhile law has been revamped and why the same has not been discarded?

Appointed date is 1st November, 2016.

Applies to earlier Benami transactions if not declared in IDS.

Erstwhile law – containing only 9 sections (most of which were merely non-charging ones) – was only a ‘skeleton’ and was not being acted upon at all.

Article 20 of Constitution of India: Protection in respect of conviction for offences:

No person shall be convicted of any offence except for violation of the law in force at the time of the commission of the act charged as an offence, nor be subjected to a penalty greater than that which might have been inflicted under the law in force at the time of the commission of the offence

Some definitions:

Property:

Assets of any kind, whether movable or immovable, tangible or intangible, corporeal or incorporeal and includes any right or interest or legal documents or instruments evidencing title to or interest in the property and where the property is capable of conversion into some other form, then the property in the converted form and also includes the proceeds from the property.

Benami Transaction:

(A) a transaction or an arrangement—

(a) where a property is transferred to, or is held by, a person, and the consideration for such property has been provided, or paid by, another person; and

(b) the property is held for the immediate or future benefit, direct or indirect, of the person who has provided the consideration,

Except when the property is held by—

(i) where the person in whose name the property is held is a coparcener in a Hindu undivided family and the property is held for the benefit of the coparceners in the family; or

(ii) where the person in whose name the property is held is a trustee or other person standing in a fiduciary capacity, and

(iii) The property is held for the benefit of another person for whom he is a trustee or towards whom he stands in such capacity.

(B) a transaction or an arrangement in respect of a property carried out or made in a fictitious name; or

(C) a transaction or an arrangement in respect of a property where the owner of the property is not aware of, or, denies knowledge of, such ownership;

(D) a transaction or an arrangement in respect of a property where the person providing the consideration is not traceable or is fictitious;

Explanation.—For the removal of doubts, it is hereby declared that benami transaction shall not include any transaction involving the allowing of possession of any property to be taken or retained in part performance of a contract referred to in section 53A of the Transfer of Property Act, 1882, if, under any law for the time being in force,

(i) consideration for such property has been provided by the person to whom possession of property has been allowed but the person who has granted possession thereof continues to hold ownership of such property;

(ii) stamp duty on such transaction or arrangement has been paid; and

(iii) the contract has been registered.

Benami Property:

Any property which is the subject matter of a benami transaction and also includes the proceeds from such property.

Benamidar:

A person or a fictitious person, as the case may be, in whose name the benami property is transferred or held and includes a person who lends his name.

Authorities:

The following shall be the authorities for the purposes of this Act, namely

(a) the Initiating Officer – DCIT

(b) the Approving Authority – Addl. CIT

(c) the Administrator – TRO

(d) the Adjudicating Authority – PMLA Officer

The authorities shall, for the purposes of this Act, have the same powers as are vested in a civil court under the Code of Civil Procedure, 1908, while trying a suit in respect of the following matters, namely:-

(a) discovery and inspection;

(b) enforcing the attendance of any person, including any official of a banking company or a public financial institution or any other intermediary or reporting entity, and examining him on oath;

(c) compelling the production of books of account and other documents;

(d) issuing commissions;

(e) receiving evidence on affidavits; and

(f) any other matter which may be prescribed.

The following officers shall assist the authorities in the enforcement of this Act, namely:-

(a) income-tax authorities appointed under sub-section (1) of section 117 of the Income- tax Act, 1961;

(b) officers of the Customs and Central Excise Departments;

(c) officers appointed under sub-section (1) of section 5 of the Narcotic Drugs and Psychotropic Substances Act, 1985;

(d) officers of the stock exchange recognised under section 4 of the Securities Contracts (Regulation) Act, 1956;

(e) such other officers of the Central Government, State Government, local authorities or banking companies as the Central Government may, by notification, specify, in this behalf.

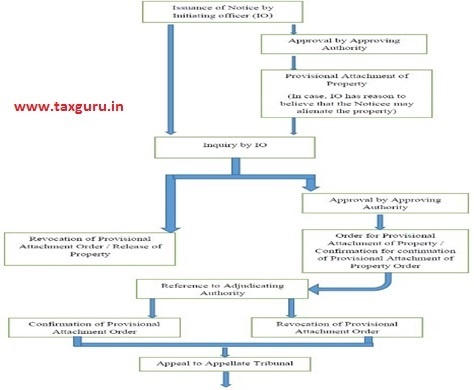

Attachment, Adjudication and Confiscation:

Any property, which is subject matter of benami transaction, shall be liable to be confiscated by the Central Government.

No person, being a benamidar, shall re-transfer the benami property held by him to the beneficial owner or any other person acting on his behalf.

Where any property is re-transferred in contravention of the provisions of sub-section (1), the transaction of such property shall be deemed to be null and void. Whereas the following is the hierarchical structure for Confiscating the benami properties:

Appellate Tribunal:

The Appellate Tribunal shall consist of a Chairperson and at least two other Members of which one shall be a Judicial Member and other shall be an Administrative Member.

The Appellate Tribunal shall not be bound by the procedure laid down by the Code of Civil Procedure, 1908, but shall be guided by the principles of natural justice and, subject to the other provisions of this Act, the Appellate Tribunal shall have powers to regulate its own procedure.

Since no designated Appellate Tribunal has been formulated under the Benami Law, the appellate cases under this law shall be adjudicated by the PMLA Tribunal at present.

Offences and Prosecution:

Where any person enters into a benami transaction in order to defeat the provisions of any law or to avoid payment of statutory dues or to avoid payment to creditors, the beneficial owner, benamidar and any other person who abets or induces any person to enter into the benami transaction, shall be guilty of the offence of benami transaction. Whoever is found guilty of the offence of benami transaction referred to in sub-section (1) shall be punishable as under:

| OFFENCE | FINE | IMPRISONMENT |

| For guilty of offence of a benami transaction | Up to 25% of the FMV | Minimum 1 upto 7 years |

| For providing false information | Up to 100% of the FMV | Minimum 6 upto 5 years |

Closure:

This new Benami Transactions (Prohibition) Act 2016 offers a wider scope. With its wider scope the new act will be a great help to deal with this social fallacy i.e. Benami properties. Due to the narrow and ambiguous scope of the earlier Act many such cases regarding Benami properties could not be solved. But now with the wider and specific scope of the said such cases can be easily proved in the court of law.

The popular perception of “Benami property” has now undergone to sea change and it will include all transactions and arrangements beyond the transactions in respect of immovable property.

There is a saying of Justice Holmes “Taxes are what we pay for civilized society. I like to pay taxes, with them I buy civilization.”