Basis of Charge of Income Tax under the Income-tax Act, 1961: An Analytical Study of Sections 4, 5 and 14

Introduction:

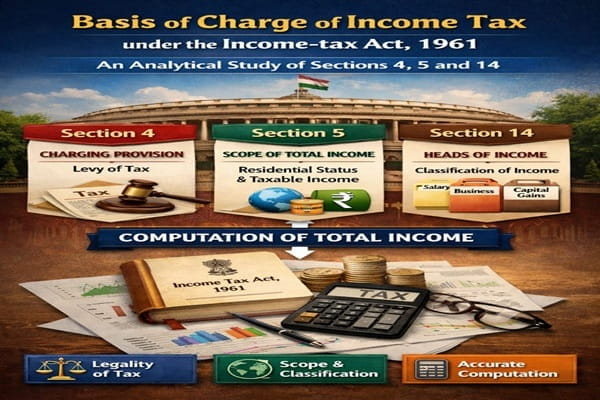

In India, the Income-tax Act of 1961 provides the statutory authority for the imposition of income tax. Sections 4, 5, and 14, together provides the legislative framework for imposing the income tax, identifying the extent of taxable income, and categorizing income into various heads for computational purpose, all these provisions provide the basis of this Act’s tax system. Section 4 provides the charging provision, Section 5 defines the scope of total income, and Section 14 lays down the heads of income.

Although taxation is a fundamental component of sovereignty, its implementation is subjected to constitutional and statutory limitations. In India, the authority to levy income tax flows from the Income-tax Act. The Act creates a systematic framework for taxation of revenue received by businesses, individuals, and other entities.

The basis of charge under this Act is not given under one section but it is the result of the combined operation of Sections 4, 5 and 14. All these provisions must be read together to understand:

- When tax liability arises,

- Which income falls under the taxable ambit and

- How income is categorized and computed.

Section 4: The Charging Provision

A. Nature and Function

Section 4 is the charging section of the Act. It provides that income tax shall be charged for every assessment year at the rates prescribed by the relevant Finance Act in respect of the total income of the previous year of every person.

The charging provision is given in Section 4 of the act. This section provides that income tax of every assessment year will be charged at the rates which are prescribed in the relevant Finance Act. It is charged in respect of total income of the previous year of every person.

The essential components of Section 4 are:

- Tax is imposed for an assessment year,

- The charge applies to every “person” as defined under the Act,

- The tax is levied on “total income” and

- The applicable rates are prescribed annually through the Finance Act.

Section 4 does not independently define income or lay down the rules for the computation purpose. Instead, it operates after total income has been determined in accordance with other provisions of the Act. Thus, it serves as the statutory authority for imposition, but not as a computational mechanism.

B. Concept of Assessment Year and Previous Year

In this Act two terms in relation to year are used. One is “previous year” the year in which income is earned and second is “assessment year” the year in which tax is to be assessed. This distinction ensures administrative clarity and systematic collection of revenue.

Section 5: Scope of Total Income

While Section 4 imposes the charge, Section 5 defines the scope of total income. It determines the extent to which income is taxable in India. It helps in determining tax liability based on a person’s residential status in India during the previous year. According to this section residents are taxed on global income, while Non-Residents (NR) and Not Ordinarily Residents (NOR) are taxed only on income received, or accrued in India.

A. Residential Status and Taxability

Section 5 classifies taxpayers based on their residential status which is determined under Section 6 of the Act. The scope of taxable income varies accordingly:

- A resident is taxable on global income, irrespective of where it is earned or received.

- A non-resident is taxable only on income received or deemed to be received in India, or income accrued or deemed to accrue in India.

- A resident but not ordinarily resident (RNOR) is subject to a limited extension of global taxation.

This differentiation on the basis of residency reflects internationally accepted principles of taxation based on territorial nexus and residence.

B. Receipt and Accrual Principles

Income may be included in total income based on:

- Receipt- Income received in India is taxable.

- Accrual or Arising- Income that becomes due or legally enforceable in India is taxable.

The concept of accrual makes sure that income is taxed when a right to receive arises, not just when it is actually received. This principle connects taxation with economic reality.

C. Deemed Income

The Act also includes certain incomes deemed to accrue or arise in India, even if not directly earned within the territory. This extends the reach of Indian taxation in appropriate circumstances.

Section 14: Heads of Income

This section is the foundational provision in this act as it mandates the classification of income into five heads which are specific and exhaustive. It is done in order to calculate the total taxable income in India. It ensures structured tax reporting, where every, source of income is categorized under one of the following, unless otherwise exempt:

- Salaries

- Income from House Property

- Profits and Gains of Business or Profession

- Capital Gains

- Income from Other Source

A. Purpose of Classification

The main purpose behind the classification of income head is computation of income tax. Rules for determining taxable income are different for all the five heads. It includes provisions for deductions, exemptions, and allowances.

This structure of classification ensures uniformity in computation of tax, helps to prevent overlapping of taxation and ensures Application of appropriate deductions to different types of income.

B. Mandatory Nature of Classification

Every income has to be assessed under the appropriate head only. Once it is decided in which head the income falls then we follow the computation provisions applicable to that head. If the income does not fall under first four heads, then it will automatically fall under the residuary head that is “Income from Other Sources”.

Interrelationship Between Sections 4, 5 and 14

All the three sections are interrelated and interconnected in a very logical way. Section 5 helps to determine whether the income falls within the scope of total income based on residential status and territorial nexus. Section 14 helps in classifying the income under a specific five heads for computation and Section 4 imposes tax on the total income so computed and classified.

This integrated structure ensures that taxation is neither arbitrary nor excessive. If income is not falling under the scope of Section 5 then it will not be taxed. If income is not falling under any of the heads defined in Section 14 then it will not be computed. And if there is no proper computation, the charging provision under Section 4 cannot operate effectively. Thus, these sections form a coherent legislative framework.

Principles Governing the Basis of Charge

The basis of charge in India is not merely governed by The Income Tax Act 1961 but also deep rooted in fundamental legal and constitutional principles. Several fundamental principles govern the charging structure:

- Authority of Law

You are liable to pay the tax only if it is authorized by statute. If no legislative mandate, no tax imposition. This principle traces its roots from Article 265 which mandates that no tax shall be levied or collected except by authority of law. This principle prevents arbitrary imposed taxation.

- Tax on Total Income

As per this act, charge is on total income and not on gross receipts. The legislative intent behind this is that taxation should be based on net income after applying relevant provisions relating to exemptions, deductions, allowances, set-off and carry forward of losses.

- Strict Construction

The charging provisions for tax are subjected to strict interpretation. The scope of taxation cannot be extended beyond the clear language of the statute. If particular income is not falling within the ambit of the statute, such income cannot be taxed. This principle ensures certainty in tax liability and also provide protection to taxpayers from arbitrary expansion of tax base.

- Territorial Nexus and Residential Principle

The tax liability depends on residential status as well as the territorial connection with India. Tax will only be levied if sufficient nexus exists between the income and the territory.

Contemporary Relevance

In modern day economy, certain issues arise relating to cross-border transactions and digital income, determination of income in international contexts, classification of emerging income streams and interaction between domestic law and tax treaties. All these issues are resolved through the interplay of Section 4,5 and 14. These provisions serves as guiding resolution to various contemporary problems related to imposition of tax.

Conclusion

The basis of charge under the Income Tax Act, 1961 is based on well structured framework which is given under Sec 4, 5 and 14. All these provisions do not operate in isolation but collectively determines the tax liability, which income is within taxable ambit and how income is to be computed. Section 4 establishes provision for levying the tax, Section 5 determines the scope of total income by linking it to residential and territorial principles, and Section 14 provides framework for classification of income under various heads.

These provisions operated harmoniously and ensures that the income tax is imposed within statutory limits. This reflects the carefully designed legislative intent that balances principles of fairness and certainty.

A comprehensive understanding of these sections is very essential for various stakeholders such as students, practitioners, and policymakers engaged in the field of direct taxation, as they form the core of the Indian income tax system.

References:

- Income Tax Act 1961.

- Constitution of India.

- Ministry of Finance, Government of India – Finance Acts.

- The Law and Practice of Income Tax by Palkhivala & Kanga – LexisNexis.

- Law of Taxation by Dr. S.R. Myneni.