Case Law Details

Mitsui Prime Advanced Composites India Pvt. Ltd. Vs ITO (ITAT Delhi)

Material Facts

The assessee filed its return of income for Assessment Year 2020-21 declaring nil income. The case was selected for scrutiny and referred to the Transfer Pricing Officer under Section 92CA due to international transactions with its associated enterprise. A draft assessment order proposed a transfer pricing adjustment. After the assessee filed objections, the Dispute Resolution Panel (DRP) issued directions on 28.03.2024. Pursuant to those directions, the Assessing Officer passed the final assessment order dated 30.04.2024 under Sections 143(3), 144C(13) and 144B, determining the assessed income at ₹4,44,72,947.

Procedural History

The assessee appealed before the ITAT and raised an additional legal ground contending that the final assessment order, though dated 30.04.2024, was digitally signed and uploaded with the digital signature on 01.05.2024, making it barred by limitation under Section 144C(13). The Tribunal admitted the additional ground as it involved a pure question of law.

Legal Issue

Whether the final assessment order was barred by limitation where it was dated 30.04.2024 but digitally signed on 01.05.2024.

Relevant Statutory Provisions

- Section 143(3)

- Section 144B

- Section 144C(13)

- Section 92CA

- Section 270A

Assessee’s Submissions

The assessee submitted that the DRP directions were issued on 28.03.2024 and the final assessment order had to be passed on or before 30.04.2024. Although the order bore the date 30.04.2024, both the order and the ITBA portal records showed that it was digitally signed on 01.05.2024. The assessee relied upon judicial precedents holding that an order or notice becomes complete only upon digital signing.

Revenue’s Submissions

The Revenue contended that the assessment order had been passed and communicated on 30.04.2024 in accordance with the draft order. It argued that digital signatures are system-appended and the Assessing Officer had completed all necessary actions on 30.04.2024, placing reliance on the ITBA order-sheet details.

Tribunal’s Findings and Reasoning

The Tribunal examined the sequence of events reflected on the ITBA portal and the copy of the assessment order. It found that the assessment order had been digitally signed on 01.05.2024. Following the Delhi High Court decision in Suman Jeet Agarwal v. ITO and the other authorities relied upon by the assessee, the Tribunal held that the assessment order became complete only upon digital signing. Since the digital signature was affixed on 01.05.2024, the order was completed beyond the limitation period ending on 30.04.2024 and was therefore barred by limitation.

Final Ruling

The Tribunal quashed the assessment order as time-barred. As the assessment itself was quashed, the remaining grounds relating to the transfer pricing adjustment and other issues were held to be infructuous and were not adjudicated. The assessee’s appeal was allowed.

Cases Discussed

- CIT v. Hyundai Rotem Company (Delhi High Court), [2025]180 com 18 (Delhi HC)

- Suman Jeet Agarwal v. ITO (Delhi High Court), [2022] 143 taxmann.com 11 (Delhi)(HC)

- Bennett Coleman & Co. Ltd. vs. National Faceless Assessment Centre, Delhi (ITAT Mumbai), ITA No. 1387/Mum/2023

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal by the assessee is against the final assessment order dated 30.04.2024 passed by the Assessment Unit, Income Tax Department, (hereinafter referred to as the ‘ld. AO’) under Section 143(3) r.w.s. 144C(13) read with Section 144B of the Income-tax Act, 1961 (“the Act”), pursuant to the directions of the Hon’ble Dispute Resolution Panel-1, New Delhi (DRP) order dated 28.03.2024 for the Assessment Year 2020-21.

2. Grounds of appeal filed by the assessee are reproduced as under:

“ General Grounds

1 . The assessment order passed by the Ld. AO in pursuance to the directions issued by the Hon’ble Dispute Resolution Panel (“DRP”) is a vitiated order as the Hon’ble DRP erred both on facts and in law in confirming additions made by the Ld. AO/Ld. Transfer Pricing Officer (“TPO”) to the Appellant’s income by issuing an order without appreciation of facts and law.

2. That the Ld. AO erred in assessing the income of the Appellant at INR 4,44,72,947 as against the returned income declared by the Appellant at INR NIL by making an addition of INR 4,44,72,947-, being the transfer pricing adjustment, by holding that Mitsui India’s international transactions do not satisfy the arm’s length principle envisaged under the Act.

B. TRANSFER PRICING GROUNDS:

3 That the Ld. AO/TPO erred on the facts and in law in enhancing the income of the Appellant by INR 4,44,72,947 by holding that the Appellant’s international transaction does not satisfy the arm’s length principle envisaged under the Act and in doing so, have grossly erred in:

3.1. Not allowing Capacity Utilization Adjustment while computing arm’s length price.

3.2. While applying Transactional Net Margin Method (“TNMM”), exclusion and inclusion of some appropriate comparable companies in the final set of comparables despite of their comparability and non-comparability with respect to the functions performed, assets employed, risks assumed, and products manufactured in comparison with the assessee.

3.3. That on the facts and circumstances of the case, the Ld. TPO has erred in considering Bank Charges as non-operating expenses and therefore, erred in not appropriately computing the operating margin of the Assessee as well as of the comparable companies.

C. OTHER GROUNDS:

4. Ld. AO/TPO has erred both the fact and in law in initiating penalty proceedings under section 270A of the Act.

The above grounds of appeal are mutually exclusive and without prejudice to each other.

The appellant craves to be allowed to add, delete or amend any other grounds of appeal either before or at the time of hearing as we may be advised.

The assessee prays accordingly.”

2.1 Subsequently, the assessee raised an additional ground as under:-

“4.4 That on the facts and circumstances of the case and in law, the final assessment order dated April 30, 2024 passed by the Assessing Officer (“Ld. AO), digitally signed and uploaded on ITBA portal dated 01 May 2024, pursuant to the directions dated March 28, 2024, is barred by limitation and thus, bad in law, as it has been passed beyond the time frame prescribed under section 144C (13) of the Income Tax Act, 1961 (“Act”).”

3. At the outset, Ld. AR has submitted that the additional ground raised by the assessee, is a purely legal ground and prayed that the same be admitted.

3.1 We have heard the rival submissions and perused the material available on record. We note that the addition ground raises a legal issue regarding limitation and hence in view of settled legal position in this regard, the same is being admitted for adjudication.

3.2 Brief facts are that the assessee filed its return for A.Y. 2020-21 on 29.01.2021 declaring Nil income. The case was selected or scrutiny and a reference to the TPO was made u/s 92CA of the Act, as the assessee had entered into international transactions with its AE. Ld. AO proposed an addition of Rs. 46846928/- vide draft assessment order.

3.3 Aggrieved, based on the TPO’s order, the assessee filed objections before the Dispute Resolution Panel (DRP). Pursuant to the DRP’s directions dated 28.03.2024, the AO passed final assessment order dated 30.04.2024 at assessed income of Rs. 4,44,72,947/-. Further aggrieved, the assessee is in appeal before the Tribunal.

4. Before us, Ld. AR submitted that the assessee wishes to first press the additional ground which is purely legal in nature and has made submissions as well filed a paper book. It has been argued by ld. AR that the direction of DRP were issued and uploaded on 28.03.2024 and, therefore, the final assessment order had to be passed on or before 30.04.2024. From the copy of the final assessment order, it is obvious that though the order was dated 30.04.2024, the same was digitally signed on 01.05.2024. This fact is also evident from the order-sheet details available on the portal wherefrom it is seen that though the order was uploaded on 30.04.2024, the same was digitally signed on 01.05.2024 and hence was time barred.

4.2 In support of his arguments, ld. AR has placed reliance on several judicial pronouncements, some of which are as under:

(i) Suman Jeet Agarwal v. ITO [2022] 143 taxmann.com 11 (Delhi)(HC),

wherein the Hon’ble Delhi High Court has held that the date of issue of notice is not important, it is the date of signing notice, which is important. Hence, where notice was dated 31-3-2021 but had been digitally signed on 1-4-2021, date of notice will be 1-4-2021.

(ii) CIT v. Hyundai Rotem Company [2025]180 com 18 (Delhi HC), it was held that an order passed by the FAO on 1/7/2022 when the period of limitation from the end of the month in which DRP directions were issued ended on 30/06/2022, the same was clearly barred by limitation.

(iii) Bennett Coleman & Co. Ltd. vs. National Faceless Assessment Centre, Delhi ITA No. 1387/Mum/2023, wherein under similar facts and circumstances, it was held by the Mumbai bench of ITAT, that the assessment proceedings conclude only after the order is digitally signed. Since the order dated 28/09/2021 was not digitally signed, it was an incomplete order which was completed on 1/10/2021 and hence barred by limitation.

5. Ld. DR, on the other hand, has vehemently argued, that as per the order-sheet details available on ITBA portal it is seen that the final order has been passed in accordance with the draft order on 30/04/2024 and, therefore, the order had been communicated to the assessee on 30/04/2024 itself which is within the limitation date. He further explained that the digital signatures are different from physical signatures and the AO does not put these digital signatures which are appended by the system. The action at the end of the AO had been duly completed on 30/04/2024 and hence it cannot be said that the order had been passed beyond limitation.

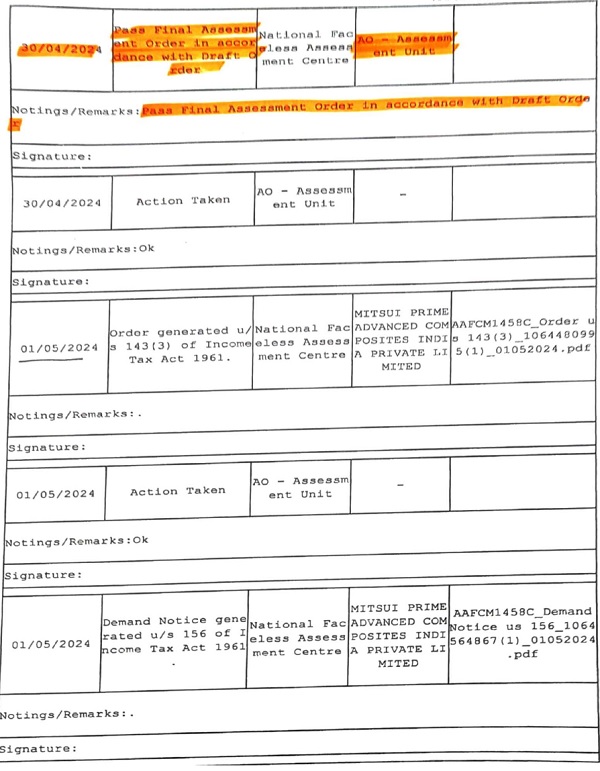

6. We have heard the rival submissions and perused the material available on record. We note that the relevant sequence of events as evident from the ITBA portal was as under:

6.1 From above sequence of events as well as from the copy of assessment order placed before us, it is evident that the assessment order had been digitally signed on 1/5/2024. In view of the decision of the Hon’ble jurisdictional High Court in the case of SumanJeet Agarwal vs. ITO (supra), other cases relied upon by the assessee and discussed hereinbefore, we are of the considered view that the order was complete only after the digital signatures on 1/5/2024 and hence the same was barred by limitation. Accordingly, the assessment order passed after the limitation date on 30.04.2024 is hereby quashed. Since the order itself has been quashed, remaining grounds are rendered infructous and hence need not be adjudicated upon.

7. In the result, appeal of the assessee is allowed.

Order pronounced in the open court on 30.06.2026.

Author Bio