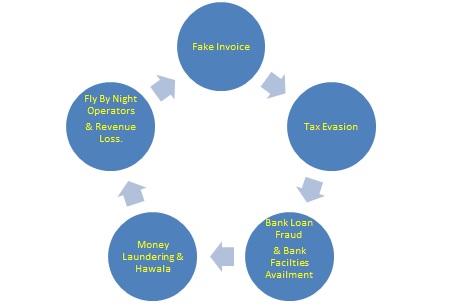

It’s almost 34 months since GST has been introduced in India and one of the major Shortfalls of the GST is creation of fake invoices to wrongly avail fake credit out of thin air thereby creating revenue loss to the Government which is not acceptable, to make you understand this concept let me explain the same with a practical example.

Mr X will open a Company/Firm and along with it open a number of Fake companies / Shell Firms/ Organizations with his accomplices for a monthly fee or commission on a regular basis until he is caught by the investigations authorities. He will book Fake invoices without any physical delivery of the goods from the intended party in his books of account and after a while passes an accounts payable entry in the book saying that the payment has been made to the quantity and value of fake goods received by their firm , but if you closely observe the accounting entry which he passes in the books, the bank transaction, in this case the RTGS transaction, the name of the account payable party will be different in the accounting books and in the bank statement, the actual beneficiary is the one appearing in the bank statement /passbook and not the person as mentioned in the accounting records, so you will come to know about this transaction only on deeper scrutiny and not on the face of it which you obviously rely upon. Now once the money reaches the above said firm, he will use the help of Couriers or Angadias to convert the bank money to cash for a commission of 4-5 % per transaction amount, that is his income but just imagine the ITC sitting on their account which will be utilized for claiming ITC, moving forward which can be in the range of 13-18%, so it’s a big game for people with an intention to commit a crime/fraud, now a question may come in to mind as to how these people have got GSTIN , it’s because of the simple registration formalities, the master mind in such a scenario would have exploited the ease of doing business conveniently in the existing system by getting a GST registration easily and quickly and later take advantage of the liberalized norm for grant of registration in GST in addition to use of fabricated electricity bills, fake rent agreements were also uploaded on the GST portal to obtain registration. Even bank account details declared in the GST registration were either found non existing or in other person’s names, the intention of all these master minds is to usurp ITC on commission basis as mentioned above.

Potential motives for using fake invoices:

An Expansive list of motives that drive unscrupulous entities to generate of use of fake invoices is as follows:

♦ Evasion of GST on taxable output supplies

- Availing undue ITC

- Saving GST (cash) by payment of tax liability using undue ITC

- Clandestine supply without invoices and without payment of taxes

♦ Converting excess ITC into cash

- Transferring of ITC to those who can utilize it

- Shifting ITC from exempted supplies to taxable supplies\

- Encashment of ITC by way of IGST refund or unutilized ITC refunds

♦ Inflating turnover for the purpose of

- Availing higher Credit Limit/ Overdraft from Banks

- Obtaining bank loans

- Improving valuations for IPO or sale of stake

- Obtaining contracts including Government contracts

♦ Booking fake purchases for getting Income-tax benefits by:

- Showing reduced profit margins and higher expenses

- Avoiding payment of Income-tax by reducing net profit

♦ Cash generation/ diversion of company funds

♦ Laundering of money

Conclusion

It has been proposed that businesses, whose owners or promoters do not have commensurate financial track record, like filing of income tax returns and payment of income tax to the government, may require detailed physical and financial verification by tax officers, before their companies can be considered for GST registration.

The Finance Ministry is in the process of plugging these gaps in the GST registration process to ensure that only genuine businesses get a GST registration and those, who have intent to defraud the system, are purged out at the registration stage itself.

Kindly clarify this sir, I understand that the GST website itself does not allow a dealer to claim ITC beyond the actual or 120% of ITC as per 2A. For any ITC to appear in 2A, it must have been credited by the supplier. The supplier has to first pay the GST to get credit in his portal after which he will be able to pass on the credit to the dealer. In that case, the supplier must pay the GST to enable the following persons to claim ITC. How frauds are happening.

Also the GST authorities at least in the case of refunds, they could verify to the eway billing and rules could be amended to verify to the income tax returns with some minimum limits.

While granting a GST registration the local industry association, and locality neighbors can be contacted.