Form GST PMT-09 is a facility provided under the GST law that enables a registered taxpayer to transfer or adjust balances available in the electronic cash ledger between different major heads and minor heads. The article explains the applicability and practical use of Form GST PMT-09, particularly for transferring cash balances within the same GSTIN or between GSTINs having the same PAN. However, transfer of cash balance to a GSTIN with a different PAN is not permitted. The cash ledger is structured into four major heads—IGST, CGST, SGST, and Cess—and five minor heads—Tax, Interest, Fees, Penalty, and Others. The article clarifies that cash balance can generally be transferred from one major head to another major head and from one minor head to another minor head without restriction. Various scenarios are discussed explaining transfers from IGST, CGST, SGST, and Cess to other major and minor heads, demonstrating that the GST portal permits most such adjustments through PMT-09. However, a key restriction is that transfer is not permitted when both the major head and minor head are the same, as this would amount to transferring funds from the same head to itself. The article also highlights that balances available in the electronic credit ledger (ITC) cannot be transferred through PMT-09. The legal basis for such transfers is provided under Rule 87(13) of the CGST Rules, which allows taxpayers to transfer any amount of tax, interest, penalty, fee, or other amount within the electronic cash ledger using Form GST PMT-09. Practical portal screenshots further illustrate that the system disables entries where transfer is not allowed, while allowing transfers between permissible heads. Overall, PMT-09 serves as an important compliance tool enabling taxpayers to efficiently reallocate cash balances and correct payment classifications within the GST system.

1. Coverage of this article:

a. In this article, I am discussing the applicability of Form GST PMT-09 under GST Act.

b. Whether we can transfer the amount of cash ledger in various major or minor heads.

c. Further, are there any restriction on transferring the cash from major to another major head or from one minor head to another minor head?

2. Full form of PMT:

Full form of PMT is “Payment Tax Forms”.

3. What is Form GST PMT 09:

- This form is used for transferring of cash balance within same GSTIN or different GSTIN having same PAN.

- In this article, I am covering only transferring of cash balance within same GSTIN having same PAN.

4. Types of transfer:

| S No | Particulars | Allowed or not |

| 1 | Transfer of cash within same GSTIN | Yes |

| 2 | Transfer of cash in different GSTIN having same PAN | Yes |

| 3 | Transfer of cash in different GSTIN having different PAN | No |

- A person can transfer the cash balance in their own GSTIN having same PAN.

- It is not permissible to transfer the cash balance in the other GSTIN having different PAN.

- Example: A Ltd cannot transfer the cash balance in the GSTIN of B Ltd. It is because they both are having different PAN.

5. Types of Major & Minor heads:

| S No | Major heads | Minor heads |

| 1 | IGST | Tax |

| 2 | CGST | Interest |

| 3 | SGST | Fees |

| 4 | Cess | Penalty |

| 5 | Others |

There are total 4 major head & 5 minor heads in this form for the purpose of transferring of cash balance.

6. Transfer of cash balance between major heads:

| S No | Transfer from | Transfer to | Permissible |

| 1 | IGST | IGST | Yes |

| 2 | IGST | CGST | Yes |

| 3 | IGST | SGST | Yes |

| 4 | IGST | Cess | Yes |

| 5 | CGST | IGST | Yes |

| 6 | CGST | CGST | Yes |

| 7 | CGST | SGST | Yes |

| 8 | CGST | Cess | Yes |

| 9 | SGST | IGST | Yes |

| 10 | SGST | CGST | Yes |

| 11 | SGST | SGST | Yes |

| 12 | SGST | Cess | Yes |

| 13 | Cess | IGST | Yes |

| 14 | Cess | CGST | Yes |

| 15 | Cess | SGST | Yes |

| 16 | Cess | Cess | Yes |

I am clarifying that to my article readers that you can transfer the cash balance from major head to another major head. There are no such restrictions between major heads.

7. Transfer of cash balance between minor heads:

| S No | Transfer from | Transfer to | Permissible |

| 1 | Tax | Tax | Yes |

| 2 | Tax | Interest | Yes |

| 3 | Tax | Fees | Yes |

| 4 | Tax | Penalty | Yes |

| 5 | Tax | Others | Yes |

| 6 | Interest | Tax | Yes |

| 7 | Interest | Interest | Yes |

| 8 | Interest | Fees | Yes |

| 9 | Interest | Penalty | Yes |

| 10 | Interest | Others | Yes |

| 11 | Fees | Tax | Yes |

| 12 | Fees | Interest | Yes |

| 13 | Fees | Fees | Yes |

| 14 | Fees | Penalty | Yes |

| 15 | Fees | Others | Yes |

| 16 | Penalty | Tax | Yes |

| 17 | Penalty | Interest | Yes |

| 18 | Penalty | Fees | Yes |

| 19 | Penalty | Penalty | Yes |

| 20 | Penalty | Others | Yes |

| 21 | Others | Tax | Yes |

| 22 | Others | Interest | Yes |

| 23 | Others | Fees | Yes |

| 24 | Others | Penalty | Yes |

| 25 | Others | Others | Yes |

I am clarifying that to my article readers that you can transfer the cash balance from minor head to another minor head. There are no such restrictions between minor heads.

8. Credit ledger balance:

The balance of input in electronic credit ledger cannot be transferred within the same or different GSTIN.

9. 1st scenario IGST to various major and minor head:

- I have covered the scenarios in 6th & 7th point which is related to the transfer of cash balance into major and minor heads.

- Now, I am covering the scenario that combines both heads which will be helpful for the readers at the time filing of this form.

| S No | Transfer from major head | Transfer from minor head | Transfer to major head | Transfer to minor head |

| 1 | IGST | Tax | IGST | Allowed between all minor heads except tax |

| 2 | IGST | Interest | IGST | Allowed between all minor heads except interest |

| 3 | IGST | Fees | IGST | Allowed between all minor heads except fees |

| 4 | IGST | Penalty | IGST | Allowed between all minor heads except penalty |

| 5 | IGST | Others | IGST | Allowed between all minor heads except others |

| 6 | IGST | Tax | CGST | Allowed between all minor heads |

| 7 | IGST | Interest | CGST | Allowed between all minor heads |

| 8 | IGST | Fees | CGST | Allowed between all minor heads |

| 9 | IGST | Penalty | CGST | Allowed between all minor heads |

| 10 | IGST | Others | CGST | Allowed between all minor heads |

| 11 | IGST | Tax | SGST | Allowed between all minor heads |

| 12 | IGST | Interest | SGST | Allowed between all minor heads |

| 13 | IGST | Fees | SGST | Allowed between all minor heads |

| 14 | IGST | Penalty | SGST | Allowed between all minor heads |

| 15 | IGST | Others | SGST | Allowed between all minor heads |

| 16 | IGST | Tax | Cess | Allowed between all minor heads |

| 17 | IGST | Interest | Cess | Allowed between all minor heads |

| 18 | IGST | Fees | Cess | Allowed between all minor heads |

| 19 | IGST | Penalty | Cess | Allowed between all minor heads |

| 20 | IGST | Others | Cess | Allowed between all minor heads |

In this scenario, I have explained that IGST balances can be transfer into various major and minor heads except some cases.

10. 2nd scenario CGST to various major and minor head:

In this scenario, I have explained that CGST balances can be transfer into various major and minor heads except some cases.

| S No | Transfer from major head | Transfer from minor head | Transfer to major head | Transfer to minor head |

| 1 | CGST | Tax | CGST | Allowed between all minor heads except tax |

| 2 | CGST | Interest | CGST | Allowed between all minor heads except interest |

| 3 | CGST | Fees | CGST | Allowed between all minor heads except fees |

| 4 | CGST | Penalty | CGST | Allowed between all minor heads except penalty |

| 5 | CGST | Others | CGST | Allowed between all minor heads except others |

| 6 | CGST | Tax | SGST | Allowed between all minor heads |

| 7 | CGST | Interest | SGST | Allowed between all minor heads |

| 8 | CGST | Fees | SGST | Allowed between all minor heads |

| 9 | CGST | Penalty | SGST | Allowed between all minor heads |

| 10 | CGST | Others | SGST | Allowed between all minor heads |

| 11 | CGST | Tax | IGST | Allowed between all minor heads |

| 12 | CGST | Interest | IGST | Allowed between all minor heads |

| 13 | CGST | Fees | IGST | Allowed between all minor heads |

| 14 | CGST | Penalty | IGST | Allowed between all minor heads |

| 15 | CGST | Others | IGST | Allowed between all minor heads |

| 16 | CGST | Tax | Cess | Allowed between all minor heads |

| 17 | CGST | Interest | Cess | Allowed between all minor heads |

| 18 | CGST | Fees | Cess | Allowed between all minor heads |

| 19 | CGST | Penalty | Cess | Allowed between all minor heads |

| 20 | CGST | Others | Cess | Allowed between all minor heads |

11. 3rd scenario SGST to various major and minor head:

In this scenario, I have explained that SGST balances can be transfer into various major and minor heads except some cases.

| S No | Transfer from major head | Transfer from minor head | Transfer to major head | Transfer to minor head |

| 1 | SGST | Tax | SGST | Allowed between all minor heads except tax |

| 2 | SGST | Interest | SGST | Allowed between all minor heads except interest |

| 3 | SGST | Fees | SGST | Allowed between all minor heads except fees |

| 4 | SGST | Penalty | SGST | Allowed between all minor heads except penalty |

| 5 | SGST | Others | SGST | Allowed between all minor heads except others |

| 6 | SGST | Tax | CGST | Allowed between all minor heads |

| 7 | SGST | Interest | CGST | Allowed between all minor heads |

| 8 | SGST | Fees | CGST | Allowed between all minor heads |

| 9 | SGST | Penalty | CGST | Allowed between all minor heads |

| 10 | SGST | Others | CGST | Allowed between all minor heads |

| 11 | SGST | Tax | IGST | Allowed between all minor heads |

| 12 | SGST | Interest | IGST | Allowed between all minor heads |

| 13 | SGST | Fees | IGST | Allowed between all minor heads |

| 14 | SGST | Penalty | IGST | Allowed between all minor heads |

| 15 | SGST | Others | IGST | Allowed between all minor heads |

| 16 | SGST | Tax | Cess | Allowed between all minor heads |

| 17 | SGST | Interest | Cess | Allowed between all minor heads |

| 18 | SGST | Fees | Cess | Allowed between all minor heads |

| 19 | SGST | Penalty | Cess | Allowed between all minor heads |

| 20 | SGST | Others | Cess | Allowed between all minor heads |

12. 4th scenario Cess to various major and minor head:

In this scenario, I have explained that Cess balances can be transfer into various major and minor heads except some cases.

| S No | Transfer from major head | Transfer from minor head | Transfer to major head | Transfer to minor head |

| 1 | Cess | Tax | Cess | Allowed between all minor heads except tax |

| 2 | Cess | Interest | Cess | Allowed between all minor heads except interest |

| 3 | Cess | Fees | Cess | Allowed between all minor heads except fees |

| 4 | Cess | Penalty | Cess | Allowed between all minor heads except penalty |

| 5 | Cess | Others | Cess | Allowed between all minor heads except others |

| 6 | Cess | Tax | SGST | Allowed between all minor heads |

| 7 | Cess | Interest | SGST | Allowed between all minor heads |

| 8 | Cess | Fees | SGST | Allowed between all minor heads |

| 9 | Cess | Penalty | SGST | Allowed between all minor heads |

| 10 | Cess | Others | SGST | Allowed between all minor heads |

| 11 | Cess | Tax | IGST | Allowed between all minor heads |

| 12 | Cess | Interest | IGST | Allowed between all minor heads |

| 13 | Cess | Fees | IGST | Allowed between all minor heads |

| 14 | Cess | Penalty | IGST | Allowed between all minor heads |

| 15 | Cess | Others | IGST | Allowed between all minor heads |

| 16 | Cess | Tax | CGST | Allowed between all minor heads |

| 17 | Cess | Interest | CGST | Allowed between all minor heads |

| 18 | Cess | Fees | CGST | Allowed between all minor heads |

| 19 | Cess | Penalty | CGST | Allowed between all minor heads |

| 20 | Cess | Others | CGST | Allowed between all minor heads |

13. Summary chart:

| S No | Transfer between Major Heads | Transfer between Minor Heads |

| 1 | IGST to IGST | Allowed between all Minor Heads except for the same Minor Head |

| 2 | IGST to CGST | Allowed between all Minor Heads |

| 3 | IGST to SGST | Allowed between all Minor Heads |

| 4 | IGST to Cess | Allowed between all Minor Heads |

| 5 | CGST to CGST | Allowed between all Minor Heads except for the same Minor Head |

| 6 | CGST to IGST | Allowed between all Minor Heads |

| 7 | CGST to SGST | Allowed between all Minor Heads |

| 8 | CGST to Cess | Allowed between all Minor Heads |

| 9 | SGST to SGST | Allowed between all Minor Heads except for the same Minor Heads |

| 10 | SGST to IGST | Allowed between all Minor Heads |

| 11 | SGST to CGST | Allowed between all Minor Heads |

| 12 | SGST to Cess | Allowed between all Minor Heads |

| 13 | Cess to Cess | Allowed between all Minor Heads except for the same Minor Heads |

| 14 | Cess to IGST | Allowed between all Minor Heads |

| 15 | Cess to CGST | Allowed between all Minor Heads |

| 16 | Cess to SGST | Allowed between all Minor Heads |

It is a summary table in which I have covered all the situations.

14. Note:

- If both major and minor head are same then transfer is not permissible.

- Suppose, Mr. Ram wants to transfer interest balance of CGST into interest head of CGST. It is not permitted because both major and minor head are same & you are transferring the balance from same head to same head that why it is not permissible in 9th to 12th point (i.e. 1st to 4th scenarios).

- Transfer of cash into different GSTIN under same PAN will be covered in a separate article.

15. Bare Act of Rule: 87(13):

(13) A registered person may, on the common portal, transfer any amount of tax, interest, penalty, fee or any other amount available in the electronic cash ledger under the Act to the electronic cash ledger for integrated tax, central tax, State tax or Union territory tax or cess in FORM GST PMT-09.

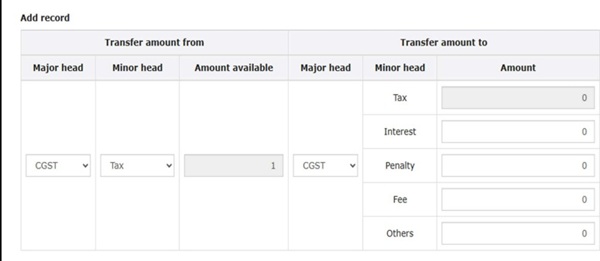

16. 1st Screenshot of the portal:

In this scenario, I want to transfer Rs 1 from CGST tax head to tax head of same major head but this is not permissible & portal disable the tax column as well. We cannot enter any amount in tax column.

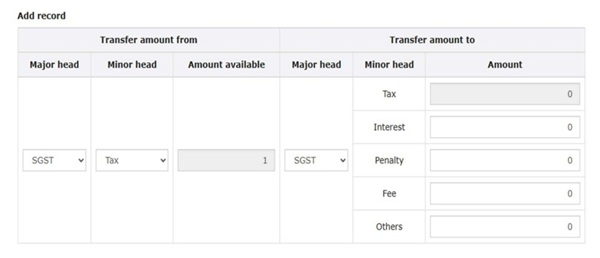

17. 2nd Screenshot of the portal:

In this scenario, I want to transfer Rs 1 from SGST tax head to tax head of same major head but this is not permissible & portal disable the tax column as well. We cannot enter any amount in tax column.

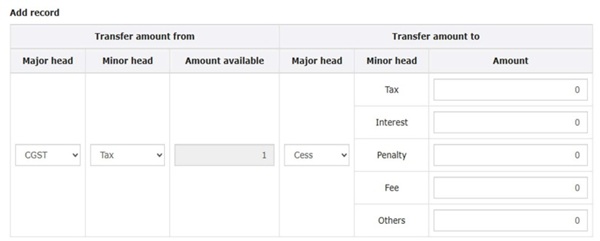

18. 3rd Screenshot of the portal:

- In this scenario, I want to transfer Rs 1 from CGST tax head to various minor head of cess major head & this is permissible & portal allows this.

- We can enter the amount in any column of minor head.

- No column is disable in this case because we can transfer the money in any minor head as per Rule 87(13).

*****

If you have any queries, you can reach the author by email at caashishsingla878@gmail.com.

Disclaimer: The views and opinions expressed in this article are those of the author. This article is intended for general information purposes only and does not constitute professional advice. Readers are strongly advised to consult a qualified professional for guidance specific to their individual situation before making any financial, legal, or tax-related decisions. The author shall not be held liable for any loss or damage of any kind incurred as a result of the use of this information or for any actions taken based on the content of this article.